The Economy

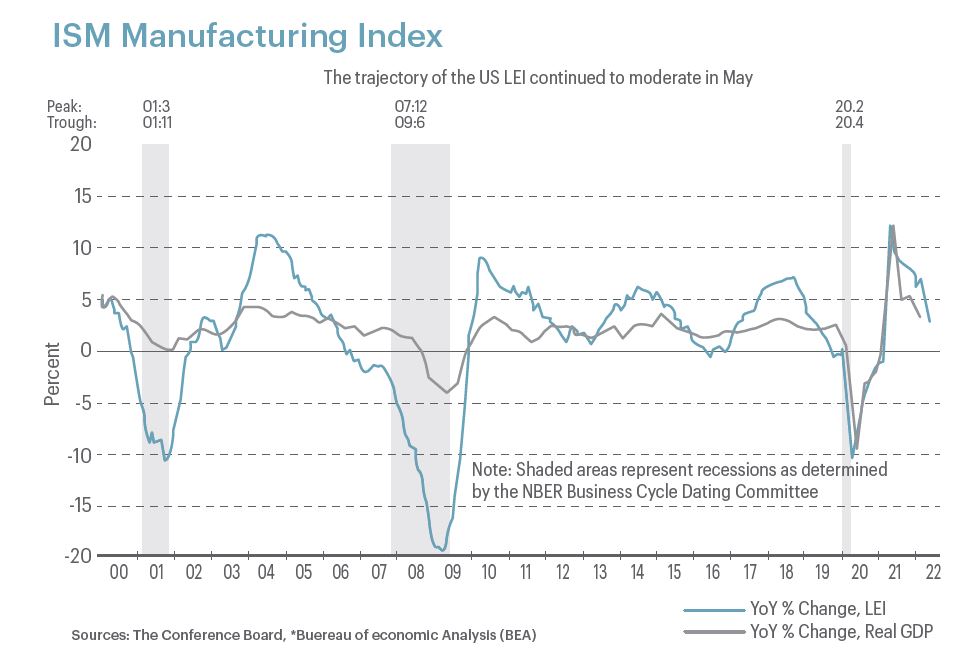

The U.S. economy probably posted little to no growth in the second quarter, with most estimates landing between a slight contraction to very small growth. This follows a first quarter in which GDP fell 1.5 percent in the United States. At the end of June, many signs are beginning to emerge which paints a picture of an economy that is slowing but not yet in a recession. The ISM Manufacturing index remains in expansionary territory but has dropped to the point where it will signal contraction later this year if current trends hold. And the Conference Board’s Leading Economic Indicators have clearly topped and are trending lower.

Chart: The Trajectory of the U.S. LEI Continued to Moderate in May 2022

Chart: The Trajectory of the U.S. LEI Continued to Moderate in May 2022

But while growth is slowing, the June Consumer Price Index reported a surprising 9.1 percent rise, the highest since 1981. The persistent surge in inflation caused the U.S. Federal Reserve to raise rates 75 basis points at its June meeting. They now expect to lift rates to as high as 3.8 percent in 2023, up from its projection of 2.8 percent in March.

Last quarter I noted that a recession was unlikely in the next twelve to eighteen months unless the Federal Reserve raises rates too aggressively to head off inflation. As the adage goes, economic expansions do not die of natural causes but are murdered by the Fed.

It appears that the Federal Reserve is headed down that path, making a recession during the second half of the year more likely. Chairman Jerome Powell said that allowing inflation to become entrenched may be worse than a recession. Minutes from the Fed’s June meeting reiterated that view, with the Board recognizing that continuing to raise rates could slow the pace of economic growth, but lowering inflation was seen as being critical due to the impact it has on low-and moderate-income Americans.

The Federal Reserve Board believes that the rate hikes will slow growth and push down job vacancies, but not cause higher unemployment because of the consistent strength in the U.S. labor market. The strong June jobs report showed that the U.S. economy continues to add jobs at a brisk pace, and the job openings rate is still very high. But employment is a lagging indicator, so it may not be indicative of more recent softness in the economy. Regardless, Chairman Jerome Powell and the Federal Reserve Board are so intent on saving consumers from rampant inflation they are willing to put up with some job losses if necessary to dampen the demand for goods and services and bring inflation down.

The inflation spike began during the latter stages of the pandemic when government spending accelerated, central banks loosened financial conditions, and supply chain restrictions made it impossible for retailers to keep up with the resultant rise in demand. When Russia began its war on Ukraine, inflation spiked even higher due to the interruption in the supply of crude oil and many foods. Now, both fiscal and monetary policies are tightening, and supply chain issues are beginning to improve, but headline inflation continues to remain elevated.

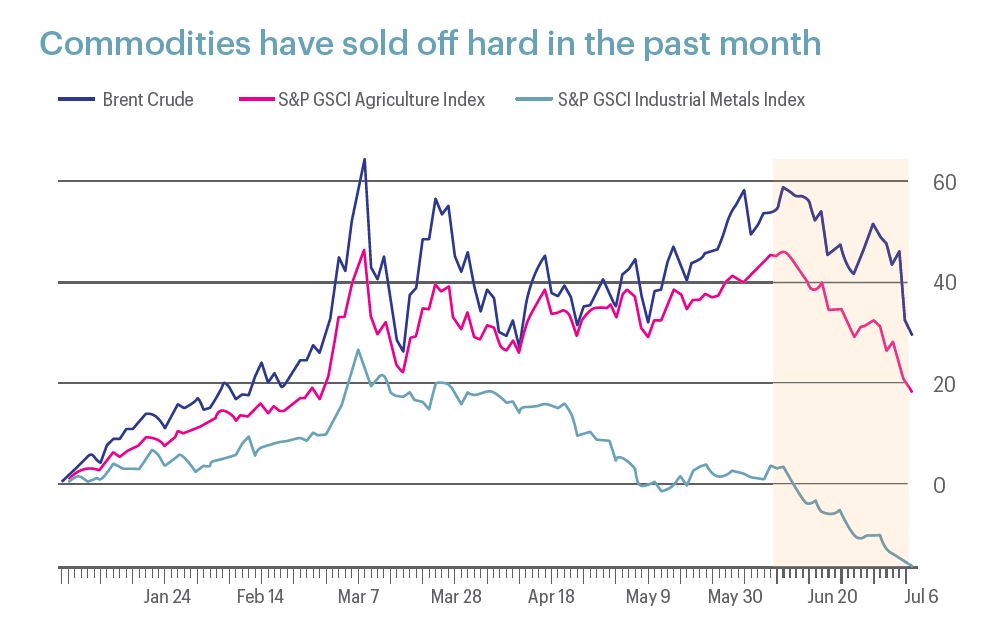

Under the surface, however, recent data shows that inflation may already be peaking and is poised to fall over the next several months. The Bloomberg Commodity Index fell nearly 10 percent in June. In particular, the price of oil, wheat and copper are all well off their highs. Mortgage applications have been falling, which will likely cause house prices to decline in the second half of the year. At the same time, corporate profit margins are shrinking, and wage growth has slowed.

Source: Bloomberg

Source: Bloomberg

Michael Burry, who was written about in Michael Lewis’ book The Big Short for his correct bet against the housing market prior to the financial crisis in 2008, tweeted recently about the “Bullwhip Effect”, and the deflationary forces that will occur in the second half of the year. The Bullwhip Effect is when retailers hold too much inventory and then need to get rid of it, so they cut prices. Retailers’ inventories had been building, but suddenly they have too much as consumers rein in spending in the face of higher energy costs. As a result, inflation could fall faster than many economists expect, and the Fed could stop raising rates well before reaching its current rate target.

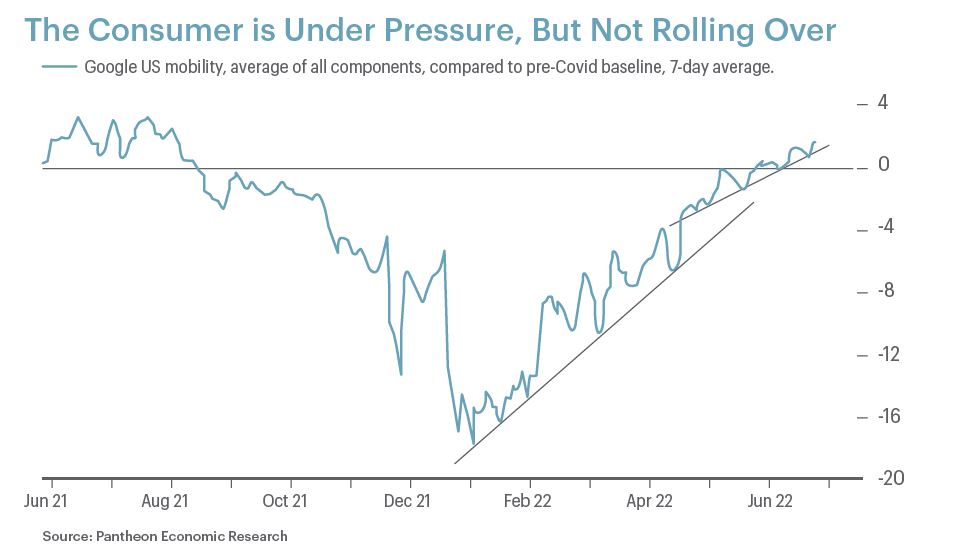

With the Federal Reserve hiking rates despite slowing growth and signs of deflation, a recession the second half of this year is now more likely. After all, Fed’s rate hikes only curtail demand but do nothing to help supply chains regain full functionality after COVID shutdowns and Russia’s war on Ukraine. Thankfully, businesses and consumers are still flush with cash, which should provide the support necessary to ensure a potential recession is mild and short-lived. Early signs show this excess cash is starting to be spent on higher gas and food prices, setting up the economy to resume growth by the end of the year.

The Stock Market

A broadly recognized threshold for a bear market is for a broad market index to drop at least 20% in price from its highs, which occurred in many markets as stocks continued to fall during the second quarter. The MSCI All Country World Index, which measures the global stock market, was down 15.5% for the quarter, putting it down 20.0% year-to-date through June 30th.

In the United States, the closely watched S&P 500 Index of large U.S. companies fared even worse, down 16.7% for the quarter. The index is down 20.9% year-to-date through June 30th. Many factors contributed to the decline, including higher interest rates, weaker job and income outlooks, and negative consumer sentiment. But the primary factor causing stocks to fall sharply is inflation, which continues to persist despite the Federal Reserve’s aggressive rate hikes. Many investors sold stocks because they believe the Fed has no choice but to continue raising rates and push the economy into recession to keep inflation in check.

The biggest question facing investors as we move into the second half of the year is whether the selling is nearing an end and when stock markets will begin to recover. As we look forward to the rest of the year, it is tempting to try to spot patterns in the charts of recent stock price action which purport to predict the future path of stock prices. This is called technical analysis. A study done by the CFA Institute Journal Review concluded that publicly available technical indicators had not proven to consistently predict future prices. Many other studies have come to the same conclusion. There are shorter periods of days or weeks when technical indicators appear to have predictive value, but not over longer periods. As a result, basing one’s long-term investment decisions on technical analysis charts will likely cause investors to make mistakes which could reduce the probability of reaching their financial goals.

When someone on a business news network is describing what “the charts” show, it is important to remember that at any point in time there are hundreds of charts that may provide conflicting signals, and the analyst is selecting the charts that support their views and ignoring the charts that conflict. Also, many charts can be interpreted in different ways depending on one’s viewpoint.

The real driver of future stock market performance is when economic data is released and there is a change in investors’ perception of the path forward for important economic data. The information gleaned from technical analysis is only useful for short time periods, until the economic data changes. The level of interest rates, the change in corporate earnings, or how expensive stocks are versus their long-term average are examples of some economic data that impact the price of stocks. Long term investors should focus on these economic data releases and pay little attention to the shorter-term signals of technical analysis.

So what is currently known about these important data points, and how might they change in a way that would impact stock prices in the second half of the year?

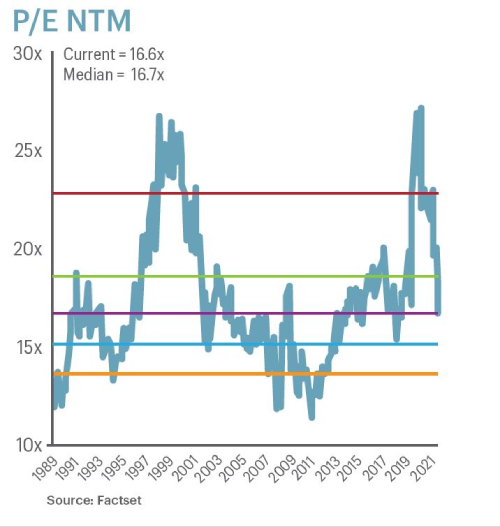

The drop in prices have brought the valuation of the market down to very reasonable levels. The Price to Earnings ratio based on earnings over the next twelve months is now slightly below its longer-term average level.

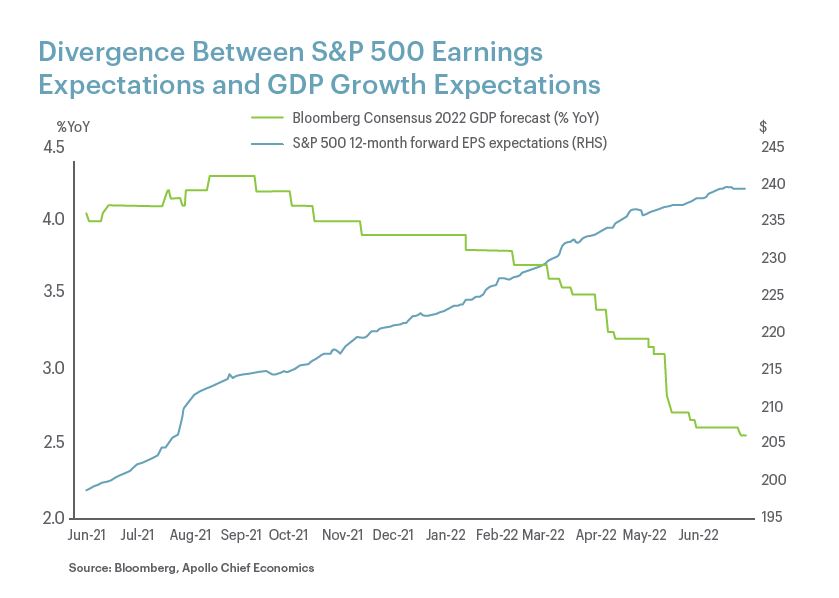

However, reasonable valuations don’t mean a rebound in stock prices is imminent. Corporate earnings growth will need to remain strong to justify that valuation, but the results may not match what Wall Street analysts currently anticipate.

Analysts expect corporate earnings for companies in the S&P 500 Index to grow by 9.6% this year, which likely would be strong enough to support a rising stock market. However, it is uncertain if that level of earnings growth will be realized. The combination of inflation, higher interest rates, slower growth from China due to their zero Covid policy, and oil supply disruptions caused by Russia’s invasion of Ukraine will cause economic growth to slow meaningfully in the second half of the year. This is being recognized by economists, who have been ratcheting down estimates for growth in Gross Domestic Product (GDP) over the next 12 months. However, slower growth has not caused Wall Street analysts to lower their expectations for corporate earnings growth at the same time. In fact, they have been raising them until very recently, when they only modestly trimmed estimates.

It doesn’t make sense for corporate earnings to be stronger if GDP growth is lower than it was when those estimates were formulated. It reminds me of Wile E Coyote in The Road Runner cartoons. Wile E Coyote regularly runs off a cliff while chasing the Road Runner and is suspended in mid-air temporarily. When he looks down and realizes his predicament, he falls into the canyon below.

It is likely that earnings growth will be cut over the next few months, which could take investors by surprise. Flows into equity mutual funds and ETFs have remained solid even as stock prices fall. Like Wile E Coyote, when investors realize the corporate profits are not there to support the market’s valuation, there could another leg down in stock prices.

While stock markets could struggle over the next few months, such a scenario would provide a decent environment for stock prices to resume rising toward the end of the year. By then, inflation and interest rates will have leveled off at modestly higher levels and growth expectations will be more reasonable. At that point, the strong balance sheets of both corporations and consumers would propel a recovery in spending, driving growth once again. So, the next several months are likely to continue to be turbulent, stocks could begin rising during the second half of the year. Thankfully, history provides some comfort. According to Morningstar, this year is the fifth time that the S&P 500 index lost 20% or more in the first 6 months of a year. The index produced positive performance in the final six months of the year every other time. The lesson is to remain patient, stay invested, and the market will recover in time.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.