Prepaid College Plan

If you have children in the Florida Prepaid College Plan and haven’t checked those accounts lately, you should. You might be surprised. If you bought a Florida Prepaid in 2008 or later, you could be due a refund. And not just pennies. I received a refund of $3,000.

In mid-January Governor DeSantis announced that Prepaid Plan prices were being reduced—to the lowest in 5 years—and that, as a result, those buying Prepaid Plans since 2008 essentially overpaid and were eligible for refunds. Roughly half of the 224,000 eligible families are entitled to refunds that average more than $4,000, a total of about $500 million. As well, the reduction means more than 108,000 families have refunds due and/or plans that are paid in full.

Florida has always had a well-designed and funded Prepaid College Plan. The program has run an actuarial surplus for years: in 2018, 123 percent—over 500 percent greater than Maryland, the next best-funded plan. An actuarially sound plan and successive years of lower than anticipated tuition and fee increases have combined to produce the excess in the trust fund.

If you have a plan or plans, simply log into the website (www.myfloridaprepaid.com) and click on each of your respective plans to see the reduction and/or your refund. You can request your refund online or apply it to a new purchase or pay down the balance of an existing Plan or Plans. If you don’t see a refund, check your payments; they should reflect a reduction. If you are currently making an ACH payment, the amount drawn on your account will have changed to reflect the reduced rate. If you are sending your payments, make note of the new amount.

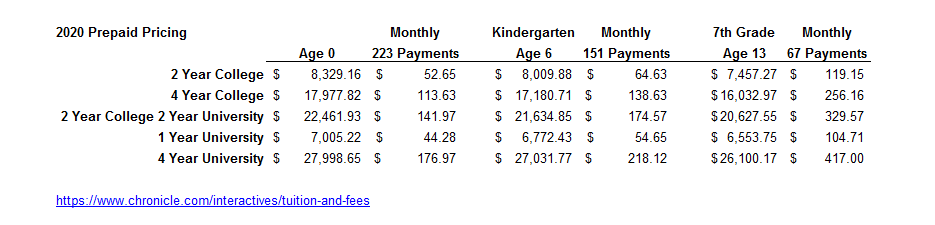

See the chart below for details of current costs. The reduction might inspire you to consider a Prepaid Plan if you don’t already have one. The new rates mean you can buy four years of in-state tuition for roughly $28,000. If you are opening an account for a newborn, consider the cost of that education in 18 years (at just 3 percent inflation) of almost $48,000—plus room and board, of course. That’s in the neighborhood of $100,000. The lesson: if college for your children is a priority, start saving early to maximize the compounding effect of any college savings strategy.

If you want to sign up this year, you need to do so during the open enrollment period, which ends April 30.

Bright Futures (the “other” Florida program)

The Florida Bright Futures Scholarship Program provides scholarships to Florida students attending Florida public universities and colleges. Awards for students attending private universities or colleges are also available, though calculated at a per-credit-hour dollar amount. The awards are made based solely on merit, which is defined as high school academic achievement. The program provides for as much as 100 percent of tuition to most top in-state Florida universities.

Bright Futures offers a Florida Academic Scholars Award, a Florida Medallion Scholars Award, and the Gold Seal Vocational Scholars and Gold Seal CAPE Scholars awards for specialty and technical programs.

The Academic Scholars Award (FAS) is the top award. It provides 100 percent of tuition plus applicable fees, including activity and service, health, athletic, technology and tuition differential fees, among others. An additional $300 per semester is provided for expenses. The Medallion Scholars Award (FMS) pays 75 percent of the tuition cost, including fees, but no additional stipend for expenses.

To qualify for one of the awards, you must complete a series of administrative tasks and requirements. For one, the student must graduate high school from a Florida school with specific “college prep” credits. Both FAS and FMS require 16 such credits: four English, four mathematics, three in natural science, three in social science and two in world language. For FAS eligibility you must also have a high school weighted GPA of 3.5—calculated using the Bright Futures methodology on the 16 college prep courses—as well as 100 community service hours. The FAS also requires an ACT score of at least 29 or a minimum SAT score of 1290. For FMS you must have a 3.0 GPA and 75 volunteer hours, and an ACT score of 25 or SAT of 1210. There are some other ways to qualify, such as obtaining an International Baccalaureate (IB) program diploma, which would waive the weighted GPA and ACT or SAT score but not the course requirements. As the awards are based on merit, the student needs to maintain a minimum GPA for the FAS of 3.0 and 2.75 for FMS to keep the scholarship through his or her college career. Also, Bright Futures requires you to pay the program back for any classes from which the student withdraws.

If you have both a Prepaid College Plan and your student has earned one of the Scholarship Awards, the scholarship money is applied first, then any excess is picked up by the Prepaid Plan. You can request a refund of any excess Prepaid funds, or use them to cover other costs, such as books—or to fill the gap if the student fails to maintain the required GPA and loses the Bright Futures scholarship.

You can also use Prepaid Plan funds to attend a private or out-of-state school if it’s a qualified institution. The Plan pays what it would have paid had the student attended a Florida public college or university. Bright Futures awards are not available for students attending out-of-state schools.

If your child doesn’t use the Prepaid funds, you can cancel the Plan for a full refund of your payments, though you will not receive any of the interest or earnings on your payments. You can retain the growth by changing the Plan beneficiary to another family member who will use the funds for a qualifying college.

While the programs are fairly transparent, they come with some nuances and there are issues to negotiate. As such, it pays to consult your HBKS Wealth financial advisor for help finding the solution that fits you and your student best. We stand ready to help.

IMPORTANT DISCLOSURES

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS® Wealth Advisors) will be profitable or equal the corresponding indicated or intended results or performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.