Global investment powerhouse Vanguard sharply cut the expected returns for U.S. stocks in the next decade. If the forecast proves to be accurate, the implications could be significant for retirement-plan sponsors, employees and participants.

In an interview with CNBC on Feb. 15, Greg Davis, Vanguard’s chief investment officer, forecasted that the stock market may not deliver the kinds of annual gains investors have become accustomed to since the bottom of the financial crisis in 2009. “If we look forward for the next 10 years, our expectations around U.S. equity markets is for about a 5 percent median annualized return,” he said. “Our expectations have clearly come down. Historical average annualized returns for the stock market accounting for inflation is about 7 percent.”

Vanguard’s 10-year market call is below HBKS Wealth Advisors’ current outlook for U.S. stocks, though it’s safe to say that our forecast will be adjusted lower too, we are currently reviewing our capital market assumptions. Still, we don’t anticipate our market outlook to be as low as Vanguard’s. For our latest market updates and outlook from the HBKS investment policy committee and chief investment officer, visit our Insights page.

To be sure, making market predictions has proven to be exceedingly difficult for even the most successful investors. Short-term market moves are virtually impossible to predict, with long-term trends only slightly less difficult. Still, Vanguard, a mutual fund giant founded in 1975 with about $5 trillion in global assets under management, is in a position to put some significant resources behind these long-term market calls.

Because of my work with retirement-plan sponsors, I think it is useful to consider the impact on the retirement plan marketplace and retirement plan participants if the Vanguard long-term market call is correct. Lower stock returns over the long run will have significant implications for all participants and correspondingly for sponsors of retirement plan such as 401(k)s.

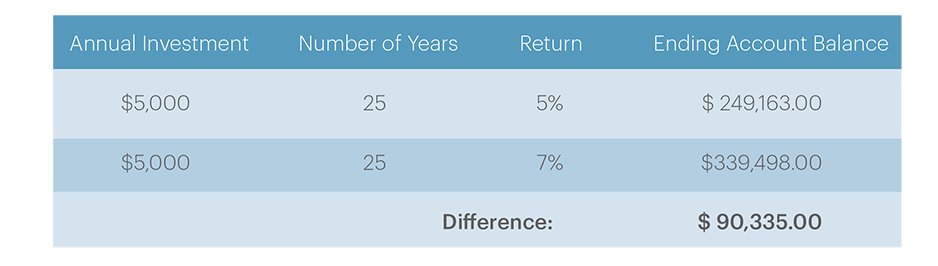

Let’s look at the impact of lower long-term returns from stocks of large U.S. companies. To keep it simple, consider the impact of a two-percentage-point drop in portfolio performance on future account balances on a participant who earns approximately $50,000 per year and saves 10 percent of his wages through a combination of employee salary deferrals, employer-matching contributions and profit-sharing contributions (contributions assumed to be set aside in a monthly basis via payroll deduction).

In this example, a 2-percentage-point difference in expected return means a participant will have about $90,335 less at the end of 25 years. One or two percentage points over a 10- or 20-year period of time can have a material impact on a participant’s ability to build a retirement nest egg and have enough money to last through decades in retirement.

Further, as we consider reduced expectations for U.S. stock market performance over the coming years, participants may need to think more carefully about their personal asset allocation. Diversifying on a global basis begins to be critical. Investors may need to look around the globe or to other asset classes for higher returns.

Consequently, it’s important for plan sponsors to include tools that allow participants to diversify on a global basis effectively as part of their model portfolios and high quality, low-cost target retirement date funds. Such target-date funds or professionally managed models are common default investment options in qualified retirement plans such as 401(k)s or 403(b)s.

For retirement-plan sponsors, lower long-term returns mean high expenses will really stick out. In spite of all of the focus in the industry and from regulators on fees, it is still quite common to see total fees for retirement plan record-keeping, administration, mutual fund expenses and investment advice approach or even exceed 2 percent. If the total fees associated with servicing your retirement plan exceed 2 percent and we do in fact enter this lower-return environment that Vanguard forecasts, then where does that leave net returns for retirement plan participants?

This is why it’s critical for plan sponsors to pay close attention to plan expenses, whether they manage startup and micro-sized plans or large retirement plans. In our firm, because of the volume of business that we do in the retirement plan space, we have the opportunity to regularly provide our clients and prospective clients with a forensic review of the fees associated with servicing their defined contribution plans such as 401(k)s

In a world of significantly lower long-term future returns from U.S. and other developed markets, the impact of fees will be much more apparent to plan sponsors and their participants. As we’ve counseled frequently in our correspondence, retirement-plan sponsors have a legal obligation under the Employee Retirement Income Security Act of 1974 to ensure that the fees retirement plans pay are reasonable, especially those that they pass on to their participants. The critical point is this: You must have a process for making this assessment of reasonableness and be able to document that you’ve done so.

We continue to feel that a best practice for determining whether your fees are reasonable is to commission a benchmarking study that compares your retirement plan fees to other retirement plans of a similar size. This benchmarking study should compare your plan fees to average fees by category of expenses such as record-keeping expenses, administrative expenses and other charges.

If Vanguard’s muted outlook for the markets proves accurate, it will pay for plan sponsors to provide tools to allow participants to diversify effectively on a global basis and to review the plan’s fees to make sure that they are reasonable based on the services provided.

Any investment involves some degree of risk, and different types of investments involve varying degrees of risk, including loss of principal. It should not be assumed that future performance of any specific investment, strategy or allocation (including those recommended by HBKS Wealth Advisors) will be profitable or equal the corresponding indicated or intended performance level(s). Past performance of any security, indices, strategy or allocation may not be indicative of future results.

The information included in this document is for general, informational purposes only. It does not contain any investment advice and does not address any individual facts and circumstances. As such, it cannot be relied on as providing any investment advice. If you would like investment advice regarding your specific facts and circumstances, please contact a qualified financial advisor. This document does not contain any accounting or legal advice. If you would like accounting, tax or legal advice, please contact a qualified accountant or attorney.