However, Stocks Can Still Finish the Year in Positive Territory

The first quarter of 2023 was marked by so many changes in the outlook for the economy that it reminds me of last year’s most-awarded movie. But even though it seemed as if changes were occurring in “Everything Everywhere All at Once” all the changes brought most economists’ views on where the economy is headed back to where they were at the beginning of the year.

In January, most economists believed that a recession would occur in 2023 with the U.S. Federal Reserve continuing to raise rates aggressively even as the economy was already weakening. By the end of February, however, the U.S. economy was showing signs of recovery. Consumer spending was strong thanks to a resilient job market and rising wages. Corporate earnings were strong despite higher interest rates and falling profit margins. This prompted many economists to sense that a recession would be avoided, and the “soft landing” scenario may be achieved.

That all changed on March 10th, when Silicon Valley Bank (SVB) closed due to a run on its deposits. The bank’s failure was caused by several issues unique to SVB, which was the bank of choice for many Technology start-ups. As these companies were being flooded with cash, SVB went from $60 billion in total deposits to nearly $200 billion in just two years. SVB invested these deposits in longer-term U.S. Treasuries and mortgage-backed securities. At the same time, the Federal Reserve substantially raised interest rates to combat inflation. This caused two problems: the value of the investments fell, and startup funding became more difficult and more expensive to access. SVB’s clients needed to withdraw their cash, forcing SVB to sell bonds to fund the withdrawals that had lost value due to the interest rate increases. SVB was eventually purchased by First Citizens Bank after it accrued $1.8 billion in losses.

Other banks also have unrealized losses in their investment portfolios, but most have key differences from SVB and Signature. Larger banks are deemed to be safer because they are viewed as “too big to fail” by the Federal Government and so their clients would be protected in the event of a run on deposits. Most mid-sized banks have a more diverse clientele, and their clients’ accounts typically are smaller and fully covered by FDIC insurance.

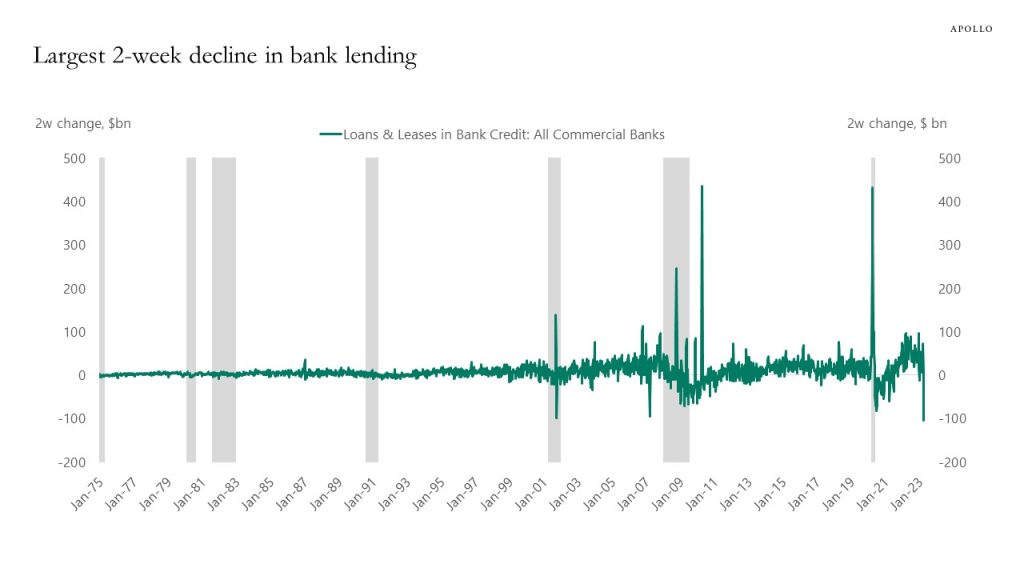

Still, the fear of more bank failures has caused all banks to tighten their lending standards, resulting in many fewer loans being made. In the two weeks after the bank failures there was a dramatic downturn in loan volumes.

Source: Apollo Global Management, Inc., Federal Reserve Board, Haver Analytica

The strength in the economy is fading, and tighter lending standards will cause economic growth to slow further. Still, the Fed hiked rates by 25 basis points at its March 22nd meeting even though the problems in the banking industry highlighted the dangers of the unprecedented speed at which the Fed was raising rates. By the end of the first quarter, most economists were back where they started the year – with the sense that the U.S. economy is heading for a recession in 2023. The recent economic data supports this view.

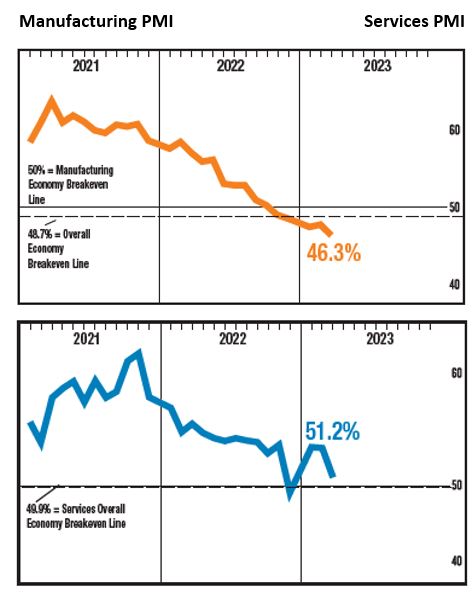

The U.S. manufacturing sector fell deeper into contractionary territory in March, shrinking for the fifth month in a row. At the same time, the service sector dropped in March, falling closer to contractionary territory.

Source: The Institute for Supply Management

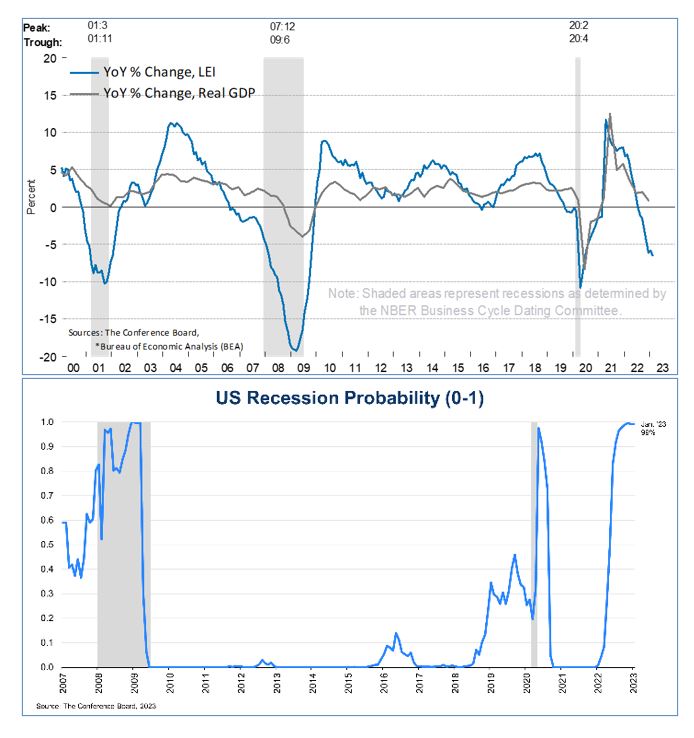

The Conference Board Leading Economic Index (LEI) for the U.S. fell for the eleventh month in a row in February and will likely continue to fall in the coming months when the tighter lending standards will begin to be reflected in the data. The Conference Board forecasts a 99 percent chance that the US economy will dip into recession in the next twelve months. The turmoil in the banking industry probably shortens that time frame.

The Annual Growth Rate of the US LEI Continues to Fall, making the Likelihood of a Recession near 99 Percent

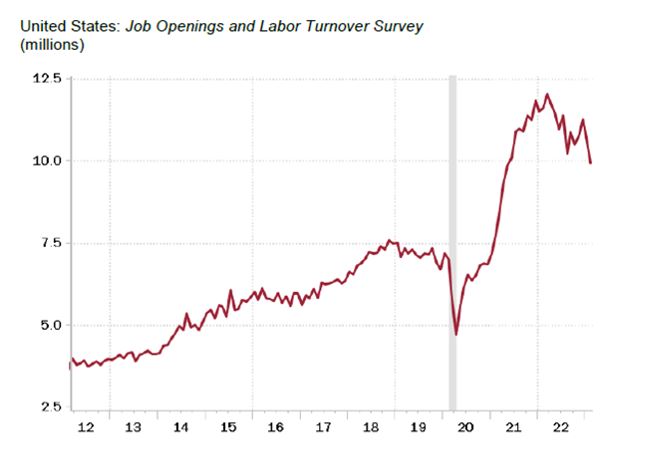

In the jobs market, private payrolls rose less than expected in March as employers in the United States pulled back from a year of strong hiring. Pay growth, after a three-month plateau, is inching down. The Job Opening and Labor Turnover Survey (JOLTS) showed sharply reduced job postings and new hirings, especially in the retail sector. This should ensure that if the Fed does raise rates one more time in May, it will be the last one of the cycle.

The Employment Situation is Deteriorating

Shading indicates recession

Source: Haver Analytics, Rosenberg Research

The combination of higher rates and tighter lending standards also will likely lead to lower inflation. For the first time in eleven years, home prices are dropping. Rental amounts are now either flat or declining in most parts of the United States as property owners are not able to raise rents anymore. This data has not been reflected in the Consumer Price Index but will be going forward.

It seems imminent that the economy will slip into recession soon if it has not already. Still, the recession should be mild and short because of the underlying strength in some sectors of the economy. Consumers and businesses are still flush with cash, so when the Fed stops hiking rates, they could resume spending. Interest rates should come down as growth slows and the Fed stops raising rates. The problems in the banking sector will exacerbate the slowdown, but do not appear to be the start of a systemic crisis due to the specific issues the failed banks were facing.

A recession would likely lead to a lower stock market in the near term but could set stocks up for a recovery by the fourth quarter of this year. In the first quarter, stock markets in the United States ended mostly higher in rollercoaster trading. The S&P 500 Index was up over 6 percent in January as investors became optimistic that the economy would continue to grow even as inflation was peaking. In February, however, the Federal Reserve hiked rates another twenty-five basis points at the FOMC meeting, and Chairman Powell reinforced the need to keep interest rates higher for longer. Stocks fell as investors focused on the expectation of higher long-term interest rates and weaker corporate profits.

March began with stronger-than-expected economic data, strengthening the idea that economic growth can continue despite the Fed’s rate hikes. Stocks rallied to start the month, but then the rapidly evolving banking crisis intruded on this narrative. After SVB and Signature Bank shut down, several others also seemed vulnerable – especially First Republic Bank. Federal Regulators stepped in to backstop all depositors at SVB and Signature and facilitated their sale to First Citizens and Flagstar Bank, respectively. Meanwhile, the political leaders in Washington DC debated whether current regulatory oversight is sufficient and whether Federal Deposit Insurance Corporation (FDIC) limits should be increased.

These actions calmed the situation, though there is the potential for another shoe to drop. For example, there will be a lot of attention on bank earnings this quarter, with a particular focus on their commercial loan portfolios. However, stock market investors have turned their focus back to their expectations of how high the Federal Reserve will hike rates before stopping, which has been the determining factor in whether the stock market trades up or down.

When economic data has been strong, investors assume this means the Fed will raise rates more aggressively, causing stocks to fall. On the other hand, when the data has shown growth is slowing or inflationary pressures are easing, stocks rise as investors assume this means the Fed will soon stop raising interest rates. This mindset is the reason stocks rallied during the second half of March despite tighter lending standards. As bank lending falls, growth will slow and the investors believe this means the Fed can stop raising rates.

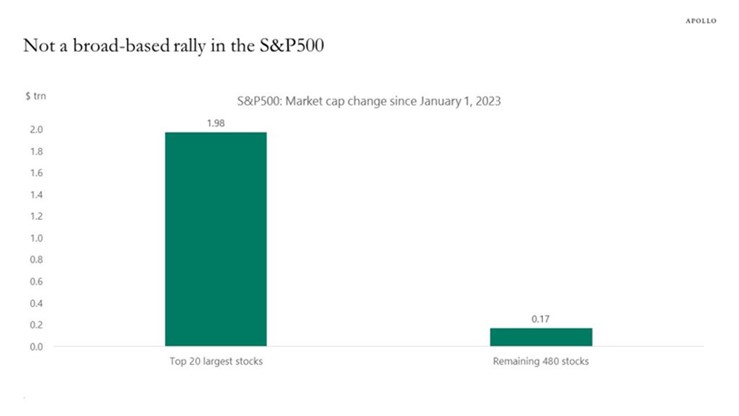

As a result, the stocks in the sectors that benefit the most from lower interest rates, such as technology stocks, were up almost 11 percent during the first quarter. In fact, since the beginning of the year, the S&P 500 Index was again driven by only twenty stocks, mostly in the Technology sector. The remaining 480 stocks in the index had very minimal performance. The implication is that this market is not being led by broad-based growth expectations but instead by speculation about when Fed will stop raising rates.

Source: Apollo Global Management

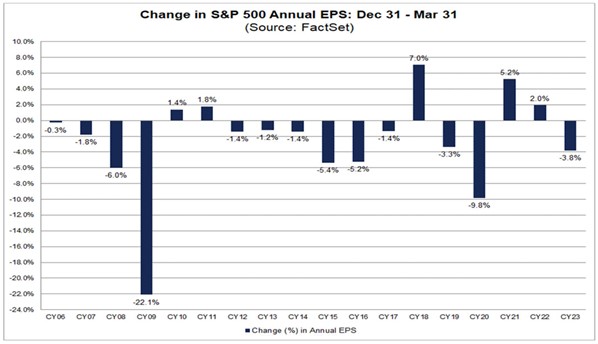

This trend could continue, at least until the Fed stops raising rates, probably at the May FOMC meeting. At that time investors are likely to turn their focus to corporate profits, where the picture is not particularly good. During the first quarter, Wall Street analysts lowered their earning estimates for S&P 500 companies by 3.8%, which is larger than the twenty-year average.

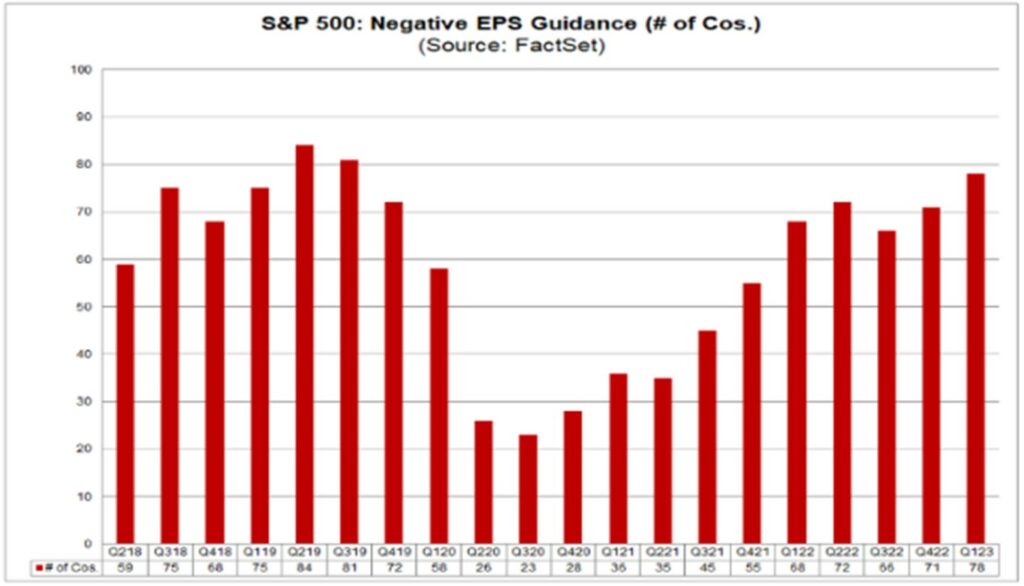

The companies themselves have also been lowering their earning estimates. In fact, the first quarter has seen the highest number of companies in the S&P 500 Index lowering their Earnings per Share guidance since 2019. It seems likely these estimates will need to come down even further as companies will continue to face higher input costs, higher interest rates and tighter lending standards.

Both Corporations and Analysts Have Been Lowering Earning Estimates for 2023…Is more to come?

Source: FactSet

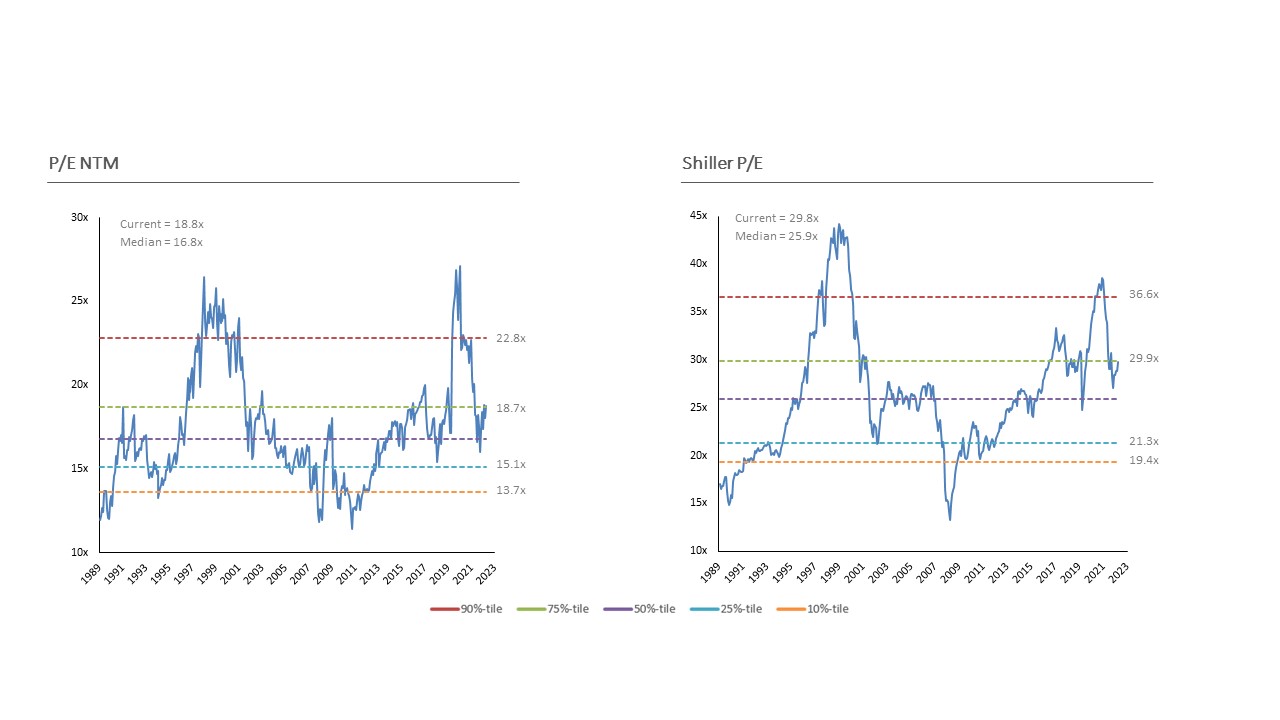

These headwinds to corporate profitability, combined with stock market valuations that are still above their long-term averages, mean that stocks will probably fall once it is clear that a recession will occur, possibly retesting their lows of last year. Stocks usually do not begin a sustained recovery until the recession has begun and valuations have retreated below the average historical Price to Earning level. Also, the market typically peaks before a recession and bottoms after the Fed stops hiking rates.

Bloomberg and Robert Schiller as of March 31, 2023

Fortunately, the recession is likely to be short, so stocks could begin to recover before the end of the year. In fact, stocks usually do well in the twelve months after a Fed pause. When the Fed stops raising rates, inflation and interest rates will have leveled off at modestly higher levels and growth expectations will be more reasonable. Valuations will also be more reasonable. The strong balance sheets of both corporations and consumers could drive a recovery in spending, leading to stronger growth and higher stock prices in the latter part of the year.

Our advice for long-term investors is to stick to your disciplined plan, which includes a strategic allocation to stocks and bonds. This can be difficult to do after a year when a traditional portfolio of stocks and bonds performed miserably last year. However, last year’s high inflation, rising interest rates, and sky-high valuations led to a poor year in most asset classes. Going forward, both stocks and bonds should do well once the Federal Reserve stops raising rates and the recession is almost over. We may see a lot of volatility in the short term, but patience will be rewarded.

Higher net worth investors should also look into the private markets for investment opportunities. An allocation to some top fund managers in the private equity and private credit space can add value to a long-term portfolio allocation.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.