Traditional economic theory held to the concept that investors act rationally, that we make rational choices in our effort to maximize profitability and achieve our investment goals. Then in the 1970s and ‘80s, an emerging study rooted in psychology, “behavioral finance,” revealed more about how investors actually make financial decisions. It’s probably not surprising that researchers discovered that humans are not always rational. We tend to make decisions based on emotion and cognitive biases, one of which is “recency bias,” whereby we rely heavily on recent events, experiences that are fresh in our minds, to make choices. It seems we are hardwired to do so; our brains are designed to access and prefer the most available information instead of doing the hard work of analyzing long periods of the past. We’ll pull from the quickest information available to make the quickest decisions.

For investors, recency bias leads to decisions based on short-term rather than long-term performance. It encourages investors to chase market trends. We’ll identify an asset class that has performed well recently and assume that performance will continue. The result is that the investor buys assets at their peaks, their highest prices. It can also result in an investor putting all, or at least too much, of their assets into a single stock or asset class instead of diversifying.

Consider that in 2019 financial services was one of the best performing sectors in the S&P 500 Index, delivering an annual return of 32 percent. In 2020, that sector returned -2 percent, while the S&P 500 Index returned more than 18 percent.

Source: https://novelinvestor.com; NovelInvestor.com

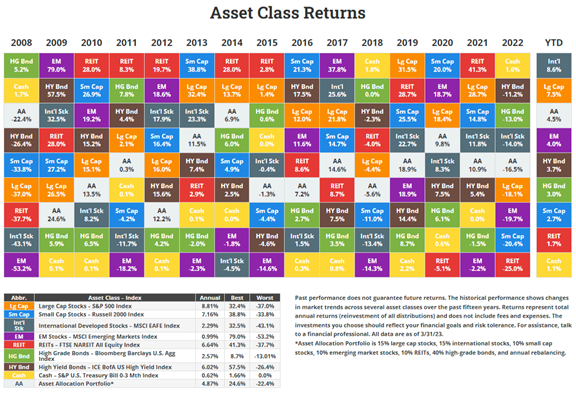

The performance of each asset class in comparison to others over the years demonstrates how performance of a particular class varies from year to year. Hence the cautionary warning: “Past performance is no guarantee of future returns.”

FOMO

Recency bias can be exacerbated by a fear of missing out (FOMO). As opposed to considering the underlying value of a stock or investment, the investor buys it or avoids it because others are. That can result in buying at the highest price, or not buying when the investment is at a discount. We’re reminded of the movie JAWS, how many people avoided the water that year despite 50 years of history of the slightest chance that you would see much less get bit by a shark.

An essential role of your advisor is to design a target asset mix that supports your financial goals, risk tolerance, and time horizon. The percentages of the mix are not stagnant as the values of the difference asset classes grow and change over time, so your advisor restores your target asset allocation by routinely rebalancing your portfolio.

For example: A portfolio is designed for a 40 percent allocation of U.S. large-cap stocks. Over time the value of those stocks grows to 55 percent of the portfolio value. If left unchecked this increased weighting to equities alters the risk profile of the portfolio. The advisor trims 15 percent of U.S. large-cap stocks gains, then buys something out of favor, something undervalued, thereby rebalancing the portfolio to its proper allocation with investments priced at a discount.

It’s a common theme of Warren Buffet’s, that investors should be “fearful when others are greedy, and greedy when others are fearful.” That contrarian view on stock markets relates directly to the price of an asset. When others are greedy, prices typically boil over, and you could overpay for an asset that subsequently leads to anemic returns. When others are fearful, that could translate to a high-value opportunity.

As financial advisors, we want our clients to stick to their financial plans, sound financial plans that target long-term goals, part of those plans being reallocation. In our meetings with our investor clients, we focus on long-term performance of their assets as a way to negate recency and other biases. Of course, people can be concerned, or fearful, when markets are down, but we ask our clients to hold off on rash decisions. As the much quoted Benjamin Graham, the so-called “Dean of Wall Street,” noted, “The investor’s chief problem—and even his worst enemy—is likely to be himself.”

Markets are cyclical

Your plan shouldn’t change based on a current event. The market works in cycles, and it’s important not to act on fear or greed, selling in a down market or chasing yesterday’s winners. Recency bias clouds our judgment and can derail us from our financial goals.

Instead, investors should think long-term. Stay connected with your financial advisor, reviewing your plan regularly to stay on course toward your long-term goals. Consider an investment, whether you’re buying a business or a stock, as something you see yourself holding for ten years. It’s the difference between investing and speculating.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.