The importance of financial literacy cannot be overstated in today’s ever-changing financial landscape. Financial literacy is more than a buzzword; it’s the foundation for creating a life of freedom and choice—untangled from the worries of debt and uncertainty. Yet, according to a recent Zippia study, 77% of Americans are financially anxious while 73% of teens want a more personal finance education. As parents and caregivers, we have the opportunity and responsibility to instill healthy financial habits in the next generation from an early age.

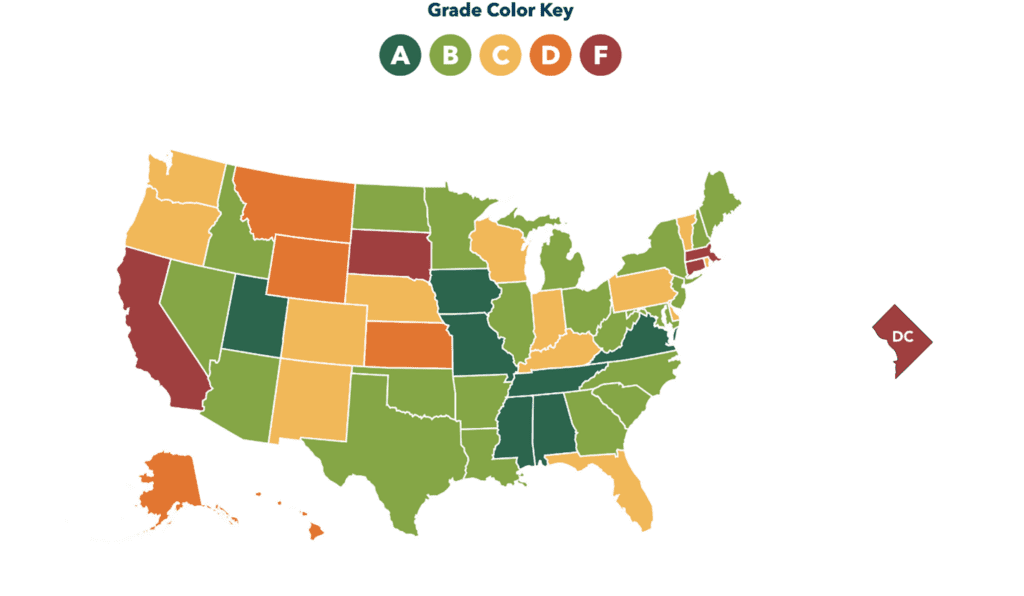

As of 2023, the United States ranked 14th in financial literacy globally, a position that is concerning given its status as the world’s wealthiest country. Meanwhile, Denmark leads as the global frontrunner in financial literacy, with approximately 71% of its adult population recognized as financially literate. Overall, financial literacy among U.S. high school students varies significantly by state, with many still lacking rigorous financial education standards according to Champlain College’s 2023 National Report Card on State Efforts to Improve Financial Literacy in High Schools. Based on findings from the Program for International Student Assessment (PISA), one in five American teenagers have insufficient basic financial literacy skills.

Source: Champlain College

In this article, we’ll explore the significance of financial literacy, the critical role of early education in shaping financial attitudes, and practical strategies for teaching kids about money effectively.

Understanding Financial Literacy

Financial literacy is like a map that guides you through the vast landscape of personal finance management. Think of it as a fusion of knowledge and financial skills that spans across:

- banking

- budgeting

- saving

- investing

Each component is a stepping stone towards financial stability and freedom.

The pursuit of financial literacy is not just about managing money but crafting a financial life that supports your dreams and aspirations.

Understanding the Importance of Financial Literacy

Why is financial literacy important? Consider the burden of student loan debt, the shackles of living paycheck to paycheck—an all-too-common reality for many.

Financial literacy shines as a beacon of hope, offering the tools to break free from the cycle of debt by living within one’s means and making informed decisions. Financial literacy skills, as promoted by the National Financial Educators Council, are a set that, once acquired, provides a lifetime of financial security and peace of mind.

Why Financial Literacy Matters

The ripple effects of financial literacy extend far beyond individual success. When individuals flourish financially, they uplift their families, invigorate their communities, and fortify the nation’s economic backbone. The stark reality of how debt can consume half of one’s income underscores the urgency for financial education—a transformative force that fosters prudent budgeters and savvy savers, capable of withstanding life’s financial storms.

Building a Strong Foundation: The Basics of Personal Finance

Personal finance is the bedrock upon which financial dreams are built. It encompasses the decisions that shape our daily lives—how we earn, spend, save, and invest. Mastering these basics is the cornerstone of a strategy that leads to owning a home, enjoying a comfortable retirement, and achieving the financial goals that matter most to you. Personal financial management plays a crucial role in this process, ensuring that you stay on track towards your objectives.

Introducing Financial Basics to Children

Educating children about basic financial concepts plants the seeds for a prosperous future. I believe deeply in the importance of financial education at all stages, which is why I actively collaborate with local high schools. By working with business departments and teachers, we teach juniors and seniors about financial literacy, covering essential topics such as cash flow, budgeting, and investments. These sessions explore various investment accounts and vehicles, such as stocks, bonds, and mutual funds, and emphasize practical skills like budgeting and responsible credit use. This commitment to fostering financial acumen from an early age aligns perfectly with the nuanced advice provided by professional advisors, ensuring that individuals are prepared for financial decision-making throughout their careers.

By starting early, children can learn the value of money, the importance of saving, and the basics of budgeting. Simple practices like having a piggy bank, setting savings goals for desired toys or games, and involving them in family budgeting discussions can ignite an interest in personal finance. As they grow, more complex concepts such as the role of banks, having a bank account or savings account, the concept of interest, and wise spending can be introduced. This early financial education is pivotal in developing financially savvy adults who are well-equipped to navigate the complexities of the financial world.

Crafting Your Financial Roadmap for the Future

A financial plan is your compass in a sea of economic uncertainty. It’s about more than just numbers on a spreadsheet; it’s a blueprint for realizing your and your children’s life’s ambitions. A robust financial plan can help you with:

- Understanding taxes

- Managing student loans

- Saving for education

- Saving for home ownership

- Planning for retirement

A financial plan is a critical ally in the quest for education, home ownership, and retirement, and acts as a blueprint for achieving these goals through effective budgeting and resource allocation. It emphasizes the importance of creating a budget to track and manage income and expenses, ensuring that every financial decision aligns with one’s long-term objectives. By incorporating budgeting into a financial plan, individuals can prioritize their spending, reduce unnecessary expenses, and set aside funds for future investments, savings, and debt repayment, thereby laying a strong foundation for financial health and stability.

Credit Mastery: Understanding Credit Cards and Scores

Credit is a double-edged sword; wielded wisely, it can carve a path to financial opportunities. Understanding credit and debit cards and how they impact your credit score is paramount. It can mean the difference between favorable loan terms or being hindered by high-interest rates.

Decoding Your Credit Score

Your credit score is a numerical reflection of your financial integrity, encapsulating your creditworthiness based on your historical and current financial behaviors. It’s a score that credit rating agencies meticulously calculate and update, taking into account factors such as your credit history, loan repayment track record, credit card utilization, and the diversity of your credit accounts. Additionally, your credit report provides detailed information about each of these factors, including specific data on your outstanding debts, the length of your credit history, the types of credit accounts you hold, and records of your payments, including any defaults or late payments. This score is a critical indicator to lenders about your future reliability as a borrower.

Credit rating agencies, such as Equifax, Experian, and TransUnion, use complex algorithms to adjust your score as new financial information becomes available. They monitor your financial activities, including the timeliness of your bill payments, the length of your credit history, and the types of credit you manage. For instance, consistently making payments on time positively influences your score, while late payments, defaults, or bankruptcy filings can significantly lower it.

By understanding the dynamics of credit scores and the meticulous approach credit rating agencies employ to adjust these scores, you can take proactive steps to maintain or improve your good credit standing. This entails keeping your credit utilization low—experts often recommend using less than 30% of your available credit—and ensuring a solid payment history. Such prudent financial practices are indispensable for preserving your financial health and securing favorable terms for future credit needs.

Saving Smarter: Emergency Funds and Beyond

Building an emergency fund is like constructing a financial dam—it holds back the floodwaters of unexpected expenses that could otherwise sweep away your stability. Beyond emergency funds, wise saving practices lay the groundwork for wealth accumulation that supports a life of financial ease.

Starting Your Emergency Fund

The journey to financial resilience begins with the first dollar saved for an emergency. It’s about setting attainable goals and nurturing a habit of preparation. Financial experts commonly advise maintaining sufficient funds in your emergency savings to cover living expenses for a period of three to six months. This can provide a cushion for unforeseen events such as medical emergencies, job loss, or urgent home repairs.

Despite this recommendation, statistics reveal a concerning trend: a significant portion of the population is unprepared for financial disruptions. According to a report by Bankrate, nearly 25% of Americans have no emergency savings at all, and only a mere 40% have enough to cover three months of expenses. This highlights the critical need for a mindset shift towards saving and the importance of incremental contributions to build a robust emergency fund.

Through automated savings plans that transfer funds directly from checking to savings accounts, and by gradually increasing contributions as financial circumstances improve, individuals can fortify their financial position. The emergency fund then becomes a bastion of security in an unpredictable world, offering peace of mind and the strength to withstand financial adversities.

Investing in Your Future: Retirement Planning and More

Retirement planning may seem a distant concern, but it’s a journey that begins with a single step today. By investing wisely and harnessing the power of compound interest, you set the stage for a retirement filled with freedom and choice rather than one constrained by financial necessity.

Understanding Retirement Savings Plans

Retirement savings plans are a commitment to your future financial well-being. With a variety of options like 401(k)s, IRAs, and Roth IRAs, you’re empowered to choose the investment vehicle that best aligns with your retirement vision. These plans serve as a cornerstone for long-term wealth accumulation, leveraging the power of compound interest. This financial phenomenon works tirelessly behind the scenes, transforming your regular contributions into a more significant sum over the decades. By initiating your savings journey early, you take full advantage of this effect, allowing your money to grow exponentially. As each year passes, the interest on your savings earns interest of its own, and this cycle repeats, potentially turning even the most modest of savings into a sizeable retirement fund. It’s this principle that underscores the importance of consistency and time in building a substantial retirement nest egg, ensuring that when the time comes to step back from the workforce, you have a reliable financial cushion to support you.

Recognizing Signs of Financial Stress

Financial stress can be a silent predator, lurking in the shadows of our lives, often going unnoticed until it pounces with overwhelming force. Early recognition of signs such as unmanageable credit card debt, constant worry about making ends meet, and a lack of emergency savings, is crucial for taking preemptive action. The consequences of financial stress are not only personal but can spill over into one’s professional life. Studies have shown that employees preoccupied with financial concerns are less productive and more prone to errors at work. For instance, a report by PwC’s 2023 Employee Financial Wellness Survey indicates that 56% of employees distracted by finances spend three hours or more at work each week thinking about or dealing with issues related to their personal finances.

By acknowledging these red flags and seeking wise counsel, you can chart a course back to financial serenity. Starting financial education early can be a game-changer. The Council for Economic Education (CEE) has found that students who receive a financial education are more likely to save, less likely to max out their credit cards, and more likely to pay off their credit card balance in full each month. This early foundation sets the stage for a lifetime of sound financial practices, effectively sidestepping the pitfalls that lead to financial stress. With the right knowledge and tools, you can navigate your financial journey with confidence and poise, ensuring that your focus at work remains sharp and your professional performance unhampered by monetary distractions.

Summary

As our journey through the landscape of financial literacy concludes, remember that the principles and strategies discussed here are not just for the financially savvy—they are for anyone aspiring to a life of financial stability and freedom. With a strong foundation in personal finance, a mastery of credit, disciplined saving, and strategic investing, you are well-equipped to face the financial challenges of today and tomorrow. Let this knowledge be your guiding light, illuminating the path to financial success.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.