The economic recovery continued to strengthen into the second quarter this year, but are investors too optimistic regarding how long growth will continue to improve?

Most recent economic data shows that economic growth is recovering from the pandemic-induced lockdowns faster than many economists expected. The ISM manufacturing index in March rose to its highest level in thirty-seven years. The monthly employment report for March was much better than anticipated, with 916,000 jobs being created in the United States. The services index also improved in March, with all 18 service industries exhibiting growth. The success of the vaccination rollout is enabling consumers to go out for entertainment more often, and they are flush with cash thanks to stimulus checks. High-frequency data, or data that can be collected almost immediately after transactions take place, confirm that activity has started to rebound more quickly. Airport traffic, restaurant dining, and hotel occupancy are all rising fast. The economic-activity index, calculated by The Economist magazine using data from Google, has jumped recently and is now only about 20% below pre-pandemic levels.

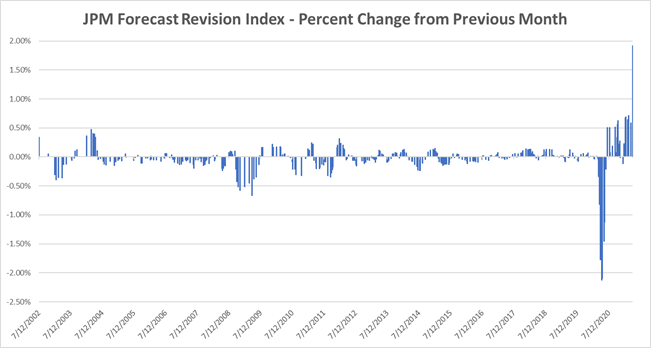

A dramatic rebound in optimism regarding the economic outlook for the rest of this year is driving the recovery. Both consumers and economic forecasters have gone from extreme pessimism to extreme optimism in the span of just a few months. In March, the Consumer Confidence indicator posted its biggest one-month gain since 2003. Also, the quarterly change to the JPMorgan Forecast Revision Index, which measures how much economic forecasts have changed either upward or downward over the course of the quarter, had its single biggest upward move in history.

At the beginning of the year, the COVID numbers were spiking after the holidays, and the vaccine rollout got off to a horrible start. Also, it appeared that the Senate was going to be divided, which meant the passage of another round of stimulus was unlikely. However, by the end of the quarter, an historic stimulus bill was on target to be passed, and additional spending on infrastructure was being discussed. COVID-related deaths and hospitalization rates, which were still trending higher to start the year, are now falling rapidly. The distribution of vaccines is going much more smoothly than it was earlier, prompting President Biden to announce that all adults in America will be able to receive a vaccine by April 19th. Already, many states have begun lifting COVID-related restrictions.

Source: JP Morgan and Bloomberg

Source: JP Morgan and Bloomberg

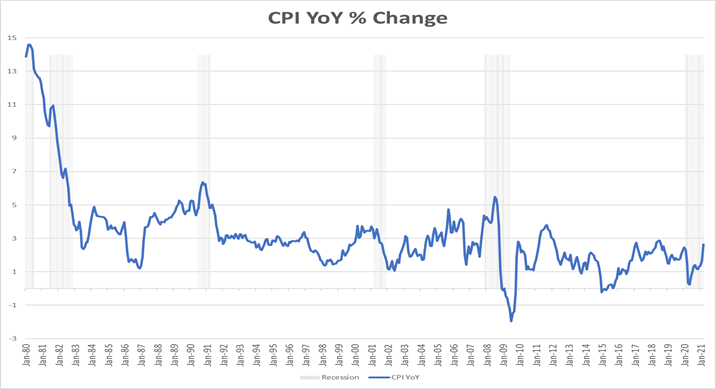

In the span of just a few months, an expectation of stronger growth has turned fears that the recovery would be derailed into fears that the economy will become overheated. Inflation climbed 4.2% for the twelve months ending in March, and Treasury yields have risen accordingly. The Ten-Year Treasury Bond yield increased from 0.93% to 1.74% during the first quarter of 2021.

Still, Federal Reserve Chair Jerome Powell reiterated that he believed the rise in inflation will be transitory because there is ample slack in the labor market and supply chains will adapt and become more efficient. After all, the Federal Reserve has been trying unsuccessfully for many years to generate inflation to no avail. The forces that have kept inflation in check – global competition, improvements in technology and just-in-time inventory management – are still present. In addition, the US economy is nowhere near full employment, and inflation has never risen dramatically with the unemployment rate at current levels.

Shading indicates recession. Source: Federal Reserve Economic Data (FRED)

Shading indicates recession. Source: Federal Reserve Economic Data (FRED)

Those who argue that inflation will continue to spike higher point to the fact that the recent increase is the fastest pace since September of 2011.

However, the spike in inflation proved to be transient then, and it may this year as well.

After the initial surge in business activity in the United States, the economy will probably revert to the slow growth we saw before the pandemic. The impact of the fiscal stimulus likely will not have a long-lasting effect on global growth for several reasons. The boost in consumer spending from the stimulus checks are one-time payments, and not an increase in the annual income of consumers. Also, the Federal government is providing rescue funds to prevent the economy from collapsing, not to stimulate new investment. A lot of the stimulus is going to state and local governments and universities to plug deficits and distribute vaccines, so the spending will only provide a short-term boost.

Source: Federal Reserve Economic Data (FRED)

Source: Federal Reserve Economic Data (FRED)

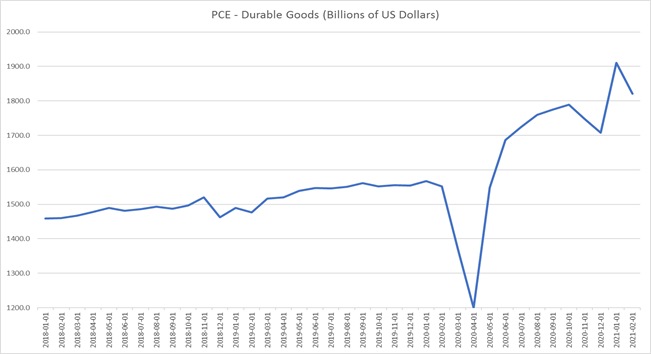

Additionally, last year during the lockdowns many consumers cut back on travel and entertainment spending but boosted their spending on household goods. As the economy reopens, this trend is likely to reverse, which would keep economic growth on a solid but potentially lower trajectory than many anticipate. Higher spending on travel and entertainment, which has a relatively small impact on GDP growth because it does not get multiplied as much through the supply chain, will likely be offset by a drop in spending on durable goods, which has a larger impact on GDP growth because it has a longer supply chain. As a result, the burst of economic activity this year will probably be followed by a long, slow recovery, and inflationary pressures should ease.

The optimism being displayed by many market participants could mean that the most positive view on the economy and corporate profits the rest of this year is already reflected in the level of both bond and stock prices. If the effect of the stimulus is less than is currently expected, the disappointment may induce short-term volatility in the capital markets. At the very least, the path forward for the stock market appears to be much more challenging, while the outlook for bonds may be brighter than the current dire consensus.

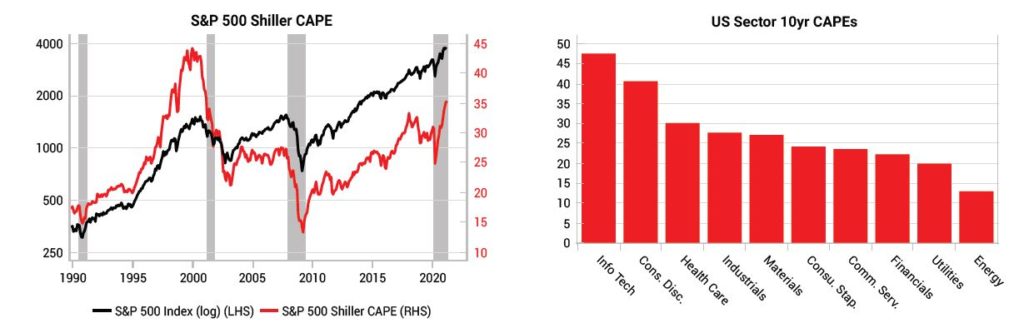

Valuations in the stock market, while not excessive, are stretched in some sectors. Still, there are some potentially attractive opportunities.

Source: Variant Perception Research

Source: Variant Perception Research

Stocks may trend higher, but the stocks that will lead the market forward are likely to be different than those that have led the way for much of the bull market. The stocks that have led the market have been the large, high growth companies in the Technology and Consumer Discretionary sectors. These stocks generated strong growth even in a pandemic and are leaders in several technological trends which will continue to shape the world’s economy going forward such as robotics, video conferencing, shopping from home, financial services innovation, and cloud computing.

Many of these stocks have valuations that are now priced for their growth to continue to accelerate long into the future, however, there are numerous reasons why their growth could slow. Privacy and monopoly concerns are causing regulators in many countries to investigate what restrictions on these companies should be enacted. The tax policies of many countries also are being reviewed to make sure these high-growth companies pay more to help pay off the debt that has grown rapidly in the past year. At the same time, the surge in earnings that many of these companies received during the lockdowns may have come from pulling future growth into last year. That could mean that future growth will be lower than is expected, while last year’s growth was higher than expected.

Meanwhile, the earnings of companies in the Energy, Utilities, Financials, Communication Services, and Industrial sectors were depressed during the pandemic, but are going to benefit the most from the recovery in economic activity and are much more reasonably valued than many other sectors.

Longer term, there are several additional technological trends that also will shape economic growth over the next five to ten years, including 3D Printing, bioinformatics, and nanotechnology. The prices of the stocks of the mega-cap companies benefitting from these trends are also beyond where the company’s fundamentals would indicate the price should be. However, there are opportunities in many other companies that also benefit from these trends but do not have as high a profile and are more reasonably priced. These companies are generally smaller than the huge technology firms and provide the software and services that drive these technologies. We believe that they will also do well relative to the rest of the stock market.

With investors expecting economic growth to continue accelerating the rest of this year, slower than expected growth would bode well for returns in the bond market as well. Yields seem to have entered a higher range but may not rise much further. Inflation expectations are at the highest level in eight years, and some economists do not believe the Fed when they say they will not raise rates this year. With a rate hike in 2022 expected by many, an extremely positive economic outlook may be priced into the bond market. If growth is more moderate than is expected, and the Fed is true to its word and does not hike rates in 2022, the selloff in bonds may be overdone. As a result, longer-term bonds may perform better than most people anticipate over the next year. Also, with no recession in sight, the strong relative performance of bonds with lower credit quality could continue.

So, returns in both the equity and fixed income markets should be modest, but positive in 2021, and several pockets of opportunity still exist. However, there could be more bouts of volatility as investors realize economic growth will not be as strong for as long as many currently anticipate. We believe that the balanced HBKS investment approach, which incorporates broad diversification among some asset classes that will benefit from the recovery in economic growth as well as some asset classes that will protect a portfolio from losses during stressful times, is well suited for this environment.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.