Article updated March 2024

Much of what was spoken by the characters in Christopher Nolan’s Oscar-winning “best picture” Oppenheimer reverberated with me. One particular scene, which takes place in the desert of Santa Fe, New Mexico, has Kitty and Robert Oppenheimer reflecting on the global conflict of the early years of World War II. Kitty proclaims, “Everything is changing Robert. The world is pivoting in some new direction…It is reforming.”

While certainly not as historically consequential as WWII or the dawn of the atomic era, we too are living through a changing, reforming period of time, most notably on an economic front as it pertains to monetary policy as set by the U.S. Federal Reserve. In March 2022, the Fed embarked on a period of aggressive and hawkish interest rate tightening that lasted until the middle of the summer of 2023. The year 2022 ended up being an extremely challenging year for stocks and bonds, the first time in 45 years that both stocks and bonds fell significantly in value in the same calendar year. This rise of interest rates was the most aggressive example of tightening monetary policy in those last five decades. Then 2023 closed out strong for the capital markets, as markets responded positively to Chairman Jerome Powell’s comments in December that he could see the Fed cutting interest rates as many as three times in 2024. In March of 2024, he reiterated that likelihood.

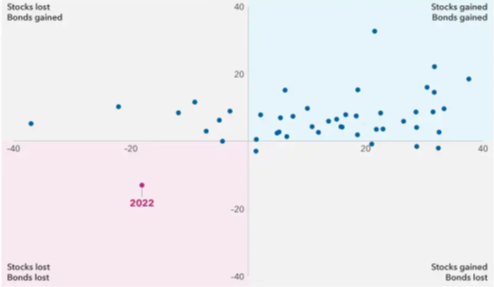

Annual returns for stocks and bonds since 1977 (%)

Sources: “Diversification isn’t dead: Bonds poised to offer balance,” by Capital Group, Bloomberg Index Services Ltd., Standard & Poor’s. Each dot represents an annual stock and bond market return from 1977 through 2022. Stock returns represented by the S&P 500 Index. Bond returns represented by the Bloomberg U.S. Aggregate Index. Past results are not predictive of results in future periods.

Outlook for stock and bonds

As we pivot from a “headwind” to a “tailwind” monetary policy as the Fed gradually reduces interest rates in the coming years, what can we expect from stocks and bonds?

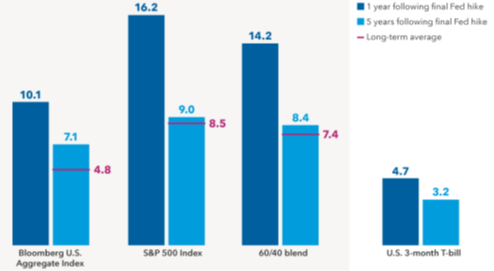

The chart below illustrates how stocks and bonds performed after four separate rate tightening cycles since 1995. The changes in both the 12-month and five-year average returns for stocks and bonds are dramatic. Of course, as the adage reminds us, past performance is not indicative of future results; however, it is informative to reflect on what has transpired in prior periods.

Sources: Capital Group, Morningstar. Chart represents the average returns across respective sector proxies in a forward extending window starting in the month of the last Fed hike in the last four transition cycles from 1995 to 2018 with data through 6/30/23. The 60/40 blend represents 60% S&P 500 Index and 40% Bloomberg U.S. Aggregate Index, rebalanced monthly. Long-term averages represented by the average five-year annualized rolling returns from 1995. Past results are not predictive of results in future periods.

Unfortunately, many investors disenchanted with the returns on stocks and bonds in 2022 fled to cash/money markets/CDs/Treasuries. Deposits in money market funds climbed to an all-time high of $5.6 trillion on September 6, 2023. While cash investors might feel safer for the time being, history shows that investors who flee all or the majority of their investment portfolio during market downturns for cash equivalents miss out on substantial returns on stocks and bonds as interest rates decline from elevated levels.

Words of wisdom

In 2023 I wrote the first version of “Be Like Water” inspired by the words of Bruce Lee. He uses the analogy of the inherent power of water to rapidly adapt or conform to whatever it is placed into, such as a coffee cup or a tea pot:

“Be like water making its way through cracks. Do not be assertive, but adjust to the object, and you shall find a way around or through it. If nothing within you stays rigid, outward things will disclose themselves.

Empty your mind, be formless. Shapeless, like water. If you put water into a cup, it becomes the cup. You put water into a bottle and it becomes the bottle. You put it in a teapot, it becomes the teapot. Now, water can flow or it can crash. Be water, my friend.”

―Bruce Lee

There are various interpretations of what Bruce meant, mine being that you need to adapt to whatever it is you are confronting at the moment.

Investors should work with a financial advisor to prepare a comprehensive financial plan structured around their personal financial goals. The financial plan serves as an investors’ North Star, pointing them in the right direction regardless of prevailing economic conditions in any one year because reaching your long-term financial goals requires a long-term point of view. The planning process includes addressing the overall investment allocation the investor should use in pursuit of their objectives.

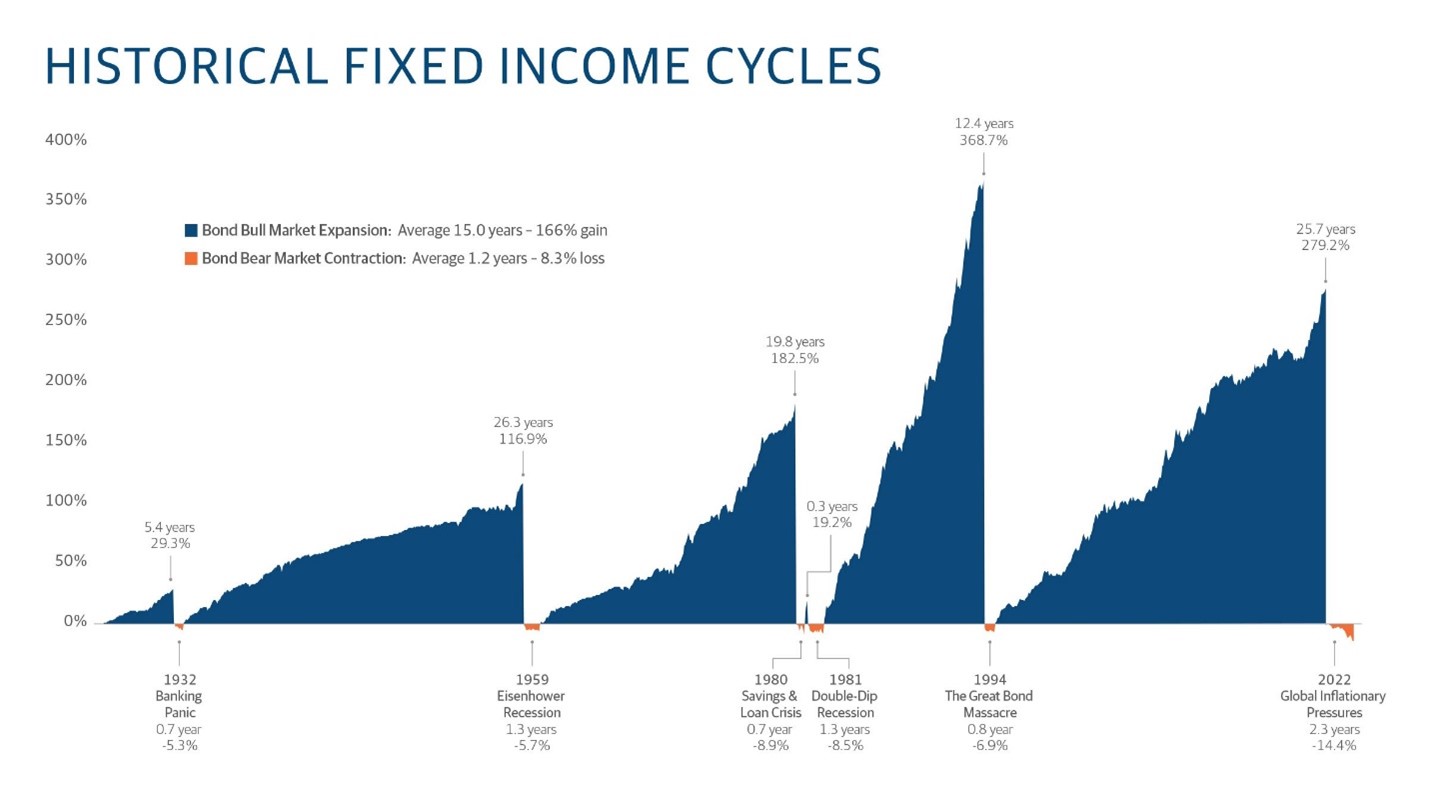

In closing I offer the chart below, which illustrates that while periodic downturns in bonds are not uncommon, on average, historically, they have been short-lived compared to the expansionary, bull-market side of the cycle:

Source: Northwestern Mutual Wealth Management Company. Bonds are represented by the IA SBBI U.S. Intermediate-Term Government Bond Index, which measures the performance of five-year maturity U.S. Treasury Bonds. 2022 data through the end of October. Areas of expansion are defined as bond market performance from the low of a bear market to the high of the market preceding the next bear market. Areas of contraction are market performance from the prior market high to the market low in a bear market. A bond bear market is defined as a loss of 5 percent or greater. All data from Morningstar Direct.

Links to sources used for this article:

https://www.capitalgroup.com/advisor/insights/articles/diversification-not-dead-bonds-poised-offer-balance.html

https://www.schwab.com/learn/story/fixed-income-outlook

https://www.northwesternmutual.com/life-and-money/why-bonds-still-make-sense-in-a-portfolio/

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.