As HBKS Chief Investment Officer Brian Sommers wrote in his recent commentary , the combination of trending economic data and the Federal Reserve’s determination to continue raising key interest rates is edging us closer to a recession. Of course, recessions vary in many ways, including depth and length, so what might this impending recession look like? The following Q&A should be helpful in understanding how that recession might unfold and how to respond to it:

What is a recession? The National Bureau of Economic Research, Inc (NBER) defines a recession as “a significant decline in economic activity spread across the economy, lasting more than a few months.” The decline is typically seen in gross domestic product (GDP) and measures of employment, income, industrial production, and wholesale and retail sales.

How did we get here? The COVID-19 pandemic was marked by a slowdown in supply in both production and logistics and increased demand for many products that were experiencing shortages. Simultaneously an influx of dollars into the economy through Paycheck Protection Program loans and personal household stimulus checks encouraged an unsustainable growth rate in the economy. The combination set us up for a situation where a recession is expected to recalibrate to more realistic growth and inflation rates.

What is the average length of a recession? According to NBER, from 1854 to 2020 the average U.S. recession lasted about 17 months. However, in the post-World War II period, from 1945 to 2020, the average recession lasted only about 10 months. U.S. recessions have become shorter and less frequent in recent decades.

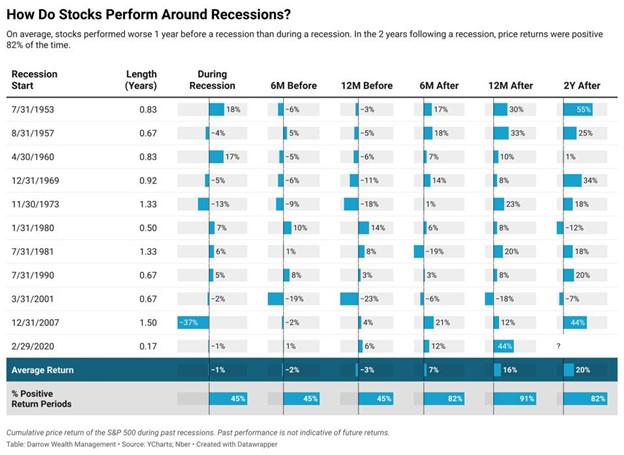

How has the market performed during past recessions? During all recession periods since 1945 the S&P 500 rose an average of 1 percent, as markets typically peak before the start of a recession and bottom out before its conclusion. In most cases, the S&P 500 has bottomed out roughly four months before the end of a recession after hitting a high seven months prior to the start of a recession.

During the four recessions since 1990, the S&P 500 declined an average of 8.8 percent, according to data from CFRA Research. But in over half of the 13 years of recession since World War II, the S&P 500 posted positive returns.

Stock Market Returns During Recession Years

Markets typically bottom out and rebound months before the end of a recession.

Table with 3 columns and 13 rows. Currently displaying rows 1 to 13.

| Recession Year | Recession Year Returns (S&P 500) | Following Year Returns (S&P 500) |

| 1945 | 30.3% | -11.9% |

| 1949 | 10.3% | 21.8% |

| 1953 | -6.6% | 45.0% |

| 1957 | -14.3% | 38.1% |

| 1960 | -3.0% | 23.1% |

| 1970 | 0.1% | 10.8% |

| 1974 | -29.7% | 31.5% |

| 1980 | 25.8% | -9.7% |

| 1982 | 14.8% | 17.3% |

| 1990 | -6.6% | 26.3% |

| 2001 | -13.0% | -23.4% |

| 2008 | -38.5% | 23.5% |

| 2020 | 16.3% | 26.9% |

Source: CFRA Research, NBER, S&P Global.

How is a recession declared? A recession is official when the Business Cycle Dating Committee of the NBER announces it.

What is the average time it takes the NBER to declare a recession? For the last six recessions, the announcement of the start of a recession has been, on average, 234 days after the decline in economic activity as measured by GDP is announced. That translates to approximately eight months to declare a recession, which means in some cases, such as the 2020 recession, we are out of the recession before it is declared to have begun.

What are we focused on? HBKS works with our clients to address recessionary concerns in multiple ways.

Financial Planning: No matter the time period or phase of an economic cycle, we add significant value to our clients through financial planning. The planning process helps our clients establish their goals for retirement. Then, using our sophisticated software, we run multiple random market scenarios to determine the likelihood that the client’s resources will be sufficient to provide for their goals throughout their lifetime.

Because the markets and economy are cyclical, we do not assume the same rate of return every year. As such, many of our clients with desirable success rates before the recent market downturn have been surprised that the market decline has minimally impacted their success rate. That’s a formula for peace of mind and far less stress about day-to-day market volatility.

Investment Management: Our Asset Management Group, as they do in all market environments, continuously reviews the market environment to find ways we may be able to add value to our clients’ portfolios.

Tax Planning Opportunities: We look for tax loss harvesting opportunities to offset current or future gains for clients with substantial non-qualified assets. And we work with our HBK accounting partners to ensure minimal tax consequences through proper planning.

Protection Planning: We examine opportunities for our clients to protect their families against unfortunate events such as premature death, disability, or long-term nursing home stays. We evaluate existing insurance coverages to ensure they are efficient and providing the intended protections.

Business Planning: From startup mode to looking for an exit plan, we work with business owners to identify resources and expertise to be successful in all phases of their businesses.

The U.S. economy will go through cycles. Ultimately, a recession can provide balance by slowing the economy long enough to reset prices and growth to a more manageable, reasonable level and pace. Times of economic uncertainty provide an opportunity for investors to become more mindful of their financial future, and allow us as advisors to help our clients become more diligent about financial planning, to adopt habits that might not be their priorities during more generous economies and markets.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal to the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.