Congress has passed and the president signed into law a bill that will change not only how you save for retirement, but how you’ll retrieve your savings. Among its provisions, the SECURE Act (Setting Every Community Up for Retirement Enhancement) includes new rules that substantially impact those who inherit retirement funds in the form of qualified plans like IRAs, rules that require you as a plan owner to re-think how you will pass along the wealth in those plans to your heirs.

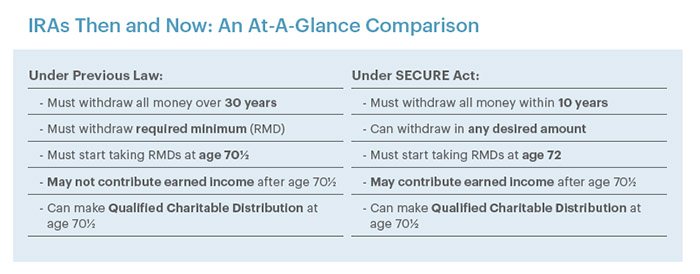

Under the old regulations, your beneficiary was able to draw down the funds in an inherited IRA over a period that corresponds to his or her life expectancy as established by an IRS table. For example, a 50-year-old might have 34 years to withdraw the funds, each year taking a required minimum distribution (RMD), which is determined by dividing the value of the IRA by a life expectancy factor. The SECURE Act changes that. For account owners who die after 2019, all inherited IRA funds must be withdrawn within 10 years of the death of the original owner. Exceptions to this limit are spousal rollovers and accounts where the beneficiary is a minor or disabled. The old RMD rules are grandfathered in, meaning they will continue to apply for those who inherited IRAs before the end of 2019.

Planning is critical

The SECURE Act gives qualified plan beneficiaries the option of withdrawing whatever amount they desire each of the ten years. They could take it all on day one or leave it in the plan and build earnings until the last day of the tenth year. Most likely is that beneficiaries will spread their withdrawals out over the ten years according to a designed plan. Of course, each situation is different, and beneficiaries will need their own financial planning, much of which will consider tax implications—the larger the account, the greater the impact.

For both you as the retirement plan owner and your beneficiaries, planning is critical—not only as the new law applies to their withdrawals, but how you might restructure those savings while you’re still alive to alleviate some of the tax burden for your heirs.

Other retirement plan-related provisions of the SECURE Act:

- Allowing contributions from earned income to a traditional IRA after age 70½

- Increasing the age when a retiree must start taking RMDs: from age 70½ to age 72

- Leaving the age at which an individual can make a tax-advantaged Qualified Charitable Distribution from their IRA at age 70½ (creating a one- or two-year window where IRA distributions may qualify as charitable contributions, but not as RMDs that won’t begin until age 72)

Planning considerations

Accelerated withdrawals are one answer to the federal government’s quest for more tax dollars for Washington to argue over—an estimated $15.7 billion over 10 years. But they also raise a lot of new questions for retirees and their retirement plans, among which are:

- What strategies are available to minimize the tax burden?

- Does it change how you consider charitable contributions?

- Should you convert your IRA to a Roth IRA?

- Will a spousal rollover help?

- Could life insurance provide some replacement value?

There are many issues and options to consider. And while each situation is different, everyone planning to pass along wealth in an IRA or other qualified plan should meet with their advisor to review their financial plan under the light of these changes to the law. We are here to help you navigate these important financial issues.

SECURE Act: A Hypothetical Case

Problem:

Mr. Jones passes away in 2020 at age 85. He leaves an IRA with a value of $1.2M to his son, Charles, who is 54 and married with two teenage children. Charles and Linda Jones’s taxable income for 2020 is $292,000.

Under previous IRS rules—prior to the passing of the SECURE Act—and the IRS Life Expectancy, Table I, Charles and Linda could stretch out required minimum distributions (RMDs) from the inherited IRA over 30 years. The first year’s RMD of $39,344 would not move them into a higher tax bracket; all their income would be captured within their 24 percent bracket. However, under the SECURE Act, they are now forced to withdraw all the money in the account over 10 years, and because Charles and Linda plan to work at least another 11 years, until they are both 65, they decide to spread the distributions evenly, $120,000 per year.

The additional $120,000 increases their 2020 total gross income to $412,000, about $67,000 of which will be taxed in the 32 percent bracket. As well, their gross income is now above $400,000, which triggers the beginning of a phase-out of the child tax credit they have been receiving.

Solution:

The solution involves strategic Roth conversions with the IRA money while the parent is alive to help reduce the tax burden on the heirs.

Per our hypothetical case:

Mr. Jones earned $95,000 of income and was in the 24 percent tax bracket when he retired—he could have earned up to $160,000 in a year and remained in the 24 percent bracket—and began converting his traditional IRA contributions to a Roth IRA. It was an effective strategy. His IRA savings grew tax-free, as were his distributions in retirement, as opposed to tax-deferred as is the case with a traditional IRA.

The strategy proves even smarter when Mr. Jones passes away and the distributions to Charles get bunched into 10 years under the SECURE Act. The distributions won’t impact Charles’ and Linda’s taxable income as the father’s after-tax contributions to his Roth IRA and the earnings are being distributed tax-free. As such, the Roth conversions have allowed both parent and son to take control of their tax planning and generate considerable tax savings.

A “Backdoor Roth” is a strategy taking advantage of a combination of IRS provisions to get the money into a Roth IRA. Mr. Jones could have generated even more tax savings by making a non-deductible contribution to a traditional IRA each year, then immediately converting those accounts to a Roth IRA. With no other IRA savings, he could have made the conversion without incurring taxes on his pre-tax contributions. (See “Backdoor Roth: A Savings Strategy for High Earners,” by Steven T. Swindler, CFP®)

The information included in this document is for general, informational purposes only. The hypothetical scenario does not represent an actual client or client result, does not contain any investment advice, and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. You are not guaranteed similar results and, in fact, actual results may be materially different than those discussed above. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor.

The historical and current information as to rules, laws, guidelines or benefits contained in this document is a summary of information obtained from or prepared by other sources. It has not been independently verified, but was obtained from sources believed to be reliable. HBKS® Wealth Advisors does not guarantee the accuracy of this information and does not assume liability for any errors in information obtained from or prepared by these other sources.

HBKS® Wealth Advisors is not a legal or accounting firm, and does not render legal, accounting or tax advice. You should contact an attorney or CPA if you wish to receive legal, accounting or tax advice.

Insurance products are offered through HBK Sorce Insurance LLC. Investment advisory services are offered through HBK Sorce Advisory LLC, doing business as HBKS Wealth Advisors. NOT FDIC INSURED – NOT BANK GUARANTEED – MAY LOSE VALUE, INCLUDING LOSS OF PRINCIPAL – NOT INSURED BY ANY STATE OR FEDERAL AGENCY.

James M. Rosa is a Principal in the Tax Advisory Group in the Youngstown, Ohio office of HBK CPAs & Consultants and has been with the firm since 1986. He has extensive experience in personal and estate planning, charitable planning, tax-exempt organizations and individual tax and financial planning.