Co-author: Alexander Wood, Student, University of Richmond Robbins School of Business, and HBK CPAs & Consultants Intern

As the financial industry has evolved, it has yet to find a way to help the individual investor be more successful without the support of professional guidance. One could argue that, with the amount of information overload today, the industry has done more to hurt than help these investors. Study after study shows the average investor simply doesn’t invest well.

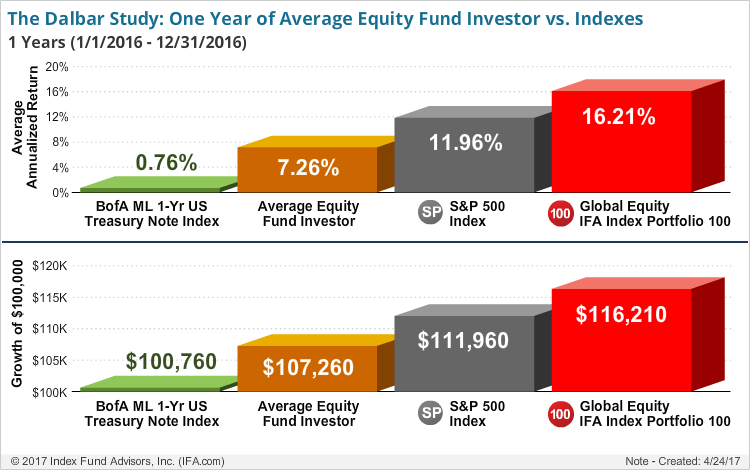

One commonly cited ongoing study is Dalbar’s Quantitative Analysis of Investor Behavior, which has now conducted over 25 annual analyses of 30 years of historical investor returns and 30 different categories of investing. The study consistently reports the same result: the average investor, especially on their own, loses. According to the most recent release, the average equity investor underperformed the S&P 500 substantially – over the 30-year period the average investor should have invested with almost no risk in 1 year treasury bonds and been more successful, but this experience unfortunately isn’t limited to equities.

Some stats:

- Average Equity Investor Return in a negative year like 2018 was -9.42 percent; the S&P 500 was -4.38 percent.

- The Average Equity Index Fund Investor in 2018 underperformed the S&P 500 by 2.84 percent.

- The 20-year average equity investor underperformed the S&P 500 by 1.74 percent per year.

- The 10-year average equity investor underperformed the S&P 500 by 3.46 percent per year. To put this in context, for every $100,000 over 10 years invested at 10% vs the average investor – that’s roughly $70,000 left behind by the end of the 10 years!

Source: Dalbar 2017 QAIB Study, Morningstar Inc., itabt.com, IFA – Created: 4/24/17

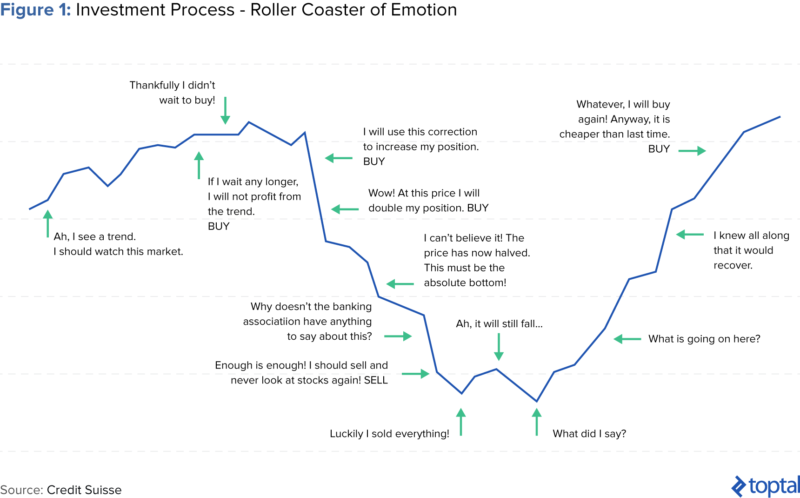

By focusing on fund fees and advisor compensation (all worthy considerations), investors tend to overlook the value of professional advice to keep them on track toward their investment goals. An advisor doesn’t just help the investor develop an investment strategy and plan, but counter poor investment psychology which is incredibly powerful. Studies have shown investor behavior left to itself isn’t any different than normal human psychological behavior (developed over millennia):

- Loss aversion: Fear of loss as a result of the mind feeling pain twice as strongly as pleasure. Example – not selling a stock because its down even though it may be an awful investment (its not real until they sell it).

- Narrow framing: Not being able to see the forest because you are staring at the trees or in finance terms, a tendency to see investments without considering the overall big picture.

- Mental accounting: Taking big risks in one area and avoiding risk completely in others. An example would be investing in penny stocks but hoarding cash or taking large gains from an investment that is “found money” and speculating with it rather than realizing those dollars are just as important as any other dollars.

- Diversification: Normally a good concept, but in this case seeking to reduce risk by relying on different sources, but often investing in the same things (just different places). For example having an IRA two difference places… both investing in US large Cap stocks with very similar profiles creating overlap and overexposure.

- Herding: Copying the behavior of others or as my mom put it as a kid – jumping off a cliff because everyone else is doing it.

- Regret: This isnt having regret, but rather including the fear of possible regret in their investment decision making. This leads to investors being unnecessarily risk-averse or overly risky.

- Anchoring: Relating to familiar or irrelevant information for making decisions. That stock is expensive because its $1,000/share or its more valuable because its $1,000/share regardless of the meaningful measures of value.

- Media response: Simply put – The media is there to sell advertising not necessarily providing a fiduciary level viewpoint, this behavior though is to use media as a driver of your investment behavior.

- Optimism: Good things happen to me with no consideration for the alternative until it happens, often then triggering mental accounting, narrow framing and/or loss aversion. Another example is market timing. Although every long-term study shows that market timing doesn’t work, investors believe “I am different”.

Source: Credit Suisse

Help for the unadvised

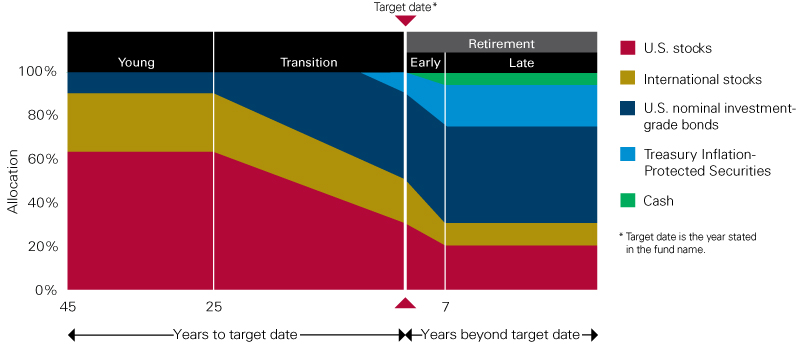

While studies show that most people need some level of guidance, the fact is professional advisors aren’t for everyone, even if many people know they need help. So how can the financial service industry help those without advisors to keep them from hurting themselves as the studies show? Enter target date funds, mutual funds designed to grow assets within a specific timeframe. As the name suggests, investors choose a fund with a “target year” that approximates the time they anticipate needing to start to withdraw their money. Target funds follow a “glide path,” which defines the asset allocation from the time of inception to the target date. When the investor is young and more risk-tolerant, their target date portfolio is more equity-focused, as they are still producing income. As the investor gets older and closer to retirement, the portfolio rebalances with more emphasis on fixed income, lowering risk.

Source: Vanguard https://retirementplans.vanguard.com/VGApp/pe/pubeducation/investing/LTgoals/TargetRetirementFunds.jsf

The major advantage to target date funds is that everything is on autopilot. The funds are a fund of other funds, professionally managed to accommodate that glide path and regularly rebalanced. The most common use of target date funds is for retirement savings and college 529 plans; 401(k) plans have adopted them as their standard investment strategy, often the default investment option when no election is made.

For an investor to benefit from a target date fund, they first must be reasonably sure that their financial goals and plans will stay the same throughout the investing period. For example, your retirement date will remain relatively unchanged and you will stay invested over that time period. Since the funds perform best long term, the investor should choose their target date carefully. They must also consider what level of risk they desire. Typically, they can decide between a conservative, moderate, or aggressive glide path; they can ultimately switch to a different path if they want to. Each path rebalances over time, but the riskier track will continue to be more equity focused.

Another comforting factor is that the investment choices are made by an outside professional. If the individual lacks investment knowledge or does not have time to research and actively manage their portfolio (which clearly investors don’t succeed at even when they try), target date funds can be enticing because the fund’s managers do all the work. Of course, people who enjoy managing their assets and don’t want outside advice will likely find themselves less fit for a target date fund.

Some detriments

While there are many advantages to target date funds, there are some potential detriments. If an investor decides to purchase these funds outside an IRA or qualified plan, they could realize capital gains on a relatively regular basis as the funds are rebalanced, making them tax inefficient. And beyond regular rebalancing, investors lose the ability to manage their taxes: for deferring taxes in a high-tax year or accelerating them in a low-tax year. They also lose, for the most part, the ability to harvest losses. Another potential disadvantage are the fees charged by the various underlying funds. Since a target fund is essentially a fund of mutual funds, each with its own expense ratio, the fees can quickly add up and reduce actual returns. According to Morningstar, the average expense ratio for a target date fund is 0.62 percent but can be as high as 1 percent. Investors can reduce expenses by avoiding the target date fund and investing directly in the underlying mutual funds, but they but would lose the advantages of an outside manager and have to reallocate the funds manually to match the glide path.

Perhaps the major drawback to target date funds is that they tend to be too simple to accommodate peoples’ more complicated lives. And they tend to be used very poorly. For example, they are designed for an investor to put all their money into, such as a 401k, but investors tend to spread their money across a variety of funds including these, thus countering the power of simplicity, and effectively negating the value they bring. Having 3 target date funds and 5 index funds is not a strategy, yet we see it all the time. There is also no one there to stop them from timing with these funds – as an example – being in the aggressive 2050 fund in good times and after the market drops they move to the 2022 fund, thereby missing any rebound had they remained in the 2050 fund all along.

Overall, target date funds can be a sound investment for individuals if used properly. This is especially the case if they have a modest balance and lack professional advice. They provide professional management and a well-balanced track to make sure savings are preserved and growing while reducing investor stress. The key to using target date funds successfully is using them the way they are intended and most importantly – leaving them alone to do their job.

Still, data indicates that an investor with sufficient dollars and professional advice can create a significantly more sophisticated portfolio managed around the uniqueness of an individual and their personal financial plan. Not only can it be built to “suit” the individual’s goals, but also manage the third biggest drag on long-term performance of a financial plan, taxes. To be clear, the biggest three drags are 1) client withdrawals/utilization, 2) bad investment behavior and 3) taxes. Perhaps even more importantly, a professional advisor can prevent an individual from following their instincts.

Advisors are the first and last line of defense to keep people on track. Target date funds and robo-managed plans simply cannot do that. But for individuals who will not use an advisor, target date funds are likely a better option than winging it.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.