Weakening Economic Data Indicates Recession Will be Delayed but Not Sidestepped

Earlier this year, I wrote that we expected the Federal Reserve’s rate hikes to bring about a recession around the fourth quarter of 2023. Many of the talking heads on business news channels also had been predicting the US economy would fall into a recession in either late 2023 or early 2024. Many of these same people are now saying a recession will be avoided, with economic activity remaining solid despite higher rates and falling leading economic indicators.

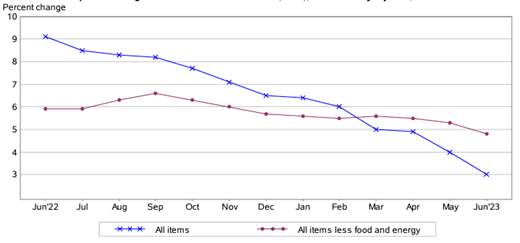

The news has been good on the inflation front in the United States as well. The Fed’s goal in raising interest rates is to slow growth and bring inflation down to its targeted rate of 2 percent. While inflation has not dropped to that target, inflation is finally cooling. The Consumer Price Index (CPI) rose a less-than-expected 0.2 percent in June. It was up only 3 percent from a year ago, the lowest level since March 2021.

One-Month Change in CPI, Seasonally Adjusted

Source: The Bureau of Labor Statistics

Some of the underlying data was also encouraging. Used car and core goods prices fell, and rental inflation rose very modestly. The one potential trouble spot is core inflation, which had been coming down more slowly. While core CPI also rose less than expected, it is still too high at 4.8 percent. As a result, the Fed is still likely to raise rates at least one more time this year before they are finished despite the signs of slowing growth and the lag of prior tightening. Typically, it takes twelve to eighteen months for the full effect of monetary tightening to be felt on economic activity. The first rate hike in the current cycle occurred on March 17, 2022, or about sixteen months ago, so the first few rate hikes are just now starting to impact the economic data. However, the Fed won’t stop raising rates until there is definitive evidence that inflation is under control.

The U.S. economy, along with the economies of most developed countries, may have achieved the soft landing that the Federal Reserve has been trying to generate with its monetary policies. Several tailwinds have kept the U.S. economy growing despite higher interest rates.

- Receding inflation and the resilient labor market is boosting consumer confidence. The University of Michigan’s preliminary survey of consumers jumped to its highest level since September 2021.

- Flush with cash and anxious to get out of their homes after the COVID lockdowns, consumers are spending on air travel, hotel stays, and dining in restaurants. Consumers are also beginning to spend again on household durables.

- The labor market remains healthy because there continues to be a shortage of workers. The strong job market has made people more optimistic about both current economic conditions as well as their future expectations.

- Long-term loans are locked in at lower rates, so higher interest rates aren’t having much of an impact on spending by both businesses and consumers.

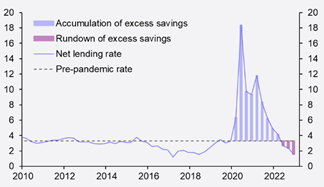

However, these tailwinds are likely to fade toward the end of the year. From March 2020 to August 2021, consumers amassed $2.1 trillion in excess savings, but those excess savings are dwindling. Consumers are not flush with cash anymore, and higher rates are impacting consumer spending. The Restaurant Performance Index has sharply declined in recent months. Credit card and auto loan delinquencies have started to rise, and consumer spending on big ticket items such as furniture and appliances is slowing. Banks are tightening their lending standards, so loans are not only more expensive due to the Fed’s rate hikes but also harder to obtain.

Average Household Savings as a Percent of Income

Source: Capital Economics

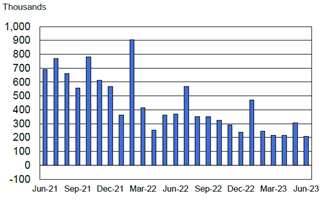

For most of the year, the labor shortages have been so severe that the Fed’s rate hikes have possibly slowed additional hiring but haven’t caused a substantial rise in unemployment. More recently, the labor market is beginning to show signs of cooling, although it is still tight by historical standards. The June Employment Situation Summary release confirmed that the U.S. economy added the fewest jobs in two and a half years during the month and lowered the number of jobs created in April and May. There was also an increase in the number of people working part-time in June, partly because their hours had been reduced due to slower business conditions. While there are still plenty of jobs, the US Federal Reserve has made it clear they will raise rates at least one more time this year and maybe more if inflation does not fall more rapidly. An uptick in unemployment seems probable if the Fed follows this path.

Monthly Change in Nonfarm Payroll Employment

Source: The Bureau of Labor Employment Situation Report – June 2023

Another factor contributing to the resilient economy is the fact that many corporations extended the maturity of their loans during the pandemic, and households have 30-year fixed mortgages at low rates. 51 percent of consumer mortgages in the United States have an interest rate of 4 percent or below. As a result, the impact of higher rates on economic activity has been muted. However, going forward companies may not be willing to take on new loans at higher rates to make capital investments in their business. This could lead to businesses operating at less than full capacity.

Also, consumers may feel stuck in their homes and will not be able to afford to trade up because of the current higher mortgage rates. The lack of demand for housing would lead to fewer homes being built and sold. The end result would be lower economic activity from both businesses and consumers. This is just one example of why it takes a while for the full effect of monetary tightening to be felt on economic activity.

While growth is slowing, economic activity should remain positive for the rest of this year. Inflation can continue to drift lower as long as the labor market remains tight. The lagged effect of the rate hikes could result in fewer job openings and softer wage growth, but not necessarily higher unemployment. These conditions could continue to provide a tailwind for consumption over the coming months.

However, once unemployment begins to tick higher the tailwinds from the consumer may fade. Growth is not likely to persist into next year as the lagged effect of the Fed’s rate hikes will slow growth over the coming year. The start of the much-anticipated recession is likely to be delayed until 2024, not avoided altogether. Any additional rate hikes by the Federal Reserve this year could make a 2024 recession more severe. The good news, however, is the slowdown should allow inflation to fall more rapidly next year.

So what does that mean for the stock and bond markets? As always, it is nearly impossible to predict the path forward for the stock market, especially in the short term, because many variables could exert some influence on the market’s direction. Is the Fed on its way to guiding the economy to a soft landing? Will the momentum of the seven stocks that are driving the market higher continue? Will inflation come down fast enough for the Federal Reserve to halt its rate hiking campaign? Will consumer spending continue to weaken? Will investors remain confident enough to keep buying stocks?

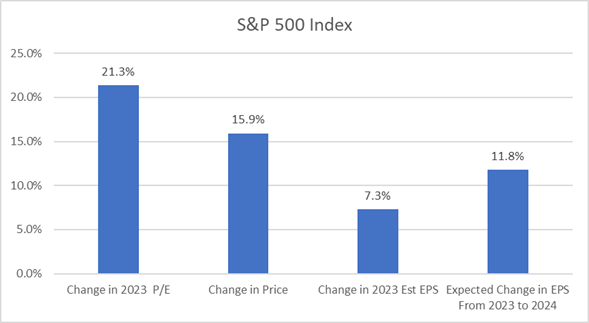

This year is a good example of how emotion can drive stock prices in the short term. Long-term, growth in corporate earnings per share (EPS) is the primary driver of stock market returns. This year stock prices have risen faster than the growth in corporate earnings, which has caused the Price to Earnings (P/E) multiple to expand. EPS for S&P 500 companies is only expected to grow 7.3 percent this year. But the S&P 500 Index has returned 15.9 percent through June 30. The P/E ratio for 2023 has gone from 16.77 up to 20.35.

Source: FactSet

The prevailing sentiment that has helped drive stock prices higher is that the Fed will achieve an economic soft-landing and inflation will fall to a level where the Fed will stop raising rates after one more rate hike. This rosy narrative could persist for the rest of this year, keeping investors’ confidence in the stock market high. Though economic growth is slowing, it still should be solid enough for stocks to add to their gains in the second half of the year. Earnings are expected to rebound in the second half of 2023, providing support for further gains in stocks.

Longer term, the variables that mostly relate to investors’ emotions and market sentiment tend to be trumped by the fundamental growth of the company’s profits. When stock market prices increase in the short term much faster than corporate EPS, it usually means investors expect an acceleration of earnings in the future. So, the good news must continue next year if the market is to keep rising.

Next year could be a difficult one for the stock market because estimates for EPS growth for 2024 may be too optimistic. Analysts currently expect corporate earnings per share for S&P 500 companies to grow 11.8% in 2024. Given the headwinds to economic growth next year (lagged effects of Fed rate hikes, higher interest rates, tighter lending standards, and lower consumer savings), earnings are likely to fall short of those expectations. If corporate earnings do not live up to the high expectations, the gains in stock prices in 2023 could evaporate in 2024. So while stocks should remain on an upward trajectory for the rest of this year, next year could be a different story.

In the bond market, shorter maturity bond yields have been pressured higher in the first half of 2023 by the Fed’s efforts to return inflation to its 2% target. Bond investors continue to bet that the Fed will be lowering rates sometime within the next 12-18 months. This dynamic has caused the Treasury yield curve to remain inverted for an extended period. Longer maturity Treasury yields are lower than where they began the year despite 75 basis points of additional rate hikes in the first half of 2023. Five-year maturity Treasury Inflation Protected Securities (TIPS) have been pricing future inflation rates to be somewhere between 2.0-2.5% since last summer.

We believe that the Fed is very close to being done raising short-term interest rates due to a combination of continued progress on the inflation front as well as our expectation of the lagged effects of aggressive global monetary policy tightening will slow economic activity in the next 6-12 months. We see value in the US fixed-income market with Treasury yields hovering around 4% across the curve while future rates of inflation are likely to be below that level. This offers investors a positive “real” yield for the first time since early 2019 as well as the highest yields since before the global financial crisis.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.