Managing investments in retirement is challenging enough, but steering them through volatile and uncertain times, in particular in a post-COVID world, can be harrowing. Yet it is an unavoidable task for the four to five million Americans who retire every year.

As a Certified Financial Planner(TM), I regularly encounter the concerns of clients who are in or considering retirement. Their questions about how they should be invested vary widely, from whether they should adhere to the age-old idea of owning the percentage of bonds equal to your age—if you’re 65 you should have 65 percent of your invested dollars in bonds—to whether someone with enough money to live comfortably for the rest of their life and no desire to leave a legacy should take no risk at all (even though no one knows just how long they will live and what their expenses will be).

As I’m having more and more of these conversations with clients, I decided to take a look at a more quantitative approach to investing in retirement. You might have heard of a “bucket approach” to retirement income planning. What if we use a similar approach to asset allocation?

Strategy

The idea involves using your needs in terms of retirement income to create a series of buckets that combined will supply that income. The strategy is completely customizable to each individual based on risk tolerance, personal goals, and variables like inflation. For illustration purposes, let’s use a broadly applicable if oversimplified approach:

- Bucket #1 consists of two years of needed income invested conservatively in cash and fixed income securities. Putting the required dollars in these types of investments will spare the retiree from a market correction.

- Bucket #2 consists of eight years of needed income, providing in combination with Bucket #1 a total of ten years of needed income. This bucket will be invested in a more balanced portfolio of stocks and bonds, allowing the appreciation in value during rebalancing to be used to replenish Bucket #1.

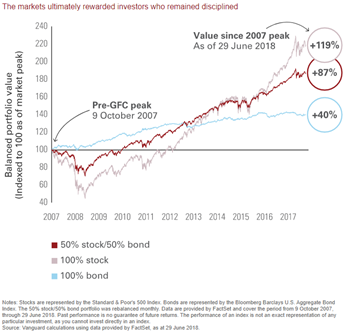

The diversified, balanced portfolio historically has fully recovered within two years as demonstrated in the chart below:

- Bucket #3 will contain any assets remaining after the first two buckets are allocated. They will be invested via a more growth-oriented allocation in accordance with the individual’s risk tolerance and financial needs or goals. The portfolio could range from 100 percent in stocks to a more moderate growth allocation with a blend of stocks and bonds, a combination of investments that will allow for replenishing Bucket #2 through different market cycles.

Execution

Let’s put our approach to work with a hypothetical example. Mr. and Mrs. Smith are about to retire. They have a combined Social Security income of $50,000 annually, and have accumulated a nest egg of $1.5 million. They estimate that they will need $100,000 a year to live on. We’ll divide their funds into three buckets and invest each bucket as follows:

• The buckets:

Bucket #1: $100,000 (two years of $50,000 each year required to supplement their Social Security income)

Bucket#2: $400,000 (eight years of $50,000 each year required to supplement their Social Security income)

Bucket#3: $1,000,000 (The remaining assets)

• The investment allocations:

Bucket #1: 50 percent cash/cash equivalents; 50 percent short-term fixed income

Bucket #2: 40 percent stock; 60 percent fixed income

Bucket #3: 70 percent stock; 30 percent fixed income

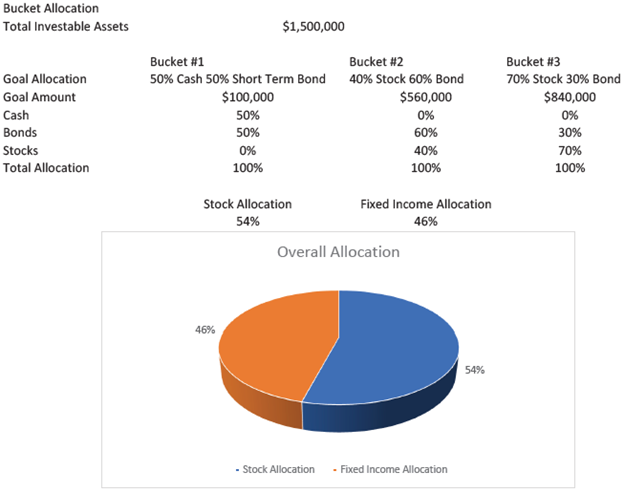

The following table illustrates the bucket distributions and the overall allocation resulting from the blending of the three: 54 percent in stocks; 46 percent in cash and fixed income:

This information is only intended for educational purposes to show an example of this type of offering.

In the above example, the Smiths have invested their savings into one overall allocation that includes multiple approaches. It does not take into account inflation or any of the many other variables we would include in an actual plan. Nor does the example consider the wide variety of investment options available to the Smiths.

Considering the current interest rate environment, one we haven’t encountered in 15 years, some additional tools might now be sensibly employed. With today’s more attractive interest rates—we haven’t seen fixed income rates on five-year securities above the 5 percent mark since 2007—fixed income options like the single premium annuity (SPIA) and multiyear fixed deferred annuities can build out portions of these buckets with more certainty than previously used bond options. The use of a five-year SPIA to provide needed income to cover expenses paired with a five-year fixed annuity to replenish the initial SPIA would be a way to guarantee covering the next five years of expenses with no market risk.

Having this degree of certainty makes the fluctuations in bucket #3 much more sustainable, as for the next 10 years there will be no volatility in the income needed. A potential additional benefit is that using the five-year fixed annuity will defer the taxes on the gain allowing for more compounded growth. Upon maturity, the annuity can be exchanged for a replacement five-year SPIA allowing the unrealized gains to be spread out over the next five years with the use of an exclusion ratio that SPIAs provide.

When clients ask me if annuities are bad investments, my response is always the same, as it is to most financial questions: “It depends.” It always depends on the particular situation. The above chart demonstrates how markets reward patience and discipline. An annuity can provide the certainty needed now, as well as allow the longer-term goal traditional investment to function through an economic cycle.

There are many ways to determine how to invest at retirement to meet your ongoing needs and goals. The bucket approach may not be right for every retiree, but it is one way to help you visualize why your investments are positioned the way they are and the reasons for and methodology of rebalancing. It is important to begin planning by taking your risk tolerance into account to ensure you can weather the ups and downs in the market and stick with a long-term plan. Your plan should also consider time horizons, such as investing for a near-term goal.

We’re here to help. Contact an HBKS advisor for customized retirement income planning.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.