Private equity, illiquidity, hedge fund, venture capital: terms that to some translate as risky, to others are incomprehensible, and to others the sound of opportunities worth salivating over. What they all have in common is that they refer to private markets in contrast to the more familiar public markets comprised of the likes of stocks and bonds and ETFs. So what are private markets and why would someone want to own them? What might keep people away from them?

In a private market, investors channel their funds into the equity or debt of an entity that isn’t publicly traded. The private market encompasses private equity, private companies that have partnered with a private equity firm in order to grow the company; venture capital, early-stage, ground-floor type of investments; private real estate investments; private debt; infrastructures; and natural resources.

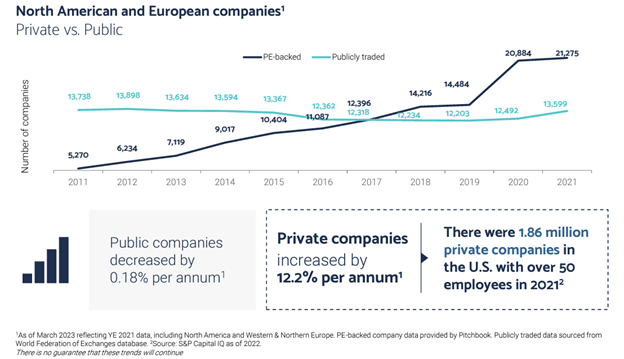

Compared to public investments, private market investments are generally a longer-term strategy due to their complicated liquidity and often even longer terms. As well, information on private companies can be more difficult to obtain compared to publicly traded ones. Still, investing in the private market has surged by 170 percent over the last ten years, as reported by the 2020 McKinsey’s Private Markets Annual Review; public investment choices, in contrast, have decreased by 50 percent over the past two decades.

Benefits of private market investing

Private market investments offer several advantages, including:

Unique opportunities. In stark contract to public companies, private markets offer access to a wide range of opportunities, including investing at various stages of a company’s lifecycle, direct access to management, and better visibility of a company’s portfolio. In most of the private spaces there are also considerably more investment options, be equity investing or debt.

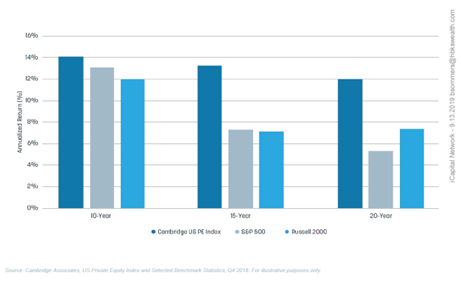

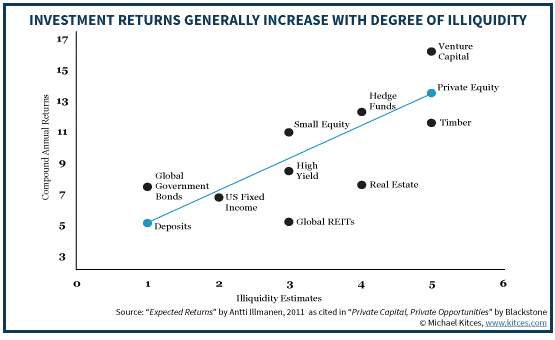

Higher return potential. Private markets often outperform public due to an illiquidity premium, which is the additional return investors receive for investing in less liquid assets. In many cases outperformance has been a function of illiquidity, dedication to time, access to companies in early stages of development, and managers who can use the additional capital to create more value. Once invested, the managers generally can exert an immense amount of control in an effort to maximize returns, whereas in public markets the focus is more often on the short-term share price.

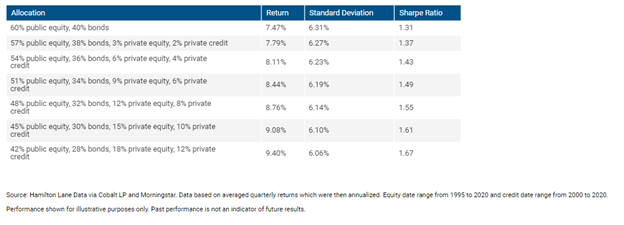

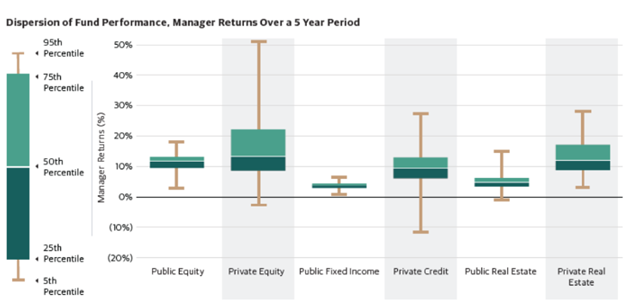

Diversification. Private market investors gain access to innovative and unique opportunities not typically found in public markets. For instance, as evidenced in the chart below, private investors can experience less volatility (standard deviation) and better returns in their portfolios due to the dynamics of buying and selling in the private market especially when combined with liquid public markets. This is a trend all portfolios seek: multiple sources of less correlated return.

Added stability. While private market investments are not at all immune to economic shifts and can and do lose money, they tend to stabilize over time, helping reduce your portfolio’s overall volatility during tough market conditions. They also tend to price on a delayed basis and thus the volatility isnt observed as suddenly.

Long-term Focus. Private market investments are generally one of the longest term investments, which helps insulate investors from short-term economic downturns that can cause extreme reactions in the public markets. It can also allow for opportunities to deploy capital during economic downturns as these types of investments often thrive in the years following a downturn, which is much more likely when a manager isn’t worried about clients pulling cash from their investment base.

Risks of private market investing

Considering these advantages why isn’t everyone invested in private markets? For one, investors and their advisors often have little or no expertise in the space, and even when they do, there are substantial risks to consider:

Illiquidity. Unlike securities in the public market that are easily bought and sold on a daily basis, private market funds, usually structured as limited partnerships, lack daily liquidity. Investors need a long-term perspective, an understanding that these investments can have a lifespan of 10 years or even longer. Additionally, holding multiple long-term investments like these may lead to increased tax burdens, so maintaining a diverse portfolio is important. However, illiquidity has its benefits. People often invest emotionally and thus sell when they should buy and buy when they should sell. The illiquidity feature forces the investors to stay invested. As such, it is a reason private investing can produce superior performance.

Associated costs. Private market investments come with management fees and incentive/performance fees. Management fees typically range from 1 to 2 percent, while incentive/performance fees, often implemented when specific target goals are met, can range from zero to 20 percent. As well, formal partnership structures may mean additional associated costs. How capital is called can also create a short-term drag as the funds may be in cash while waiting for deployment. There is also the possibility of a “J Curve,” where fees drive down the net investment value in the early years of the investment of capital followed by the funds increase in value as the targeted outcomes are achieved.

Speculative nature. Investing in the private market for the long term involves a certain level of speculation, as there is no guarantee that the promised returns will materialize. In a worst-case scenario, there can be a partial or total loss of capital. Of course, there is risk of loss in the public markets, but there are arguably more failures in private equity. Much like the public markets, these risks call for diversification.

Access to quality managers. When venturing into private markets, accessing quality managers can pose a challenge. Minimum investment thresholds mean top managers can have minimums in excess of $1 million per investor, which limits access to all but certain clientele. Additionally, there is a wide disparity between manager performance and the median. An abundance of due diligence is required to ensure you as investor are using appropriate managers and also mechanisms that allow for lower minimums. Even a $10 million portfolio probably should not have $1 million invested with one manager. Ideally you want diversity in managers in your portfolio.

Qualification. Most funds require a qualified purchaser status, such as an investment base in excess of $5 million ($25 million for a corporate entity). In some cases, accredited investor status, an annual income of $200,000 or liquid net worth excluding home of $1 million, allows access to private investments.

Tax reporting. Tax reporting for many funds is done via a K-1, which not uncommonly is produced days before the mid-October deadline for filing an extended return. In short, investors should plan on extending their tax return every year. There are ways around this, such as holding your interest in a retirement account, however the type of investment in the account could trigger Unrelated Business Taxable Income if not placed properly.

Widely varying returns. Where public markets have worked diligently to keep asset class performance in line with a benchmark, private equity markets still have the opportunity for outsized returns relative to their benchmarks. Estimates are that 90 percent of large cap managers underperform the S&P 500 Index. In private equity, far more managers outperform the median, but many drastically underperform the average. Therefore it is increasingly important to conduct due diligence and diversify private strategies.

www.atlaswealthadvisors.com

Private investments—private equity, credit, or real estate—have historically performed well in terms of both returns and risk, some of the benefit, oddly enough, driven by the investments’ inherent disadvantages. Still, private investing is not for everyone. Nor are there established thresholds of income or net worth to determine who should or should not invest. For example, it might not be appropriate for a client with a $10 million portfolio to invest 10 percent in a private investment. On the other hand, a private investment could be ideal for investor with a $1.5 million portfolio and living off a pension and Social Security. It is a decision that should be made in the context of the individual’s financial plan.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.