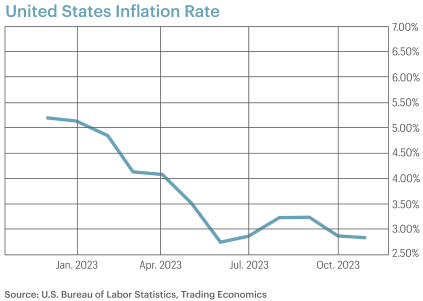

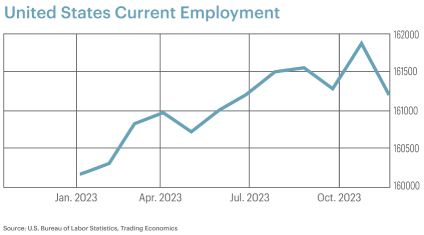

As 2023 ended, the U.S. economy’s performance was even more robust than what was projected by the most optimistic economists. Amazingly, the economy remained resilient, even after the U.S. Federal Reserve (Fed) hiked rates 525 basis points between March 2022 and July 2023. Historically, when the Fed raised interest rates to cool inflation, economic growth has slowed; as growth slows, companies produce less and reduce payroll causing the unemployment rate to rise. But while inflation has cooled to 3.1 percent after peaking at 9.1 percent in June of 2022, the unemployment rate remains low, at 3.7 percent.

Fifty-one years after those of us in Pittsburgh celebrated Franco Harris and the Pittsburgh Steelers’ “Immaculate Reception,” some economists have taken to calling the current environment in the U.S. economy “Immaculate Disinflation.” A decline in inflation of this magnitude while employment growth remains strong does appear miraculous.

Buoyed by lower inflation and a strong jobs market, the U.S. economy grew 4.9 percent in the third quarter, and growth expectations in the fourth quarter were revised higher to 2.5 percent. By year-end, it appeared that the economy was headed toward the elusive “soft landing,” a narrative reinforced at the final meeting of the U.S. Federal Open Market Committee (FOMC) meeting in December of last year. Federal Reserve Chairman Jerome Powell praised the progress made in fighting inflation and indicated the Fed is likely finished tightening monetary policy, setting the table for multiple rate cuts in 2024. The Fed’s estimates of future inflation and interest rates supported the expectation that the Committee will keep its policy rate unchanged in the near term, then cut it three times later in 2024.

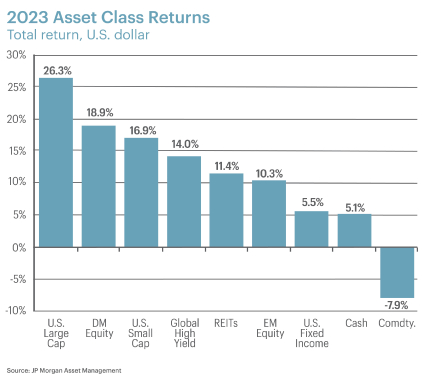

Investors responded predictably to the news that the current interest rate cycle has peaked while the economy remains healthy. They bought everything in sight, resulting in positive total returns for nearly every major asset class:

Why was the economy able to withstand the fastest rate hike of this magnitude in the past 40 years? When the Fed began tightening, pandemic stimulus was still flowing into the economy and consumers had plenty of savings. Also, many businesses and individuals were locked into long-term loans, so the rise in rates did not impact their ability to pay their debts each month yet. As a result, the demand for goods and services remained robust despite the rate hikes. Consumers also were shifting their spending from goods to services, which had the effect of lowering inflation while keeping GDP growth strong.

At the same time, corporations were able to reduce hiring without terminating many positions thanks to the high number of job openings. Toward the end of the year the good news on inflation continued, driven by falling energy costs and improvement in the supply chains that had been disrupted during the pandemic.

It seems unlikely that all those conditions will persist in 2024. Since 1945, inflation has never fallen in the U.S. as far as it has during this cycle without a recession occurring sometime in the following 18 months. Though the current economic data still shows growth is solid and inflation is tame, many forward-looking indicators signal that the good news is nearing an end.

Higher rates are finally beginning to hurt both businesses and consumers. Capital spending by businesses is showing signs of slowing. Defaults are rising on office mortgages, and delinquency rates are beginning to rise across a wide range of consumer debt, including credit cards. Many younger consumers are faced with higher debt payments, including the resumption of student loan payments. In addition, consumers are seeing their cash positions dry up. The worrying combination of higher debt payments and lower cash positions is causing consumer confidence to wane. Given the strength of the economy, the Fed might hold rates at high levels for a while yet, so it is unlikely this concern will disappear any time soon.

These issues have not dramatically cut into growth yet, but they are beginning to be felt. There is a lag between when a rate hike is enacted and when the rate hike fully impacts the economy. That lag can be anywhere from 12 to 18 months, so the largest hit to growth is not likely to come until mid-2024. This explains the observation that the current economy appears on course for a soft-landing instead of at the beginning of a recession. While many of the lagging or coincident economic indicators continue to show strength, the leading economic indicators signal that a recession was not avoided but pushed into 2024.

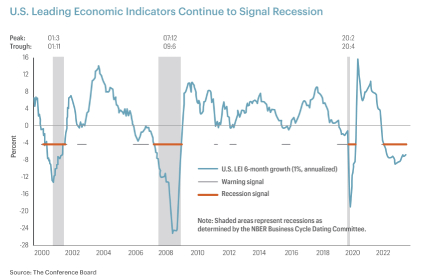

Lagging economic indicators tend to show what the economic environment was in the past. Examples are the unemployment rate, corporate profits, and labor cost. Coincident economic indicators tend to reveal the current economic environment; wages, hours worked, and gross domestic product (GDP) are examples. Leading economic indicators are data that tend to anticipate future economic activity; the yield curve, housing starts, and manufacturing activity are examples.

In the U.S., both the lagging and coincident indicators are signaling the economy continues to grow. However, the Conference Board’s Leading Economic Indicators remain negative; they have fallen for 20 straight months. The Conference Board’s statement in December said a recession “is likely in 2024 due to high interest rates, tighter lending standards and a slowdown in consumer spending.”

However, the Conference Board also noted that because of the underlying strength in some pockets of the economy, the recession is likely to be short and shallow before a recovery begins the second half of 2024.

Stock Markets

Stocks in the U.S. were predominantly higher in 2023, with most major stock market indices more than erasing their losses from the prior year. After a brief fall of almost 10 percent in September and October, the market surged into year-end, bringing the S&P 500 Index within half a percent of its record close in January 2022. The prevailing sentiment that inflation will fall to a level where the Fed will not only stop raising rates but aggressively cut rates in the first half of 2024 drove the rally the last couple months of the year. For stocks to continue rising in 2024, corporate earnings must continue to rise, and the Fed needs to follow through with their rate cuts. While this is possible, it is not the most likely scenario. There are two more likely paths the economy could take this year, and neither are favorable for stock prices in the short term.

Inflation could remain stubbornly above the Fed’s targeted rate of 2 percent, which would prompt the Fed to maintain interest rates at the current level longer than is currently expected. That would probably cause growth to slow later in the year and bring about a recession and lower corporate profits. Alternatively, if the signs of an impending recession in the first half of the year are correct, and inflation continues to fall, the Fed could cut rates aggressively. But corporate profits will shrink more than expected during a recession, and it will be difficult to justify higher stock prices with lower corporate profits.

Either way, we get a recession and lower corporate earnings, the unknown being when the recession occurs. Corporate leaders seem to agree that corporate profitability will fall in 2024. According to FactSet, both the number and the percentage of S&P 500 companies issuing negative earnings outlooks for the fourth quarter and 2024 are well above historical averages. For 2024, some are estimating that corporate profits could shrink at least 8 percent.

The uncertain path of the U.S. economy could result in a more volatile stock market in 2024. Stocks typically peak and begin to fall about six months prior to the start of a recession, then begin to recover before it ends. That cycle could begin early this year, or later depending on which path the economy takes. A recession is likely to be short and shallow, which would help limit any downward move in stocks before they recover. At the outset of the recession, both inflation and interest rates will have fallen, which will provide a boost to demand and eventually increase corporate earnings and lift stock prices.

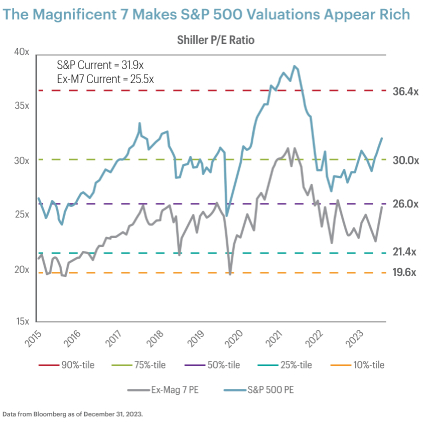

Another factor that will limit the fall in stock prices is that while valuations have become steep again for the S&P 500 Index as a whole, there are still many stocks that are reasonably valued. The Shiller Price to Earnings (PE) Ratio of the S&P 500 Index is at 31.9 times earnings, but the index’s gain was driven by the outsized performance of several mega cap tech names related to Artificial Intelligence (AI), dubbed the “Magnificent Seven.” When these seven stocks are excluded the, Shiller P/E Ratio is a much more reasonable 25.5 times earnings. With many stocks reasonably valued, a correction could be brief and less severe than usual if the recession is shallow.

Bond Markets

Bonds were also higher in 2023, with all the gains coming in the fourth quarter. The Bloomberg Aggregate Bond Index rose 5.5 percent for the full year. Corporate bonds fared even better, with the Bloomberg Corporate Bond Index up 8.5 percent.

After peaking in mid-October, longer maturity Treasury yields moved materially lower in response to lower inflation data. In December bond prices continued to rise after the Fed strongly signaled that it doesn’t anticipate increasing its policy rate any further and is open to lowering rates if inflation continues to trend toward its policy objective. Investors anticipate the Fed will begin decreasing its policy rate as early as March 2024.

Despite the nearly 80 basis point decline in yields during the fourth quarter of 2023, we continue to believe that interest rates are attractive at their current levels. Real yields (adjusting for inflation) remain well above their post global financial crisis average, which indicates that monetary policy is restrictive and could eventually cause economic activity to slow. This would be supportive of further interest rate declines and price appreciation of longer duration bond portfolios. Core fixed income strategies offer an attractive risk/return profile because of the possibilities of a slowdown in economic growth and continued progress on inflation.

Watch the latest webinar Brian Sommers did regarding the latest market trends.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.