Markets have been bullish, but as I am reminded often by my wife, I am more “seasoned” now, and with seasoning comes perspective. I am also reminded of one of Mark Twain’s oft-quoted, “History doesn’t repeat itself, but it does rhyme.”

A few warnings that have less to do with market technicals and more with perspective:

Beware of the taxman

Trading is furious, and the introduction of facilities like Robinhood accounts and Reddit trades are making it even moreso. But these spurts are not unique. Markets get frenzied and people feel compelled to take risks, then as markets rise, to take on more and more risk. Much of the profiting is in day-trading stocks, some of which aren’t worth the paper they’re printed on. But the profits are real. So aside from the risk of losing it all, why not join in?

My warning is that most people trade without realizing the implications. One of which is the most obvious – most end up losing. Another is the dreaded word – income tax. Take an investment of $100,000 in Carnival Corp (CCL). You purchased the stock in April 2020 for $8 per share, and by June it has improved to $25 per share. You sell it, and now have an account valued at $312,500, a $212,500 realized gain. Long-term capital gains rates are low: zero percent to $40,400 of taxable income, 15 percent to $445,850, and 20 percent on your gains over $445,850—plus a 3.8 percent Net Investment Income tax. Had you owned the stock for more than a year, your gain would result in tax bill of slightly less than $40,000.

But your gain is short term, and treated as ordinary income. If your total income is more than $414,700 married filing jointly, you would be taxed at 35 percent plus the NIT tax, so your bill on a $212,500 gain taxed at 38.8 percent is now more than $82,000. If you live in a state with state income tax, add that in. If you re-invested your gain and made more money, selling a second time in the short term, add in that tax bill too.

A bubble story

A CPA recounted a story about a client who had made $1 million on a small investment during the dot.com boom and bubble in the late 1990s. The client owed $400,000 in taxes on the gain but no longer had the money to pay them because while they triggered the gain, they then rode it down the next year losing it all. Or the day trader who averaged twice the return of the S&P 500 over five years, but living in New York had a combined tax rate of 50 percent. He was taking huge amounts of risk and time to get the same after-tax return as the S&P 500—not to mention that S&P 500 is incredibly difficult to beat long term, even for professionals specializing in large cap stocks.

My warning here is that trading is fun in straight-up markets where irrational exuberance is winning the day. But understand your risks and the tax ramifications of short-term gains. In my real life experience, few over the cycle end up ahead… and those that do, are far less ahead than they think after the tax bill is paid.

What goes up can wipe you out

The massive amount of federal stimulus has boosted the market. But it does raise questions about long-term effects on our economy given our spending, deficits, and national debt. That being said, we are seeing a tremendous amount of “betting” on the market. Over the years I have been witness to several market corrections, several recessions, and two black swan events. Over that time I have also observed a silly barometer that tells me when times are getting risky and people might want to reassess the risks they are taking.

Leading up to the tech bubble in the 90’s I had a really interesting conversation with a cab driver who told me how amazing the markets were and that he was doing so well he was going to retire at 40. I heard it again in Florida about real estate prices in 2008, by again, a cab driver. I again heard it on a cab ride about precious metals, gold specifically, in 2012, right before prices on that “safe” metal everyone flocked to after the financial crisis dropped almost in half. Now that cabs in my neck of the woods have been replaced by Uber, I had to hear it in a restaurant this time. A very pleasant gentleman who sat behind us with his family was explaining, not quietly, to his mid-to-late-20s kids how they should be investing in Bitcoin, Redditt picks, and tech stocks because these are “sure things” and will make them millionaires. He said he had always lost money in the market before, but he just made $20,000 and thinks he can run it to a million and retire.

My warning here is that irrational exuberance, as coined by Fed Chair Alan Greenspan, is back and this is how and when people get burned. Again, “History doesn’t repeat itself but it does rhyme.” While I think risk levels have drastically increased, I believe long-term in being aggressive in my portfolio too and will remain that way—but well diversified and I am certainly not betting the farm on Reddit, crypto currency and day trading. Too many people take too much risk and end up paying a price. Often times it ends with a phrase – I will never invest in the market again, but in reality, they were never IN the market. They were in a casino. I suggest insuring you are managing your risk, even when being aggressive. If you choose to speculate in the short term, understand the tax consequences and use money you can afford to lose. In my years working with clients, the vast majority of people, even those with large portfolios, do not have money they can afford to lose. They need all of it working for them. Nor do I see people who take inordinate risks end up with superior returns. They do well on the way up, not on the way down, and the average is less than impressive.

Returns that accomplish your goals

As boring as it sounds, spread those eggs across many baskets, remain disciplined to the strategy, rebalance, manage taxes, and don’t try to beat the market. Try to earn returns with the least amount of risk that will accomplish your financial goals. What works for you and what works for your friend is likely very different. I have seen clients with tiny portfolios need nominal returns to accomplish their dreams and I have seen clients with large portfolios run out of money investing conservatively. This is why people seek professional financial advice. We help you build the plan, invest to suit the plan, diversify, and monitor your progress. We plan for the good and for the bad. And we use our firm’s tax experts to help us keep more of your returns in your pocket. That combination of oversights is one of the things that makes HBKS Wealth Advisors unique.

So if you have a plan, stay on it. If you don’t, please make one with an experienced professional. HBKS advisors are always here to help in that respect.

Food for thought

• Gold 2012 – Source Macro Trends

• 2020 – Market disparity between top 10 vs. bottom 490 of the S&P 500 – Source Bloomberg

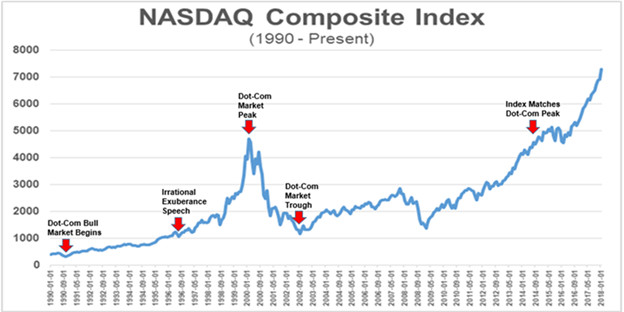

• Dot Com Bubble – Source Seeking Alpha

• Market Value of homes 1970-2014 – Brookings Institute

• Bitcoin Pricing – Coindesk

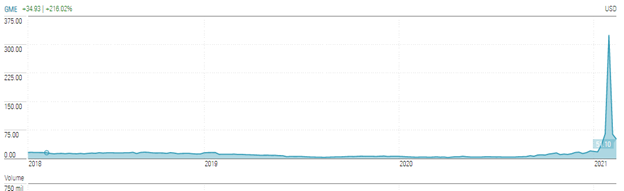

• Gamestop 3 year chart – Source Morningstar

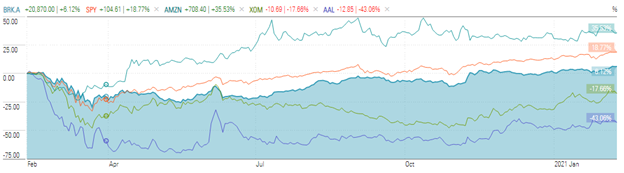

• Just for fun, the world’s greatest investor: Warren Buffett’s Berkshire Hathaway vs. S&P 500 vs. Amazon vs. Exxon vs. American Airlines, last 12 months. Source: Morningstar

Co-author: Alexander Wood, Student, University of Richmond Robbins School of Business, and HBK CPAs & Consultants Intern

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.