Stock market will remain volatile until there is more clarity

The United States economy remains in good health, but cracks are beginning to show in the recovery of activity. Manufacturing is still going strong, but many other economic indicators have begun to weaken even as COVID Delta Variant infections appear to be cresting. As we move into the final few months of the year, it is still highly uncertain if the economic recovery will strengthen or shrink to a more modest pace. It is possible that growth in economic activity has already peaked, although it remains at a high level.

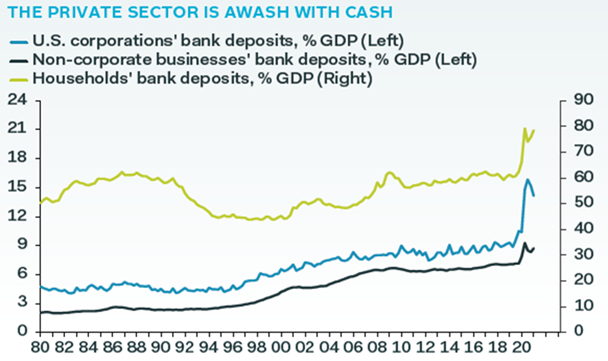

The United States Federal Government has already injected a record $5 trillion into the economy since the beginning of the pandemic, with more likely to come. However, one reason some growth data is shrinking is not all the stimulus funds have made their way into the economy yet. Cash holdings in the private sector—households and businesses—have surged since the pandemic began in March of 2020. Households in the United States are sitting on a total of roughly $2.4 trillion in excess savings, which is equivalent to about 15% of annual consumption.

Source: Pantheon Economics

While spending on durable goods spiked during the pandemic, it was not enough to use up all the excess cash. More recently spending on durable goods has fallen while spending on services has increased. However, the substantial drop in spending on services that occurred during the pandemic has only partially recovered.

Whether or not consumers decide to spend their cash will go a long way to determine if the economy will remain in above trend growth or revert to the meager growth that was happening prior to the pandemic. Unfortunately, there is reason to believe they won’t. The University of Michigan survey showed that a record number of people believe this is a bad time to be purchasing big-ticket items. The reason may be that people expect the Biden Administration to succeed in passing legislation that will raise their taxes. There is some historical evidence that the savings of consumers rise and stay high when they expect higher taxes soon.

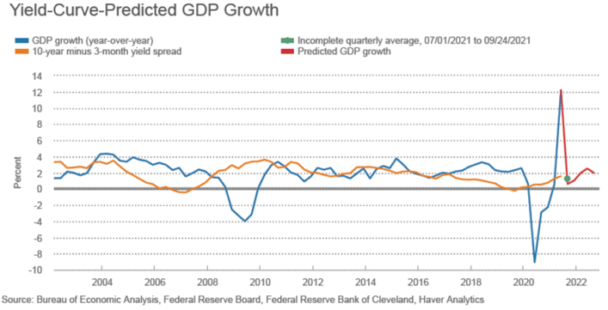

The bond market seems to believe economic growth will revert to 2% growth in GDP next year. The Federal Reserve Bank of Cleveland did an analysis that showed values of the slope of the yield curve has a high correlation to GDP growth twelve months into the future. Using September’s bond yield curve, the bond market is indicating GDP growth will be around 2 percent over the next year.

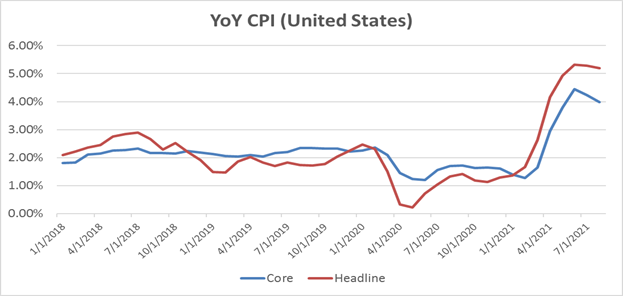

If that view turns out to be correct, the inflationary pressures in the economy will likely prove to be transitory, as Federal Reserve Chairman Jerome Powell insists. Already both the Headline and Core CPI have peaked and are rolling over. Price increases peaked in May and have fallen a bit each month since then.

Source: Factset

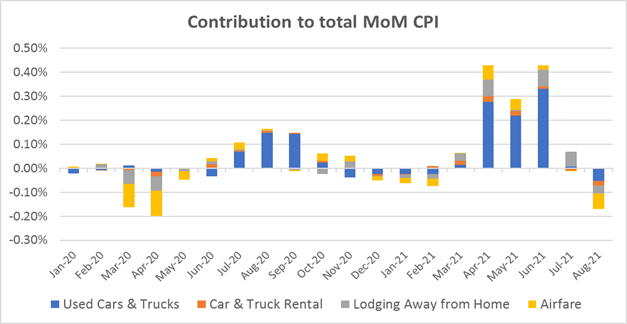

Prices in four of the most economically sensitive sectors (used vehicles, airfares, hotels, and vehicle rentals) which accounted for more than half the rise in CPI during the second quarter, barely moved in July and began to fall in August.

Source: Factset

The recent rise in energy prices has heightened people’s concerns that the inflationary pressures will continue longer than the transitory camp expected. However, it still appears that the rise in the price of energy and other costs are being caused by supply constraints due to pandemic-related shutdowns, not excessive demand. As supply chains continue to normalize, inflationary forces should continue to ease through the end of the year.

Next year, the forces that have been keeping inflation low such as aging demographics in the developed world, global competition, improvements in technology and just-in-time inventory management will likely keep inflation in check once again. In addition, central banks around the world have begun to reduce the stimulus necessary to keep the global economy afloat during the pandemic. Also, the additional debt that has been added to government’s balance sheets to boost growth during the pandemic will begin to have the opposite effect when the payments on the debt begin.

Even if the two infrastructure bills which will pump at least $3 Trillion into the economy are passed, the stimulus that has been driving economic growth will be less than it has been during the economic recovery. In the United States, Federal Reserve Chairman Powell indicated the Central Bank will begin tapering its bond purchases before the end of the year. At the same time, some government spending will plunge because the massive COVID-related support to businesses and households will not be repeated.

Corporate earnings growth remained strong in the third quarter, although global stock market performance was mixed. Stock markets rose in July and August before falling in September as investors tried to digest the inconsistent news flow. For the full year, strong earnings results have helped drive stocks higher in many markets. With the economic recovery set to continue and the Delta Variant in the early stages of fading, it is likely that earnings will continue to be strong, and stocks will churn higher the rest of the year.

But there are still a lot of contradictory data trends that make it difficult to determine if economic growth will continue to strengthen, or if the strongest growth is already behind us. For example, interest rates have risen again after falling for most of the year, the Federal Reserve was set to begin tapering its bond purchases at the same time the Biden administration was proposing $5.2 trillion in new spending, and energy prices surged while prices in many other economically sensitive sectors fell.

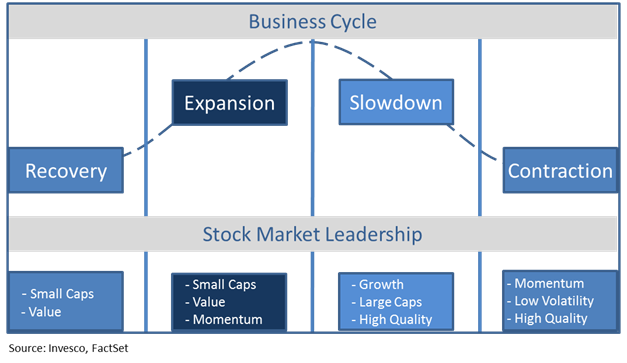

The economy is recovering rapidly, but in an uneven fashion due to repercussions from the pandemic. This has important implications for investors in the stock market. While the current environment is favorable for stocks to move higher, the economic cycle typically determines which stocks lead the market higher.

If growth continues to slow, interest rates are likely to fall. Sectors that benefit from the pandemic and work-from-home environment are likely to lead the market higher, such as Technology and Health Care. Large companies in these fast-growing sectors also would be expected to do well because historically, larger companies in growth-oriented sectors lead the market higher when the business cycle enters the slowdown phase. However, if growth strengthens again and rates rise further, that will indicate the economic cycle is still in the expansionary stage. Businesses that benefit from the improving growth rates and extraordinary level of stimulus usually outperform the rest of the market during this part of the business cycle. These tend to be concentrated in value-oriented stocks and include companies in the Financials and Industrials sectors, as well as smaller companies.

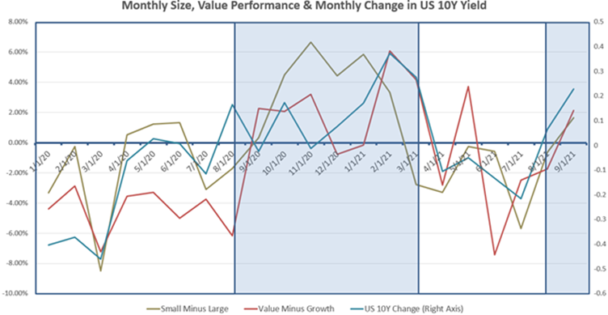

These trends have been very noticeable throughout the pandemic. The chart below plots the monthly difference in the returns of Small Caps versus Large Caps, Value stocks versus Growth stocks, and the change in the yield of the 10-year Treasury Bond. When it appears that the recovery is gaining steam, rates have risen and small stocks and value stocks lead the market (above zero on the chart below). However, every time it appears that growth has peaked and is slowing, interest rates fall and large stocks and growth stocks lead (below zero on the chart).

Source: Factset

The stock market is poised to move higher because there are still many positive dynamics that foster an environment favorable for stocks. Despite the anticipated tapering, Federal Reserve policies remain stimulative. Corporate earnings have been resilient in the face of all the uncertainty. The Biden administration is still attempting to pass two fiscal stimulus packages and infections of the COVID Delta Variant appear to be cresting, which should allow business activity to continue to improve.

While very few people would argue that stocks are cheap, they are not excessively valued. Corporate profits are strong, and although their growth is slowing it remains solid. GDP growth is slowing but is still above trend. The Fed is clearly determined to keep rates low well into next year, potentially until 2023. This is an important point because it impacts investor sentiment.

With yields still extremely low relative to history, investors are reluctant to move out of stocks and into bonds. So, when there is a change in the perception of where the economy is in the business cycle, money flows out of one group of stocks and into another group, but not out of stocks entirely. This creates a situation where stocks may not move sharply higher, but they are unlikely to have a major correction either. However, even if markets are flat there can be a lot of trading as investors swap into and out of sectors based on investors’ perceptions.

There are also many concerns that could restrict stocks from making another sharp move higher. There are worries about how the US Federal Reserve may react if inflation proves to be more persistent than they currently believe. Will they hike rates aggressively to reign it in? In the past, such a move by the Fed has typically caused stocks to fall, at times by a lot.

There also is the feeling that stocks are vulnerable to a correction because they have risen a large amount in a short time, and many stocks have valuations that are in the upper range of their historical average.

Another concern is the potential collapse of China’s giant property developer Evergrande, which has over $300 billion in liabilities, which could trigger more real estate firms in China to fail and bring about a wave of bank failures like what happened during the financial crisis of 2007 – 2008.

None of these scenarios appear to have a high probability of occurring. Inflationary pressures should dissipate once corporate supply chains adapt to the post-pandemic environment. While many stocks have valuations that are stretched, many others have very reasonable valuations. And with rates so low, investors are hesitant to give up on the stock market any time soon. Finally, while China may not bail out Evergrande, it will likely assist the company in working through a restructuring to limit the extent of the damage done to its economy.

The result is likely to be more volatility in the stock markets, with stocks expected to generate positive, albeit modest, returns over the next year. With so much uncertainty, it is prudent to maintain a diversified mix of stocks that includes both large growth stocks as well as smaller more economically sensitive value stocks to ensure participation if the stock market produces only mid-single digit returns in the next twelve months. Also, stocks in companies that have consistent earnings, a high-quality balance sheet and are generating solid cash flow are likely to do well during times of uncertainty.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.