After a cold, rainy, and sometimes even snowy April, spring has finally arrived here in Pittsburgh. And, as I’ve noticed in recent client meetings, people of all ages are excited to get out again. When I came to HBKS in August 2021, many of our meetings were conducted remotely or over the phone, as some clients were still uncomfortable coming into the office. Now, nearly all of our meetings with local clients have been in person.

Another trend I’ve noticed in recent meetings is that people are traveling again. And not just to a family member’s home nearby or a local lake spot, but to the West Coast, to national parks, even to Europe. Four folks in the past month have told me they are going to Italy this spring or summer. With COVID restrictions on the decline globally, people seem more excited than ever to travel.

Some folks with big travel plans have been saving up for the moment. And to those folks, kudos! But others who don’t have their savings account to the point where they can budget their dream trip can still take heart. Capital gains rates are at historically low levels, and, given the down market to start 2022, investment gains are lower—in many cases, there are losses—making it a good time, at least from a tax perspective, to take distributions.

As such, a review of the 2022 tax implications of taking distributions from a variety of investment vehicles:

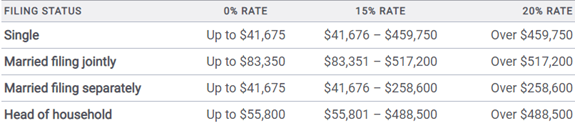

Individual/Joint Taxable Accounts and Individual Stocks

.

Traditional/SEP/SIMPLE IRA and 401k/403b

Roth IRA/Roth 401k/403b

Annuities

If you have a big trip or large expense on the horizon, and your aren’t sure of the most efficient way to fund it, contact our advisory team at 724-934-8200; or email me at bdusch@hbkswealth.com. We’ll help you develop a plan that works best for you.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.