Student loan availability has changed over the last 20 years. Options for future generations are more limited. As well, costs continue to increase, an average of 3.11 percent annually from 2010 to 2020 for a four-year college.

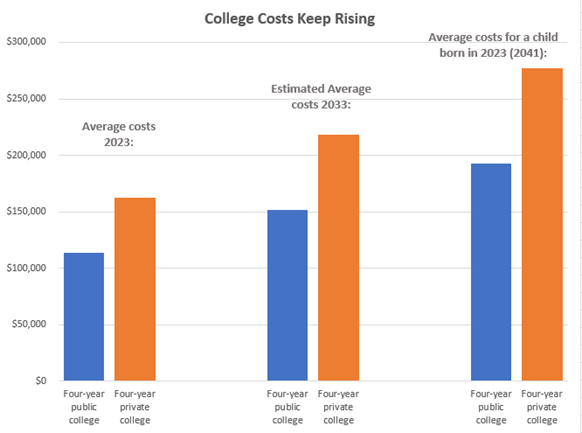

For those with household incomes of $110,000 or more, the estimated net cost after grants and aid for a four-year public college is $113,338, $162,866 for a private school. The current limit on four years of federal loans, including subsidized and unsubsidized loans, for a dependent undergraduate is $27,000. As such, a student will need an additional $86,000 for a public college or $135,000 for a private college for their four years.

That’s the estimate for a student starting in Fall 2023. It will only get more challenging. The estimated average net four-year cost in 10 years before federal loans will be $152,000 for a public college and $218,000 for a private school. In 18 years—that is, for 2023 newborns—costs will have risen to averages of $193,000 for a public college and $277,000 for a private college four-year education. Whatever is not funded by savings or cash flow will likely be funded by private student loans, which will require a co-signer unless the student has a qualifying credit history and an approved amount of earned income.

Source: Pennsylvania College averages from 2020 used and calculated with a 3% inflation rate.

How does all that translate when it comes to paying back student loans? For a freshman entering college this fall borrowing the full amount, including the federal student loans, and assuming a best scenario 5 percent interest rate over 20 years, their loan payments will be an estimated $748 per month (public school) or $1,074 per month (private school). The number of financial institutions that consolidate loans has also dwindled over the last 20 years due to higher default rates, meaning there is not as much competition to work in a student’s favor.

529 plans and savings

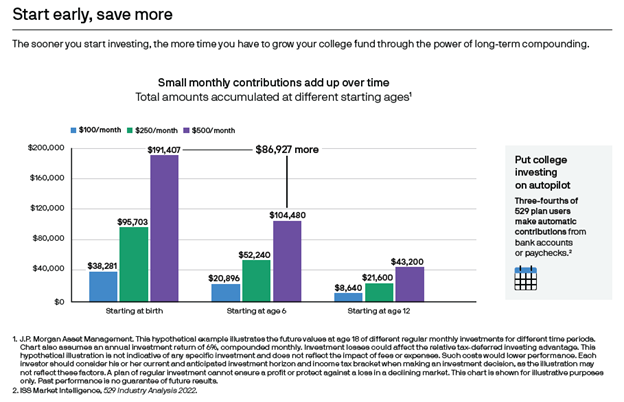

529 plans are excellent tools for saving for college, especially if they are started early in the student’s life. Ultimately they are after-tax dollars—and many states allow deductions for contributions—that grow tax deferred. If the gains are used for qualified education expenses, they are tax-free. In a scenario where $500 per month is saved for 18 years—a total of $108,000—given a 6 percent annualized return, the account would be worth $193,676, including the gain of $85,676 that will not be taxed as long as the money is used for qualified education expenses.

Qualified college education expenses include:

- Tuition and fees (for all eligible institutions)

- Books and supplies

- Computers, software and internet

- Room and board (must be enrolled and attending at least half 50 percent of the time)

- Special needs equipment

- Student loans (a lifetime limit of $10,000)

The student must attend a qualifying school, which includes colleges and universities, but also vocational and trade schools. Public, private, and parochial elementary and secondary schools also qualify for up to $10,000 per year of untaxed dollars used for expenses. As long as the institution you’re enrolling in is eligible for Title IV federal student aid, you can also use a 529 plan to pay for online tuition and fees.

Leftover funds

There are no time or age limits for using a 529 college savings plan. Money can be kept in a 529 plan indefinitely. If there are 529 funds left over after education expenses are paid, the money can be used in a variety of ways:

For additional education, such as to pursue a master’s or doctorate degree

For another student, a qualified family member of the original beneficiary:

- Spouse

- Son, daughter, stepchild, foster child, adopted child or a descendent

- Son-in-law, daughter-in-law

- Siblings or steps-siblings

- Brother-in-law, sister-in-law

- Father-in-law, mother-in-law

- Aunt, Uncle or their spouse

- Niece, nephew or their spouse

- First cousin or their spouse

As tax-free 529 distributions to pay off student loan debt up to a lifetime limit of $10,000 (a provision of the SECURE Act)

To be saved for the education of future generations (an opportunity to establish an educational legacy for your grandchildren)

In some cases, as a non-qualified withdrawal with no penalty tax on the earnings, such as when the beneficiary dies, becomes disabled, or attends a U.S. military academy

If your child gets a scholarship, up to the amount of the award to spend on anything you like (investment account gains taxed as income)

As of 2024, to roll over into a Roth IRA for the account’s beneficiary without incurring taxes or penalties (up to $35,000, subject to annual Roth IRA contribution limits [$6,500 in 2023]; a provision of SECURE 2.0 Act). Additional stipulations include:

- You must have owned the 529 educational savings account for at least 15 years before you can roll over the money.

- You can only roll over money that’s been in the account for five or more years.

- The account holder, typically a child’s parent or guardian, can’t roll over the money into their own Roth IRA. It must be an account established for the beneficiary of the 529 plan.

As a wealth advisor, I do not advise my clients to rob from their retirement savings to fund their child’s or grandchild’s education. However, if the money is available, or you can make room in your budget to put aside an amount on a monthly schedule, 529 savings are an excellent way to reduce the financial burden of student loans your children might face in the future. Parents may be inclined to think, “My kids will borrow money to go to college like I did.” However, be aware that loan access and options have changed significantly and the resulting burdens on graduating students have increased substantially.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.