As capital markets continue their strong recovery from their pandemic-influenced lows in March 2020, all eyes are on the Fed with regard to increasing the federal funds rate, the interest rate at which banks lend to each other. A rise in the Federal Funds Rate signals similar changes in other lending rates.

Fed Chairman Jerome Powell is likely to follow the playbook of the Fed for the years after the “Great Recession,” that is, provide ample signaling prior to an initial rate hike. Some predict the next hiking cycle could begin in 2022 or 2023. Regardless of when the tightening begins, there will be a great deal of speculation about the impact on the broader bond market.

The value of bonds typically declines when interest rates increase, and the rate hike periods of past decades give us an idea of what to expect with regard to the bond markets in the future. As always, of course, the warning must be issued: past performance is not indicative of future results.

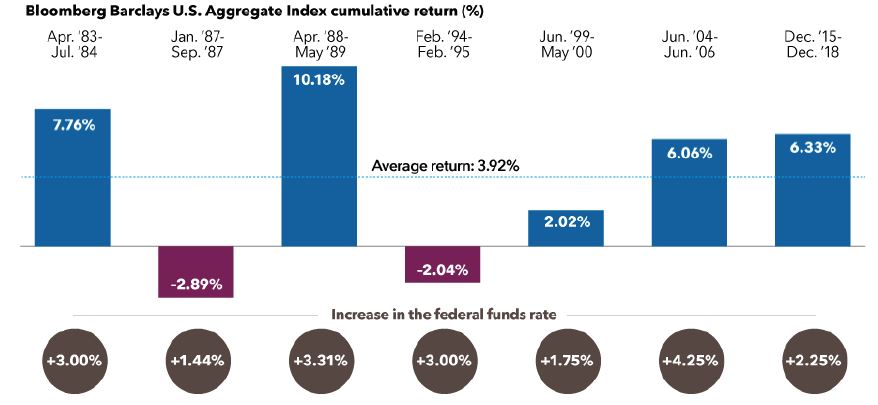

As the chart below illustrates, only two of seven periods marked by an increase in the federal funds rate since the early 1980s produced negative bond returns. The average cumulative return of the Bloomberg Barclays U.S. Aggregate Index was +3.92 percent for the seven periods, despite rising rates.

Sources: Capital Group “Four Reasons Not to Fear Rising Interest Rates”, Bloomberg Index Services Ltd., Federal Reserve. Data through 3/17/2021. Periods represented above include: 4/1/83-7/31/84, 1/1/87-9/30/87, 4/1/88-5/31/89, 2/4/94-2/1/95, 6/30/99-5/16/00, 6/30/04-6/29/06, 12/16/15-12/20/18. Note: Daily results for the index are not available prior to 1994. For those earlier periods, returns were calculated from the closest month-end to the day of the first hike through the closest month-end to the day of the final hike.

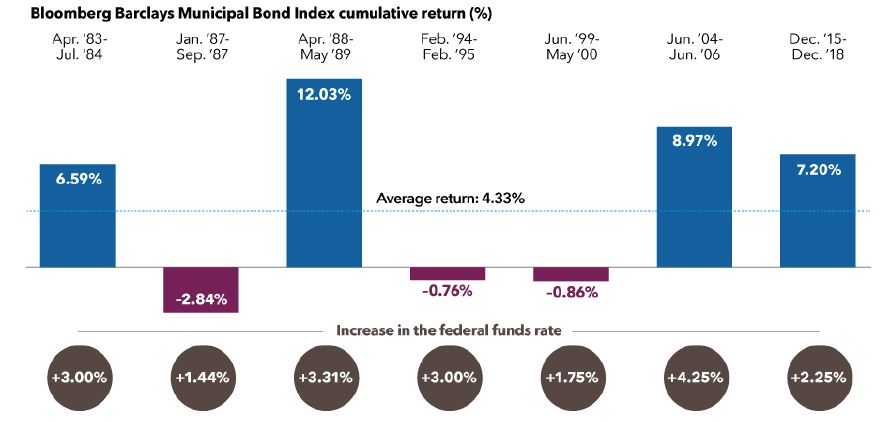

Similar resilience is reflected in the historical performance of the municipal bond market. As illustrated below, the average cumulative return over the seven periods for the Bloomberg Barclays Municipal Bond Index was +4.33 percent (see chart below).

Sources: Capital Group “Four Reasons Not to Fear Rising Interest Rates”, Bloomberg Index Services Ltd., Federal Reserve. Data through 3/17/2021. Periods represented above include: 4/1/83-7/31/84, 1/1/87-9/30/87, 4/1/88-5/31/89, 2/28/94-2/28/95, 6/30/99-5/31/00, 6/30/04-6/29/06, 12/16/15-12/20/18. Note: Daily results for the index are not available prior to 2006. For those earlier periods, returns were calculated from the closest month-end to the day of the first hike through the closest month-end to the day of the final hike.

While stocks globally have performed well in the first half of 2021, the bond market has experienced a strong headwind due to fears of rising inflation. However, we continue to recommend some exposure to bonds as part of a well-diversified portfolio. A proper allocation to core, high-quality fixed income can protect investment portfolios against an unexpected downturn in the equities markets. Additionally, the yield component of bonds can provide a steady stream of income to a portfolio, helping to offset underlying bond price volatility.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.