For much of this year, the U.S. Federal Reserve’s rate hikes have caused economic growth to slow just enough for inflation to fall substantially from its peak while the employment situation remained healthy. The economic data continued to show resilience for most of the third quarter, supporting this scenario and keeping alive the notion that the Fed could soon stop raising rates.

This view was supported recently by Chicago Federal Reserve Bank President Austan Goolsbee. On Bloomberg’s Odd Lots podcast, Goolsbee said he sees nothing to indicate that the U.S. economy is deviating from the “golden path”, which he defined as continuing to move toward the Fed’s 2 percent inflation target while at the same time avoiding a recession. He added, “I still feel like this is our goal and it’s still possible”.

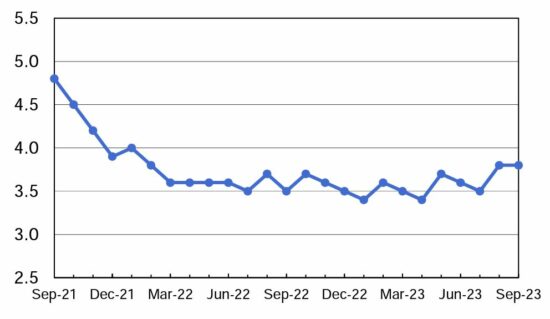

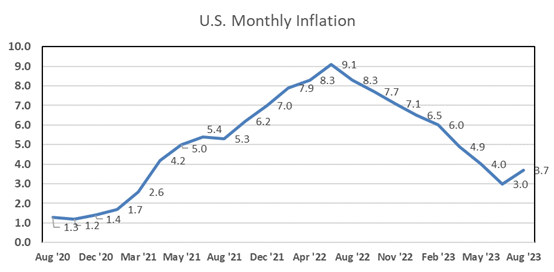

So far the “golden path”, which is often referred to as a soft landing, has been realized. The Fed’s 5.25 percentage points of interest-rate hikes over the last 18 months has brought the monthly 12-month inflation rate down to 3.7 percent in September from a forty-year high of 9.1 percent in June of 2022. At the same time, unemployment has barely budged; it was 3.8% in September, compared with 3.7% a year earlier.

Unemployment Rate Has Remained Flat

Source: The Bureau of Labor Statistics

While Inflation Has Fallen Dramatically

Source: Statista Research Department

The question as we enter the last few months of 2023 is, how much longer will it last? Will the good news continue or is this the last stage before a recession hits? Although recently the economy has been showing signs of breaking down, at times it seems that those who still see a recession on the horizon are looking at the sky in search of stars in broad daylight. They are watching for something that can only be seen under specific conditions, which do not exist at that moment. However, nightfall eventually arrives, and only then it is evident that the stars were there all along.

While the economy has been resilient thus far, the impact of the Federal Reserve’s rate hikes has still not fully been felt due to the lagged effect of monetary policy decisions. When the Federal Reserve acts, it usually takes 18 to 24 months for the action to fully have the desired impact on the economy. With the largest part of the slowing effect still to come it would be a mistake to extrapolate strong economic growth in the third quarter of this year into next year.

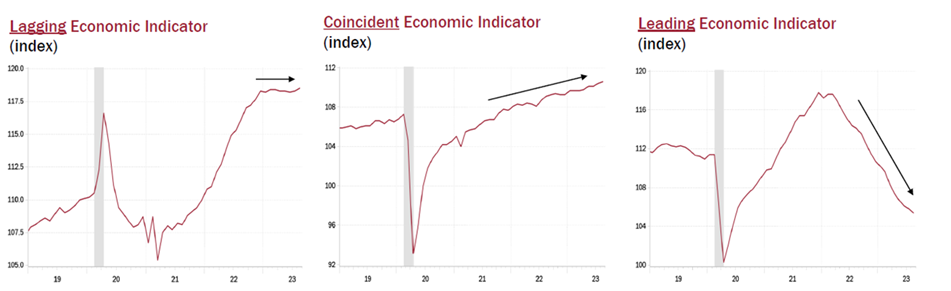

When assessing the expected strength in the economy it is important to focus on forward-looking indicators of economic growth, not backward-looking or concurrent indicators. Sometimes, there is a marked difference in what can be gleaned about the economic cycle depending on the time frame you are looking at. Currently, lagging and coincident indicators are still showing strength in the economy. However, the leading economic indicators, which are forward-looking, have been falling for seventeen straight months. In the past, a recession has followed any period when the leading economic indicator fell for that many consecutive months. It is no surprise that the New York Fed’s modified recession model pegs the odds of a recession in the next twelve months at 96%.

Source: Rosenberg Research

Additional evidence is accumulating which indicates that nighttime is approaching. Consumer spending, which has driven the recovery as the economy exited the pandemic, faces a growing list of headwinds. Gasoline prices have surged higher, interest costs have risen, bank loans are much harder to get as banks tighten lending standards, and many people will face the resumption of student loan payments in October. A long-threatened strike against Detroit automakers by the UAW union erupted in September and shows little progress toward resolution.

Also, many individual households have not been hit with higher monthly payments on their homes yet because they have 30-year fixed mortgages at low rates. However, that also means they are stuck in their current homes and cannot afford to trade up into a new home. They face a choice between staying in their current homes or paying a much larger monthly payment for a new home. The savings cushion many consumers built up through the pandemic has been largely spent, so the impact of these headwinds on spending could be significant.

Corporations will feel the pinch as well. In addition to lower sales to consumers, many corporations will soon face higher debt service on their loans. A lot of companies extended the maturities of their loans at low rates during the pandemic. Soon, they will have to choose between paying higher rates on new loans or delaying capital investments in their business. Either choice will be a drag on economic growth.

With all of these headwinds set to dampen economic growth, it seems likely that a recession will occur in the first half of 2024 when the Fed’s rate hikes begin to take a larger bite out of economic growth.

The Stock Market

The soft-landing narrative helped drive stock markets higher this year into the third quarter. The S&P 500 Index of large-cap stocks in the U.S. peaked on July 31 but then fell over 6 percent through the end of September as investors began to question how much longer the good news could last. These doubts began when the data on both employment and inflation were reported to be hotter than expected. Investors viewed this as reinforcing the need for the Federal Reserve to raise rates at least one more time, and then leave them at a higher level for an extended period. Investors had been expecting slower growth would lead to lower rates in the future, so the unexpected strength in the numbers caused bond yields to surge.

This was the primary cause of the market’s about-face. Ironically, the “higher for longer” scenario is being viewed as bad for both the stock and bond markets because tighter financial conditions have the potential to more dramatically slow growth in both the economy and the jobs market.

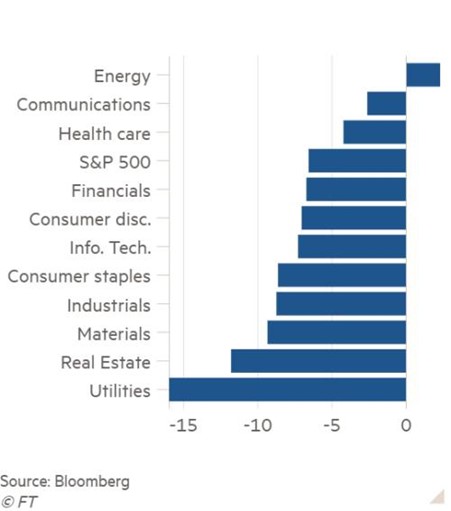

A look at the performance of the sectors in the S&P 500 Index since July 31 clarifies how the perceived need to keep interest rates higher for longer has impacted the stock market. With much higher bond yields, the sectors often thought of as bond substitutes (utilities and real estate) have performed the worst. Cyclical sectors such as industrials and materials also fared poorly, which is consistent with a slowdown in growth. The more defensive sectors such as healthcare did relatively well. Energy stocks performed the best thanks to the increase in energy prices.

S&P 500 Sector Total Return from July 31 Through September 30

The direction of stock price movements is very uncertain as we move into the fourth quarter. Stocks could regain their momentum through the end of the year, but next year might be a different story. It seems that there are two potential outcomes for the economy in the near term, and neither one is likely to be supportive of further stock market gains in 2024.

The first scenario would be if the strong data on both employment and inflation continues. The recent spike in energy prices is causing inflation to remain stubbornly high, and employment remains healthy. The “higher for longer” sentiment which has gripped the market since July 31 could continue. The resultant tightness in financial conditions could cause a more severe recession in 2024, which would lead to falling stock prices.

On the other hand, the rate hikes could more broadly begin to impact the economy and the signs of weakness could accelerate. The coincident and lagging indicators would also begin to weaken along with the leading economic indicators. This would likely mean that the recession will begin early next year but be relatively short and shallow.

We believe the second scenario is more likely. In addition to all these headwinds facing the consumer, the lagged effects of Fed rate hikes will soon be more fully felt. As a result, stocks will probably struggle as the new year begins. However, stocks typically begin to recover well before the recession is over, so the good news is the drop in stock prices would be less severe and should recover sooner if this scenario occurs.

The Bond Market

It has been a similar story in the bond markets in 2023. For most of the year, investors were expecting that lower inflation and higher unemployment would cause the Fed to begin cutting rates sometime in mid-2024, but in September investors sensed that interest rates would need to remain higher for a longer period of time.

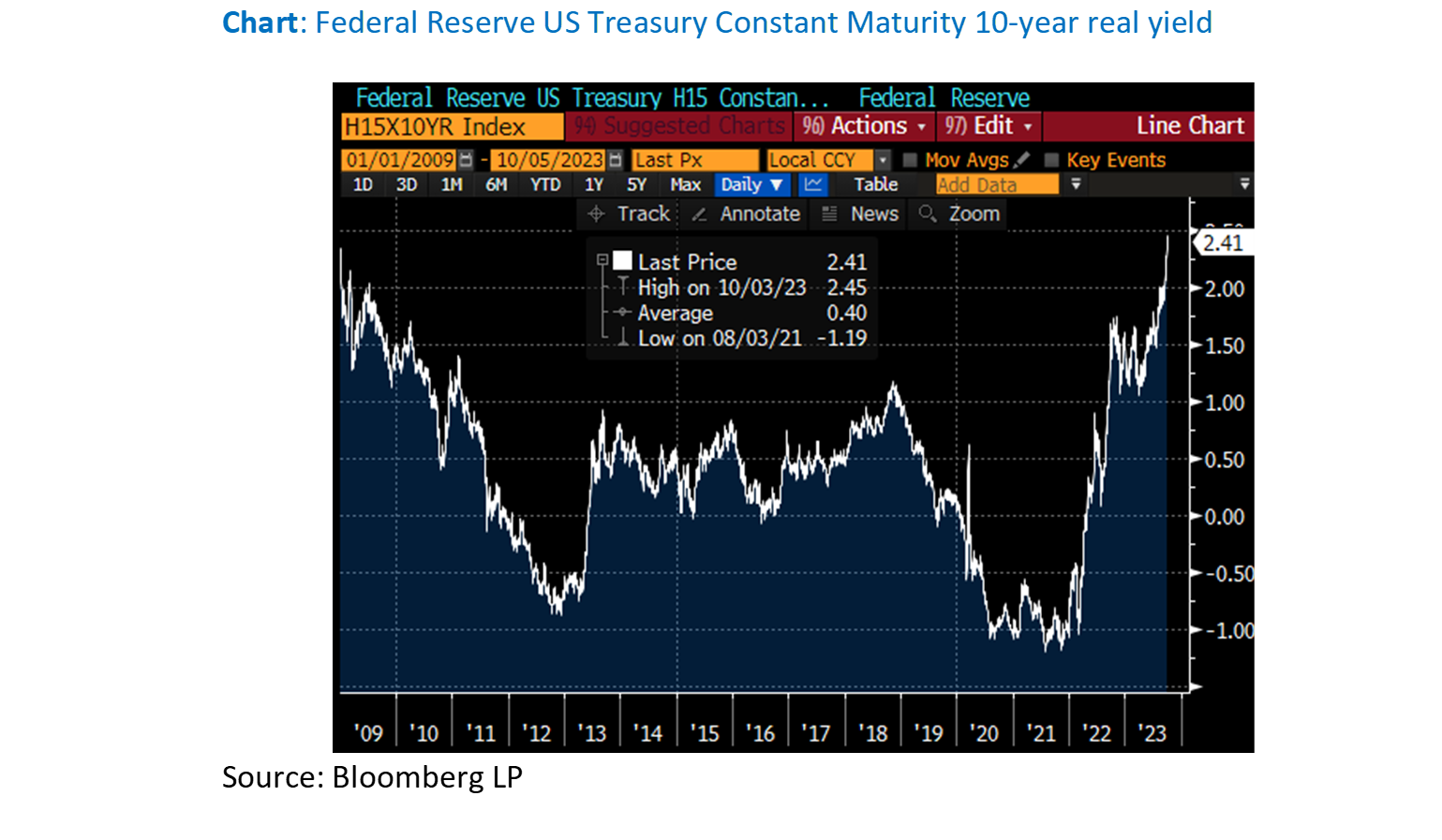

The result in the bond market was longer-maturity Treasury yields moved materially higher, and shorter maturity yields stabilized. Real yields have jumped to a post-global financial crisis high due to a combination of lower inflation and higher nominal yields.

With economic growth likely to slow in 2024 as the lagged effects of Fed tightening take hold, core fixed-income strategies offer an attractive risk/return profile. The possibilities of a slowdown in economic growth as well as stress caused by restrictive monetary policy are likely to be supportive of bond price appreciation.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.