Pandemic-Induced Recession Could Be Deep But Short In Duration

The global response to the COVID-19 pandemic has caused an unprecedented shock to most economies in the world. Social distancing and business shutdowns, while necessary to curb the growth of new COVID-19 infections, has caused business activity to practically grind to a halt. As many countries begin to explore how to restart their economies, the near-term outlook for a recovery in global economic activity is highly unpredictable. As a result, global equity markets have been extremely volatile over the past few months. Going forward, the volatility is likely to continue as the news flow regarding COVID-19 swings between optimistic and pessimistic outcomes.

Governments and Central Banks around the world are providing monetary and fiscal support in order to move past the current economic shutdown. The current recession was caused by the intentional shut down of economic activity, so it was widely anticipated. The massive relief funds are being applied pre-emptively, not after the fact as in previous recessions. They are intended to act as a bridge to keep businesses afloat until the self-induced recession is over and the world gets back to some level of economic activity. As a result, investors have begun to look beyond the pandemic, and toward what the business climate may look like the rest of 2020 and into 2021.

It appears that the current recession will be deep but short in duration. Economic growth historically has bounced back faster after short recessions, no matter how bad they were. Still, going forward consumers will likely travel less, do recreational activities outside the home less often, go to fewer live events, and shop in stores less often. On the other hand, people will likely use streaming services and social media for entertainment more and shop online more. The net effect will likely be a drag on growth the rest of this year and possibly into 2021.

Economic growth is likely to be choppy but should regain its footing as we move into next year. Meanwhile, the additional liquidity being provided by governments around the world should boost risk assets. Equity markets are still well in range of their highs, and equity valuations are now attractive for long term investors. Near-term movements in markets are very hard to predict, and so stocks may temporarily move lower again. But throughout history stock markets have withstood famines, pandemics, world wars, and financial crises. Throughout it all, stocks have always recovered and continued to move higher.

For long term investors, we believe investors should have a long term, strategic asset allocation while maintaining the possibility of adding to any asset class that displays a particularly compelling return potential. Of course, any increase in an asset’s allocation must be done within the overall framework of each investor’s risk profile. Currently, equity markets appear to possess an attractive risk/return profile.

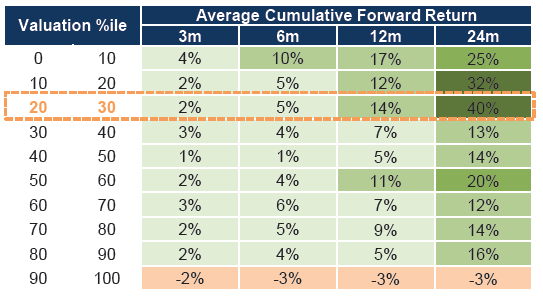

According to Goldman Sachs Global Investment Research, at current equity valuations (about 20 times earnings), global equities have, on average, produced attractive returns over the following time periods:

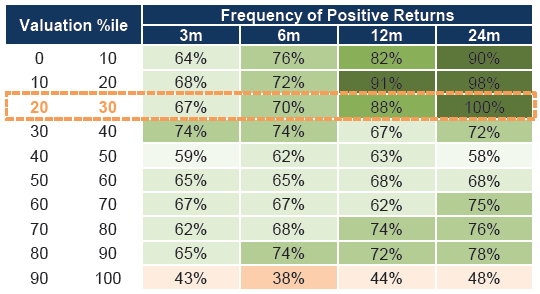

Also, there is a high probability of generating positive returns over those same time periods:

We believe that long term investors are likely to be rewarded if they add to their equity positioning at current levels if done within the risk framework of their long-term strategic allocation.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.