The economic shutdown during the pandemic and subsequent stimulus by the Federal Government caused many supply shocks and other disruptions to economic activity. As a result, for several years there were conflicting signals regarding the health of the U.S. economy. Some economic data releases indicated the economy was beginning to expand while other data pointed to economic contraction. Even when it was clear economic growth was slowing, there were different opinions as to whether the weakness was being caused by a lack of demand or disruptions in the supply of goods. This distinction is important because if the weakness was being caused by a lack of demand, then the logical conclusion is that a recession is just around the corner. But if the weakness was the result of disruptions in the supply of goods, then once these disruptions subside the economy could begin to grow again.

Recently the disruptions in the supply chain have been resolved, as the Federal Reserve Bank of New York’s Global Supply Chain Pressure Index has settled back to its long-run trend. As a result, there is a clearer understanding of the actual demand in various sectors of the economy. Smoother supply chains also reduced the cost of goods and alleviated inflation pressures.

Global Supply Chain Pressure Index

Source: Federal Reserve Bank of New York

Meanwhile, demand in many sectors appears to be holding up. Bank lending growth fell last year, but it is still about 2 percent above its longer-term trend after a boom in 2022. Consumer confidence is trending higher, with consumers particularly confident in their present situation. Spending on durable goods has begun to strengthen again, although consumer spending on services is beginning to flatten. Spending on goods provides a stronger boost to the economy than spending on services does.

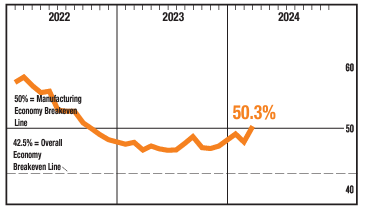

Inflation is not down to the U.S. Federal Reserve’s target of 2 percent, but it’s close (core inflation is running around 3 percent). Stronger spending on goods and lower cost inflation has relieved pressure on U.S. manufacturing. This week’s Institute of Supply Management’s purchasing managers’ index (PMI) of manufacturing registered 50.3 in March, confirming that manufacturing returned to modest expansion in March, after 16 months in contraction (anything above 50 is in expansionary territory).

Manufacturing PMI Index

Source: The Institute for Supply Management

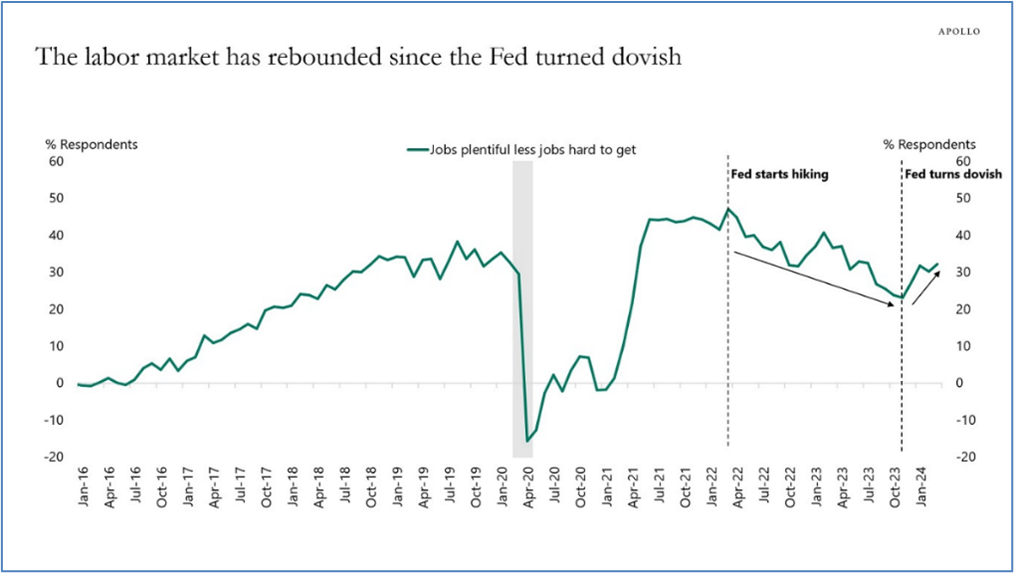

The outlook for jobs is also improving again. After the Fed started raising rates in March 2022, the labor market started weakening, with households saying that it was harder to find a job. This changed after the U.S. Fed announced it was done raising rates. Since then, the labor market has improved, with more households saying that it is easier to find a job. Combined with low jobless claims, the employment picture is back to where it was prior to 2020.

Source: Conference Board, Haver Analytics, Apollo Global

The U.S. economy now appears to be experiencing steady, if unspectacular, growth. Momentum in the economy could last the rest of this year, but that doesn’t mean the battle has been won and there will not be a recession. The Fed has been successful in cooling the economy without causing a recession so far, but many risks remain. If demand accelerates too quickly, a second wave of inflation could be the result.

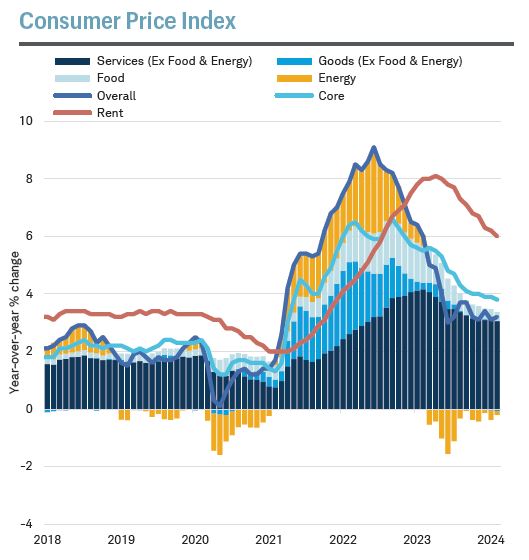

This risk was reinforced with the release of the recent Consumer Price Index (CPI) report in early April, which showed that CPI accelerated at a faster-than-expected pace in March. Headline inflation is stuck at 3 percent, and it appears that getting inflation to the Fed’s target of 2 percent will be difficult. The report likely crushed chances that the Federal Reserve will cut interest rates anytime soon.

Inflation related to both shelter costs and services are not receding as expected. Spending on services has been responsible for the bulk of inflationary pressures, and that continued in the recent CPI report. Core services inflation rose more than expected. Services inflation measures include medical care services, home and auto insurance, and transportation costs. The rebound in spending on goods may be an additional source of inflationary pressures, making the Fed’s effort to reduce inflation even more difficult.

Source: Charles Schwab, U.S. Bureau of Labor Statistics. Table 7. Consumer Price Index for All Urban Consumers (CPI-U)

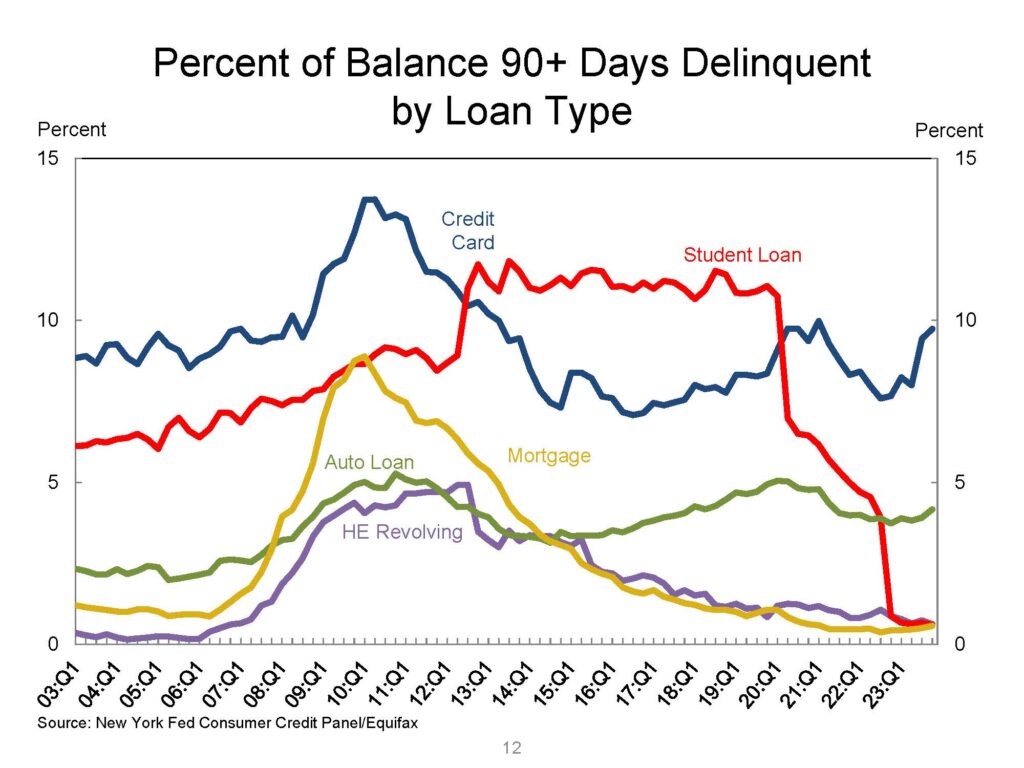

To get inflation down to 2 percent, the Fed may need to maintain elevated rates for most of this year. Higher interest rates are already hurting some sectors of the economy, especially housing. Mortgage demand has dropped sharply because people are hesitant to give up their low fixed rate mortgage on their current home. Credit card and auto loan delinquencies are also rising as debt becomes more expensive. Total debt balances are rising, and consumers’ excess savings are nearly gone.

There are also reasons for concern in the corporate world. Commercial and industrial lending is below long-term trends, bankruptcies are rising, and delinquency rates in commercial real estate are rising. Real business sales and industrial production have both peaked and are falling.

All these trends need to be watched carefully, especially with interest rates probably remaining higher for longer than previously expected. There has historically been a lag of between 10 and 18 months from when the Fed is done raising rates until the negative impacts to growth are fully felt. The Fed was done tightening in July 2023. So, while it appears that the economy is on relatively firm ground and the economic story for 2024 looks to be growth, 2025 may be a different story.

The strength in the economy spurred optimism that corporate earnings will continue to grow, driving most major stock markets around the world higher in the first three months of this year. The MSCI All Country World Index was up 8.2 percent for the first quarter. Large capitalization stocks in the United States once again performed even better than stocks in most other developed countries, as the S&P 500 Index returned 10.6 percent. With economic growth stabilizing and inflation down well off its peaks, investors bet that the U.S. Federal Reserve successfully engineered a soft landing. The Fed was widely expected to cut rates at least three times in the second half of the year, which could keep the soft-landing narrative intact.

However, that storyline is now being questioned as the second quarter begins. Many of the economic data points have been stronger than expected, and inflation remains stuck above 3 percent. This makes it more likely the Fed will maintain rates at elevated levels for the better part of this year to prevent inflation from rising again. During the first quarter, investors downplayed this possibility and instead focused on strengthening economic growth to support higher stock valuations. But the longer inflation remains above 3 percent the less likely it is the Fed will cut rates, and higher rates will likely be a drag on stock market prices.

As a result, investors are once again focusing on the future trajectory of Fed policy, as they were last year. Back then, however, inflation was falling quickly, so investors were counting on six quarter point cuts in 2024 to keep the economy growing and stocks rising. Now that inflation looks more stubborn and only three rate cuts at most are expected, investors are worried about the harm higher rates may do to economic growth in 2025.

Corporate leaders seem to agree that corporate profitability will fall, but not until the fourth quarter of 2024 or the first quarter of 2025. Earnings expectations for the next two quarters of 2024 have been rising, reflecting the stronger than expected growth in the economy. So, while the economy appears to be on firm footing for most of 2024, it is still unclear how much the rate hikes will slow growth in the longer term. A recession in 2025 remains a possibility.

It is impossible to determine how stocks will react in the short-run, even if a recession occurs in 2025. Investors may anticipate a slowdown in 2025 and sell stocks later this year in advance of a slowing economy. There are precedents for this scenario, as stocks historically peak and begin to fall about six months prior to the start of a recession. On the other hand, investors could remain optimistic that a recession will be avoided, and stocks could continue to climb.

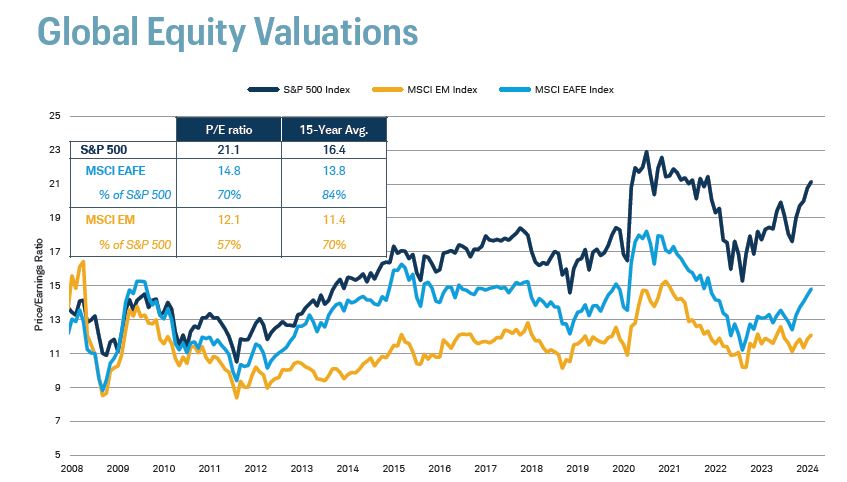

Even if stock markets do fall, a drop in prices will probably be brief and shallow. While valuations have become steep again for the S&P 500 Index as a whole, there are still stocks in many sectors and countries that are more reasonably valued.

Source: Bloomberg, the Schwab Center for Financial Research as of 3/31/2024. Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. Investing involves risk, including loss of principal. Past performance is no guarantee of future results.

The bond markets began the year by pricing in the strong possibility that the Fed would lower their policy rate by over 100 basis points in 2024 due to the expectation of continued progress of inflation measures trending toward its 2 percent target. However, with inflation remaining stubbornly above 3 percent the Fed continues to indicate it will lower rates this year but may keep rates high for longer if inflation doesn’t resume trending lower.

In response to stronger than expected data, U.S. Treasury yields increased between 30-40 basis points in the intermediate to long maturity tenors in the first quarter, which caused fixed income returns to be slightly negative. Interest rates appear to be attractive at their current levels as nominal yields remain above current and future expected inflation rates. Core bond strategies offer compelling income return and may have price appreciation opportunities when inflation eventually recedes or if economic activity stalls.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that the future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.