Investors have been accustomed to their core fixed income allocation serving as a counterweight to a weak stock market. But so far in 2022 that hasn’t been the case. Barclays U.S. Aggregate Index, the most popular index measuring bond market performance, is off 9.7 percent year-to-date (YTD) thru August 19 compared to major market equity index declines of 10 to 20 percent. That has puzzled many investors. Why haven’t bonds served their traditional role of stabilizing portfolio returns?

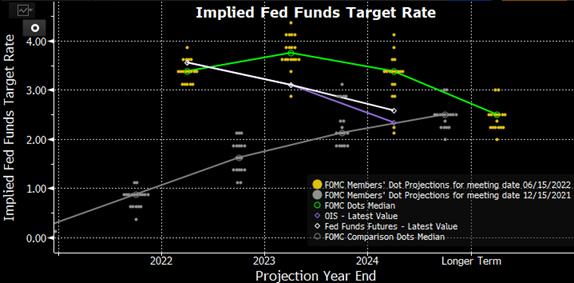

As we entered 2022, interest rates were very low by historical measures, and most investors and global central banks believed a steady pace of interest rate increases from pandemic era lows would be warranted. The following chart displays the members of the Fed’s interest-rate setting committee (FOMC) projections for their policy rate over the next three years as well as for the “Longer Term.” The grey dots (and fitted line) show their projections from their meeting on December 15, 2021. The FOMC, which uses their projections to shape investors’ expectations in pricing of longer maturity bonds via “forward guidance,” was indicating to markets that they believed a measured pace of tightening would lift policy rates toward their longer-term projection by 2024.

Source: Bloomberg LP

However, investors began to shift their expectations for how aggressive the Federal Reserve would need to be in combating inflationary pressures, which have not been ebbing as quickly as expected due to supply side disruptions caused by pandemic mitigation measures. The Russia invasion into Ukraine in February further exacerbated these pressures and has pushed global energy prices higher. In response, financial markets began to price higher interest rates into asset prices notably in March and April when roughly 85 percent of the YTD increase in interest rates occurred.

The increases in interest rates in 2022 have been the main factor driving both bond and stock prices lower. Higher interest rates have a direct negative impact on bond prices and have caused equity market investors to lower their stock valuations.

HBKS Wealth Advisors has helped our clients weather this rise in rates in two ways. We have maintained an underweight in bonds since the middle of last year, and positioned our clients’ bond exposure in ways we thought would better withstand a potential downturn in bond prices. As a result, our clients’ bond portfolios have performed a bit better than the bond market during the part of the year interest rates were rising.

Rising interest rates have been the primary reason for an increased correlation between stocks and bonds recently. In the 20 years prior to February 2020, the Aggregate Bond Index had a negative monthly correlation to the S&P 500 (-0.12); in the 29 months since, it has become positive (+0.60). We expect this relationship will remain elevated in the short term but will likely revert toward historical levels once interest rates reach a more neutral level. We expect correlations to decrease in time because higher bond yields now offer a more compelling investment opportunity via higher income and have a greater likelihood of declining should economic data be disappointing.

Where do we go from here? Investors are currently assessing how much tightening will be needed to bring down inflation and what the impact on economic growth will be from higher rates. The shape of yield curve has become volatile as investors assess the level to which the Fed will increase its policy rate before pausing or halting rate increases. Yield-curve volatility has been especially notable since the middle of June as investors have repriced longer-term interest rates lower in response to weakening economic data. The Aggregate1 Bond index performance—+2.3 percent since June 15, 2022—is notable given the Fed has increased its policy rate by 1.50 percent since that date. This demonstrates how longer-term bonds can react differently to changes in short-term rates and often do not exhibit a one-to-one relationship. We would expect continued interest rate and yield curve volatility in the months ahead until inflation readings show sustained improvement and give pause to the Fed.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.