Following a decrease in 2023, Medicare rates will resume their climb.

When the Centers for Medicare and Medicaid Services announced the standard monthly premiums and deductibles for Medicare Part B coverage for 2023, it was something of a pleasant surprise. The standard monthly premium for 2023 of $164.90 was about five dollars less than in 2022, and the annual deductible was seven dollars less at $226.

But alas, all good things must come to an end, and most U.S. residents enrolled in Original Medicare or a Medicare Advantage plan will see their premiums and deductibles increase, to a monthly Part B premium of $174.70 and an annual deductible of $240, increases of $9.80 and $14 respectively. The average Part D prescription coverage premium will decline, about a dollar to $55.50 per month.

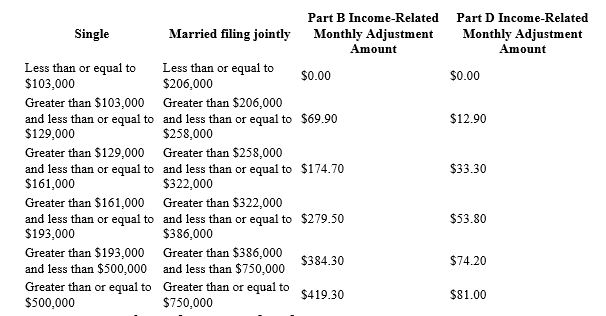

Moreover, people with incomes over a certain amount will pay a surcharge known as “IRMAA,” or Income Related Monthly Adjustment Amount, a provision that has been in place since 2003 and the Medicare Prescription Drug, Improvement, and Modernization Act, Depending on your income your monthly IRMAA could range from $69.90 to $419.30 throughout 2024.

Essentially, IRMAA is a way of increasing the Medicare Part B and now Part D payments drawn from your monthly Social Security checks. The premium for Medicare Part B has represented about 25 percent of Medicare costs, with Social Security picking up the rest. Hence, there is IRMAA.

The key points to know about IRMAA are how it is determined and when it kicks in:

IRMAA for 2024:

Source: Centers for Medicare & Medicaid Services

Additional IRMAA considerations

IRMAA’s intent is to generate funds from wealthier taxpayers, but it can also affect people who have received a lump sum of money from a one-time event, such as the sale of a house. You can appeal the IRMAA surcharge for a “life-changing event,” such as a divorce or the death of a spouse.

Avoiding an IRMAA surcharge includes being careful about how you access your savings in retirement. For example, a couple decided to withdraw cash from their tax-deferred IRA to purchase a new car. They not only had to pay the tax on the withdrawn amount, but the “income” also put them over their IRMAA threshold.

A more proactive way to plan for IRMAA is to examine your retirement savings vehicles. We’ve been programmed to put as much money as possible into a 401(k) or IRA as we move through our working years. That money is committed pre-tax; we don’t have to pay tax on it until we start withdrawing it in our retirement years, the rationale being that our tax bracket will be lower in retirement than during our earning years. However, mixing pre-tax contributions with savings in post-tax dollars, as in a Roth IRA, might be a better plan. Or consider converting your IRA to a Roth before you have to start your required minimum distributions (RMDs). Not only will you have already paid the taxes on those investments, but they will also provide more withdrawal flexibility because they won’t be subject to RMDs as are regular IRAs.

We’re here to help. For more information on IRMAA or with any of your retirement planning questions or concerns, contact me at DNWilliams@hbkswealth.com or schedule an appointment by calling 239-919-1268.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.